The Confidential Report - May 2024

America

In general, politics does not usually have a major impact on equity markets. Politicians come and go – some good and some bad – but mostly their impact is far less than the ideas of the Governor of the Federal Reserve Bank. Sometimes they have a short-term impact on one particular industry, but that seldom results in major stock market trends. 2024 is extraordinary from a political perspective. The outcome of this year’s US and South African elections will almost certainly have a long-term influence on equity markets of the respective countries.

It is difficult to accurately evaluate who is going to win the November Presidential elections. On the face of it, Biden should win easily because he has an economy that is booming and the Democratic Party is very well organised, united and strongly financed. His opponent, on the other hand, is facing dozens of criminal charges, both at Federal and state level. He has loudly claimed responsibility for the Supreme Court’s highly unpopular decision on Roe V. Wade. At the same time the Republican Party appears to be highly disorganised, internally fractured and barely holding on to its paper-thin majority in the House. And it is only May – there are still six months to go before the election. Much can and will happen in that time.

But, as private investors, we cannot shy away from making predictions just because they are difficult. Our investment strategy must be based on some sort of vision about the future. Over time the outcome of this particular US election will have a diverse and pervasive impact on the world economy and on South Africa. It is almost as important as the outcome of our own elections at the end of this month.

The decision by Biden to send the head of the CIA to Egypt to negotiate a peace settlement in the Israel-Gaza war is significant. Biden has lost considerable voter support because of what is seen as his mishandling of the war and his protracted support for Israel. The situation came to a head with the recent killing of seven aid workers by Israel. Since then, the Biden administration has taken a much harder line with the Israeli Prime Minister, Benjamin Netanyahu. The problem remains the Israeli hostages still held by Hamas. There is hope that some may now be released as the peace talks begin to gain ground. Hamas denies that there has been any progress at the talks, but other sources have said that there have been concessions by both sides. The Palestinian losses of over 33 000 now seem disproportionate to the 1136 Israeli’s killed by Hamas at the start of the war. The mounting humanitarian crisis in Gaza is bringing enormous pressure on Israel to allow aid into the stricken area. Biden has obviously become concerned that his continued support of Israel is leading to unhappiness among the American voting public.

The unexpectedly high rise in the consumer price index (CPI) in March 2024 was 0,4% in the month – ahead of economists’ predictions of 0,3% and raising the annual inflation rate to 3,5% from the previous month’s figure of 3,4%. This negative news was added to the 303 000 jobs created by the US economy in March to suggest that the Federal Reserve Bank’s monetary policy committee (MPC) would have to keep interest rates higher for longer. The markets were discounting the first drop in interest rates to come after the MPC’s meeting in June, with two more rate cuts expected before the end of 2024. Those expectations have been sharply reduced now with a concurrent drop in the S&P500 index. At the same time, higher-than-expected retail spending also indicates that the economy is far from cooling down and is, in fact booming. Expectations of the first 25-basis point reduction in rates have been shifted to September this year and the prospect of 3 such rates cuts before the end of 2024 is fading. Investors are now expecting just one 25-basis point cut by year-end. Interest rates, the highest in the past quarter of a century, do not appear to be having the desired effect of cooling the economy down. Clearly, the fading hopes of a rate cut in June are impacting on the S&P500 which is now firmly in an overdue correction.

The growth in gross domestic product (GDP), after inflation, in America in the first quarter of 2024 came in at an annualised 1,6%. This was well below the prediction of economists at 2,2%. Disappointing corporate earnings combined with higher yields on government bonds are also a negative for the S&P500. These factors have gone some way towards improving expectations of rates cuts before year end, leading to a rally within the correction on the S&P. Consider the chart:

The chart shows the S&P since December last year with the strong upward trend and the upside break above the previous record high of 4796, after a period of backing and filling. The current correction began after a loss of upward momentum in March this year and has seen the index fall quite sharply, including a six-day losing streak which is fairly rare on Wall Street.

Right now the index is taking some comfort in the latest figures coming out of the US economy which give a little more hope that rate cuts could begin earlier than expected – leading to a rally within the correction. In our view, however, the correction is probably not over and we continue to expect further downside towards the 4796 level, which has now become a support.

The escalating tensions between Iran and Israel has resulted in increased global uncertainty and is causing more international investors to invest in gold as the ultimate hedge asset – despite the fact that gold offers investors a zero return. The US President, Joe Biden, recently said that the US will not participate in any retaliation strikes on Iran following the launching of more than 300 missiles and drones into Israel by Iran. In our view, this international tension will probably subside in the coming months as diplomats work to find a solution, but the possibility of an Iran/Israel war has heightened investor uncertainty worldwide. Iran has been widely blamed as the instigator of the on-going war in Gaza as well as the troubles with the Houthi rebels around Yemen. What is interesting about this particular drone/missile strike is that it was almost completely negated by Israel’s “iron dome” which destroyed almost all the projectiles before they could reach their targets – but this success came at an estimated cost of $1,3bn. The effectiveness of drone warfare has been brought into question by this event and technical advances in the use of lasers to destroy drones. Israel is the world’s leader in anti-missile/drone technology.

Looking at the results for the first quarter of 2024, Meta not achieving its revenue growth projections had a negative impact on the S&P500. Meta fell by more than 12%. At the same time, IBM off-loaded 8% after missing first-quarter revenue expectations. Caterpillar was also down on disappointing revenue projections while Microsoft fell 4% and Amazon fell 3% in sympathy.

To date, about half of the S&P500 companies have reported on the 1st quarter. Of the companies that have reported, 77% have actual EPS above estimates, which is equal to the 5-year average of 77%. In total, companies are reporting earnings that are 8.4% above estimates, which is below the 5-year average of 8.5%.

China

The Chinese economy has been taking some strain for the past three years. The difficulties began in its property sector which appears to have had something of a “bubble”. In any event, as much as 25% of the growth in the Chinese economy is in property, so the collapse and liquidation of Evergrande with $300bn of unresolved debt has had a deep impact.

The Shanghai Stock Exchange (SSE) is a good measure of how local and international investors see the Chinese economy. As you can see from the chart below, the SSE index has been falling steadily since its peak in February 2021.

And this downward trend has taken place during a time when other international stock markets have been led by Wall Street higher. This tells us that the fate of the Chinese economy does not have a major impact on other markets. What is interesting about this chart is the trendline. Beginning from its record high, it has had two more recent “touch points” (shown by the red arrows) one in early May and one in early August 2023. In recent months the Chinese government has been trying to shore up the index by entering the market as a major buyer. This has brought the index back up to the trendline – but not yet convincingly through it. Consider the zoomed out chart of the same SSE so far this year:

Here you can see the effect of some of the Chinese government’s buying which has resulted in periods of daily stability in the price. But you can also see that the buying has only managed to stabilise the market in the short term. Left to its own devices, the market would have been unable to penetrate the long-term downward trendline to any significant degree. This shows the short-term nature of government interventions in a free market. It also shows the amazing efficacy and reliability of long-term trendlines established by multiple previous touch points.

Ukraine

The Ukraine war is really a war between NATO and Russia using Ukrainian troops and taking place mostly on Ukrainian soil. NATO is supplying arms and money but is clearly not fully committed to this war. The delay in approving the aid package from America has damaged the Ukrainian war effort and caused them to have to withdraw from some strategic locations like Avdiivka. However, it appears that Putin was not expecting the package to be approved any time soon and was making plans for a major summer offensive to take more territory. That will now probably prove to be untenable. In fact it may be Ukraine that can conduct a summer offensive. Ukraine has already received adequate supplies of ammunition and additional air defences to protect against Russian air attacks. They will soon receive F16 fighter jets and additional ATACMS long-range missiles which will probably make the use of glide bombs by the Russians impractical. In short, the approval of the aid package came in the nick of time to enable Ukraine to continue fighting and perhaps even regain some of the ground lost during the rest of this year and into 2025. It seems doubtful that Russia can continue its war effort with the losses it is sustaining for very much longer. Russia’s desperation can be seen in their recent renewed threats to revert to using nuclear weapons.

The average person living in Europe and America does not see themselves as being directly involved in a war – because they aren’t. by contrast, Putin has now switched the entire Russian economy over to a war footing with at least 40% of production now focused on military material. Europe is involved, but very far from that type of commitment. The NATO countries are approximately 20 times the size of Russia in terms of GDP – so if they were fully committed, the war would be over very quickly. In fact, if NATO just committed to spend 5% of its GDP to the war and allocate just half of its current professional standing armies, Putin would be completely overwhelmed. Putin is gambling on the fact that they are not and will never be that committed.

In our view, NATO’s arms-length involvement is becoming increasingly unworkable, and this has resulted in Ukraine being forced to make strategic withdrawals such as its final abandonment of Avdiivka. However, we believe that NATO is becoming more serious about the war and much more directly involved. The alternative is that Putin wins the war – which is essentially unthinkable from NATO’s perspective. We are expecting that some NATO countries may well commit troops on the ground in Ukraine, albeit in a support rather than a direct combat role.

Russia’s ability to refine petroleum products has been damaged by Ukraine’s drone attacks and also by the fact that Western companies will no longer assist with repairs due to sanctions. As much as 15% of the country’s refining capacity is currently not operating and although the Russian authorities say that all refineries will be repaired by June, in some cases the spare parts are not available from Russian sources. This problem must be combined with the fact that secondary sanctions are forcing India to refuse to take Russian oil exports leading to a sharp drop in exports. China is also being affected by efforts to sanction companies that do business with Russia leading to a significant decline in revenue from its most important export.

Political

The ANC’s announcement of a R3,4bn upgrade to the Durban Port can be seen as an electioneering ploy coming as it does on the eve of an election which will see ANC support fall heavily. The port is rated as one of the worst ports in the world with ships waiting as long as two weeks to dock. It is also the largest port in the Southern hemisphere handling about 32 million tons of cargo a year. The inefficiency of the port has caused many ships to bypass Durban and it has also caused significant problems for companies importing and exporting products. Furthermore, the tender for the upgrade has now run into legal difficulties with one of the other bidders, AP Moller-Maersk, claiming that their bid was superior. President Ramaphosa has set up a task team to fix the service delivery problems in Durban, particularly water, sanitation and electricity.

In another electioneering ploy the Minister of Labour, Thulas Nxesi has announced a R23,8bn boost to the Unemployment Insurance Fund’s (UIF) labour activation program. This program is designed to create jobs through private/public partnerships and the idea is to generate thousands of employment opportunities over the next three years. The funding will enable 55 projects over the next few weeks to employ as many as 700 000 people in its first phase. A second phase will then come into effect on 12th April 2024. The timing of this announcement is suspicious in our opinion.

The decision by the electoral court to overturn a decision of the IEC and allow Zuma to run for a seat on the National Assembly in the coming elections is a major blow to the ANC and a boost for the newly formed MK party. MK is expected to take votes away from the ANC especially in Natal and Gauteng. The stage now seems set for the ANC to receive the most votes, but to fall well below the 50% that it needs to control parliament. This means that it will probably have to form an alliance with one of the smaller parties to continue in power. There is also a possibility that the DA’s alliance will garner sufficient votes to control parliament. So this election is in many ways a turning point in South African politics which will have significant consequences for the economy and hence the stock market in time. The IEC is appealing the decision that allows Zuma to appear on the ballot to the Constitutional Court. There have also been some concerns over Zuma’s health after he apparently had some falls recently. The MK party denies that there is anything wrong with him – which is ironical since he is out of prison on medical parole…

In his remarks contained in Old Mutual’s integrated financial statements for the year to 31st December 2023, the chair, Trevor Manuel, draws attention to the fact that over the past decade more than R1 trillion has been withdrawn by foreign investors from South Africa’s equity and bond markets. This has obviously had an enormous impact on the economy and the quality of life for millions of South Africans and is a severe indictment of the ANC over that time. Primary causes of the withdrawal begin with the persistent loadshedding and difficulties with our rail and ports systems. But they are also related to the on-going state of corruption and state capture which continues to exist in the country. The general lack of service delivery is another major factor which results in continuous unrest and protest action. Obviously, uncertainty about the impending elections where the ANC is expected to lose control of parliament is another factor. One can only imagine what the economy would have looked like had that massive amount of foreign direct investment (FDI) remained in the country.

Home Affairs minister, Aaron Motsoaledi’s effort to force all spaza shops to register, be audited and pay tax will have the effect of discouraging if not destroying a major employer in South Africa. The informal sector has been a substantial source of gainful employment in this country for many years. Any person who has the ability can establish a shop and conduct their trade on any street corner selling whatever they think will be in demand. Forcing them to register will give an already corrupt police force a licence to seize their stock and chase them away. It will also cause unemployment to rise further.

Economy

The sharp drop-off in loadshedding in the first quarter of 2024 is having an impact on gross domestic product (GDP) growth, with the Reserve Bank now predicting growth of 1,2% in 2024 – which is double last year’s growth of just 0,6%. The reduced loadshedding may well be unsustainable as the grid remains very fragile. A major factor in the level of loadshedding has been the massive private sector investment in renewable energy. In 2023, 5,5 gigawatts of renewables, mostly solar was installed bringing the total in South Africa to nearly 7 gigawatts. This rate of installation has slowed down since loadshedding diminished, but remains high. The reduced levels of loadshedding may have a positive impact on the ANC’s prospects in the coming general election. The expected growth rate in coming years is still nowhere near sufficient to absorb the yearly growth in the labour force.

The annual inflation rate (CPI) fell to 5,3% in March 2024, down from February’s 5,6%. The month of March saw prices rise by 0,8%. Headline inflation was 5,4% - more-or-less in line with economists’ expectations. The Reserve Bank’s objective is to get headline inflation down to the midpoint of the target range of 3% to 6% - in other words, to 4,5%. Core inflation, excluding food and fuel, edged down to 4,9% from 5% in February. The expectation now is that interest rates will only come down in the last quarter of the year – in line with expected rate reductions in America. In a monetary policy report in April 2024 the Reserve Bank said that it expected inflation to come in at 5,1% this year, down from last year’s 6%. Inflation is only expected to get to 4,5% in the final quarter of 2025. Inflation in South Africa is exceptionally well controlled compared to other emerging markets. For example, Argentina is currently expecting inflation for 2024 to be 175%.

Employment statistics in South Africa are not always reliable, mostly because of the large informal sector which is a significant employer and is difficult to measure. Stats SA produces quarterly employment figures which are based on specific business samples. Its latest figures are based on a new sample, they show that the economy recovered from COVID-19 much more quickly than previously thought. Employment reached pre-pandemic levels by June 2022 and has grown by 11% between 2021 and 2023. It seems that South African businesses responded rapidly to the pandemic and then have adjusted to counter loadshedding much more effectively and rapidly than expected. The report paints a much more optimistic picture of the employment situation.

The savings rate in South Africa has always been and continues to be very low – which accounts for our relatively low growth rates, especially over the last decade. Savings provide the capital which is used in the economy to finance new projects – so if savings are low in a country, then growth also tends to be low. In any economy there are generally three internal sources of savings – that of consumers, businesses and the government. Of course, there can also be foreign direct investment (FDI) which is investment money coming into the economy from outside. In the 4th quarter of 2023, FDI was 15,5% of gross capital formation – considerably more than in 2022 when it was 3,5%. The national savings rate was 14% in 2023 down from 2022’s 14,9% - and in the 4th quarter of 2023 the rate got down to 12,7%. The average for emerging market economies is 34%. In South Africa, household savings were a miserable 1,7% in 2023 and businesses managed 15,9% while the government dis-saved by 3,6%. These figures explain our pathetic growth rates in recent times.

The ABSA purchasing managers’ index (PMI) fell to 49,2 in March 2024 from February’s 51,7 showing that manufacturing activity was lower in March. The drop-off may be due to difficulties with the Transnet rail and port system. Loadshedding was much lower in the month than in previous months. New sales orders were down and supplier deliveries were down, but sentiment towards business conditions generally improved. The employment sub-index was also up quite sharply. Overall, the PMI shows that the manufacturing sector is muddling through this difficult time in the SA economy.

Mining production increased by 10% year-on-year in February 2024, mainly as a result of reduced loadshedding. Iron ore, coal and chrome were the main contributors, with iron ore production up 43%. Global manufacturing has increased creating an increased demand for steel products and iron ore. Iron ore companies have had a major problem with the lack of adequate rail transport. Kumba which produces about half of South Africa’s iron ore exports said that problems with rail transport had cut up to 5m tons off its annual production. Manufacturing production also benefited from better availability of electricity with a 4% gain in February 2024 compared with a year earlier. The figures show that despite significant efforts by both mining and manufacturing to get away from Eskom, the consistency of their power supply remains a major factor.

The price of maize has risen 36% so far this year because of the El Nino drought conditions especially in February which has seen the expected crop size decline by as much as 25%. Fortunately, South Africa has some surplus maize from last year’s crop which means that we will not have to restrict exports or import maize. The coming year is expected to be better as El Nino gives way to La Nina and the weather turns cooler and wetter. Obviously, the higher maize price will feed through to food inflation in due course. The El Nino/La Nina cycle is expected to become more extreme in future years.

VW’s decision to invest a further R4bn into its Kariega assembly plant comes as good news for the embattled South African economy. To support the plant R130m will be invested in generators to ensure that the plant can continue production through bouts of loadshedding. The plant will build a new SUV and continue production of the Polo and Vivo products. Clearly, VW believes that South Africa will remain a viable investment destination for many years to come, despite its current difficulties.

General

British American Tobacco (BAT) is losing business to the illicit trade in cigarettes in South Africa which has ballooned. BAT is selling 40% less cigarettes today than it sold in 2020 and it has had to cut 1800 jobs. The company estimates that about 70% of the cigarettes sold in South Africa are illicit – up from about 5% in 2009. The loss of tax revenue since 2002 is about R120bn and there was R18bn lost in 2022 alone. Much of the contraband comes in from Zimbabwe. The South African Revenue Service (SARS) and the police appear powerless to stop the illegal trade.

There is little doubt now that human activities are the cause of many of many increasingly damaging weather events worldwide. The world’s average temperature reached a new record high in 2023, well above expectations, so that climatologists are struggling to predict what the effect will be. South Africa has the dubious reputation of hosting the world’s single largest emitter of greenhouse gasses – Sasol’s plant at Secunda. Our Minister of Forestry, Fisheries and the Environment, Barbara Creecy, over-ruled a decision by the National Air Quality Officer that would have forced Sasol to close the plant. The problem is, of course, that the Secunda plant produces about 150 million barrels of oil products per day from coal – which is about one third of South Africa’s total fuel requirement. This synthetic fuel plays a major role in keeping the price of petrol down in South Africa. The ANC government clearly does not want a sharp increase in the price of petrol immediately before the elections at the end of May 2024.

South Africa is moving rapidly, if belatedly, towards substantial private sector involvement in the rail transport sector. Historically, rail transport has been a government monopoly dominated by Transnet, but in recent months there has been a shift towards getting the private sector involved. The resulting rapid roll-out of rail transport could have a significant positive impact on the economy. The changes are being stimulated by the new national rail policy and changes to the Economic Regulation of Transport Bill. The private sector’s efficient operation of trains could have a massive positive impact on the economy, but this will require further substantial investment in the rail infrastructure. The maintenance backlog is estimated to be in excess of R30bn. South Africa has about 21 000km of railway lines of which about half is viable for concessioning, especially to the mining sector. The new leadership at Transnet has been a major factor. A negative is the R130bn of debt which currently sits on the Transnet balance sheet.

The Ninety-One study of inflation on the prices of a basket of products from 1986 is interesting. It shows that those products, including such items as Cross & Blackwell mayonnaise, Surf and All-Gold tomato sauce indicate that the inflation rate over that period has been about 9,1% per annum – somewhat higher than the official rate of 7,5%. The steady erosion of the buying power of the rand has direct implications for private investors, whatever the exact rate is. It means that over the long-term fixed interest investments do not even protect against inflation, let alone generate a real return after inflation. To achieve a real return (i.e. after inflation) private investors have to consider either property or equity.

Municipalities, at the end of February 2024, owed Eskom R74,5bn for electricity. This figure has more than doubled since 2021 when it was R35bn. The largest debt is with Tshwane (Pretoria) which owes R8,6bn and the top ten debtors owe roughly 60% of the total. Clearly, this situation is getting out of hand. Many of the municipalities are losing money either because consumers and businesses have chosen to deal directly with Eskom or because they have installed other forms of energy like solar power. The rising debt is making Eskom’s financial position less tenable and means that the Treasury’s R254bn bailout will probably be insufficient. In our opinion, two events seem inevitable:

1. Eskom is eventually going to go out of business and

2. the South African taxpayer is going to have to pay for their accumulated losses, including the outstanding municipal debt.

Commodities

PLATINUM GROUP METALS

The price of platinum group metals (PGM) has been declining. Since last year the basket of PGMs has fallen by about one third, led by a sharp and continuing fall in the price of palladium. Consider the chart:

Here you can see that palladium peaked in March 2022 at just over $3000 and has been falling ever since. Today it is hovering around $1000 – which has obviously had an impact on PGM producers like Sibanye and Amplats. However, South Africa is not a major producer of palladium. Most of the world’s palladium is in Russia. The primary industrial use of PGMs is in the motor industry where they are used to make catalytic converters to reduce pollution. Demand from that industry has been rising, but it is expected to fall over the next few years as more and more countries bar the production of internal combustion engines. There should be some demand from the production of hydrogen-powered fuel cells in due course. Despite the fall in the price of palladium, our view is that the commodity downturn may be close to its bottom, and we expect commodity prices to begin climbing again quite soon. If we are right, this is obviously good news for the fiscus which derives a large chunk of its revenue from mining taxes.

In the meantime, Sibanye has announced section 189 retrenchment enquiries for 3107 employees and has said that about 915 sub-contractors would be affected. In total about 4000 employees’ jobs are in danger. The problem arises in its gold mines where the company has had to reduce the value of assets by as much as R47,5bn. The company made a loss of R37bn in 2023 compared with a profit of R19bn in 2022, mainly as a result of the asset impairments. Thousands of jobs are being lost in the mining industry as commodity prices fall and loadshedding makes marginal shafts unprofitable. The trade unions pointed out that the CEO, Neal Froneman, earned a total of R300m in 2023 at the same time as he was retrenching thousands of workers. This is true, but we should also consider that without Froneman’s undisputed business expertise many of those would never have had a job in the first place.

GOLD

We have reported in the previous two Confidential Reports on the sharp rise in the US dollar price of gold since it broke up convincingly up through resistance at $2060 on 4th March 2024. The progress of gold is a direct reflection of international perceptions of global political risk. The escalating conflict in the Middle East between Israel and Iran is adding to the uncertainties surrounding the war in Ukraine to create an environment where investors are seeking the security of gold, despite the fact that it offers no return. This is an indication that international investors believe that paper assets are over-priced and risky. They are seeking to protect their wealth from a perceived drop in the value of all paper assets from equities to bonds and even hard currencies.

Historically, when the price of gold has reached significant cyclical peaks, they have often been marked by a “shooting star” formation. On 15th April 2024, I posted a tweet on “X” in which I drew attention to such a formation on that day.

Consider the chart:

Here you can see that the “shooting star” formations in gold typically occur at cycle highs. On 4th May and 1st December 2023 and then 12th April 2024 there were cycle highs marked by shooting start formations. As a technical analyst, you should be aware of the relative rarity of this formation and the fact that it normally pinpoints the top of a cycle. Two weeks have passed since we posted that tweet, and as the chart shows, gold has not exceeded the high that it made on that day, and, in fact, looks like it may be entering a correction.

The shooting star formation occurs when the price of a share, commodity or other financial indicator is pushed up by the bulls during the day’s trade to unsustainable levels. The bears then step in and bring it back to very close to its starting point. This results in a very long upward “shadow” and a relatively small “body” for the day’s candle. To be a shooting star the formation must have an upward shadow which is at least twice as long as is body – irrespective of whether the body is green or red. A shooting start indicates that the bears have won the day and regained control of the market from the bulls and it is usually followed by a downward trend – at least in the short term.

Bitcoin

For many years we have said that the price of Bitcoin can only be assessed technically - by studying its chart. It has no fundamentals and hence whatever value it has exists only in the minds of those people who buy it. It is therefore worth looking closely at the Bitcoin chart to ascertain where it is technically:

You can see here the cycle low of $38896 in January 2024, after which there was a very rapid rise to the record high of $72657 on 13th March 2024. This was slightly above the previous record high of $68536 made on 10th November 2021. That level has been the resistance which Bitcoin has so far failed to break convincingly above. From a technical perspective it has now made a “descending double top” formation followed by a third top which is below the resistance level. To us this looks extremely bearish. This type of top typically occurs when the smart money is selling out as quickly as they can while the optimism of less well-informed investors persists.

So, our advice remains what it has always been with Bitcoin – If you have them, sell them. If you don’t have them, don’t buy them.

Companies

THARISA

Tharisa (THA) is a platinum group metals (PGM) mine which also produces chrome. It is located on the south-west limb of the Bushveld Igneous Complex. It is an extremely well-managed company that has been growing its resources and beneficiating its production for many years. Obviously, it has suffered with the general decline in PGM metals prices over the past two years. We advised applying a long-term downward trendline to the chart and waiting for a clear upside break. That break came on 26th March 2024 at a price of 1405c. Since then, the share has moved up to 1575c and should appreciate further. Consider the chart:

As you can see the share has been in a long-term downward trend since April 2022, but now seems to have turned the corner and entered a new upward trend. Obviously, it is a commodity share and so depends on the internationally set prices of the commodities which it produces so this makes it volatile. In our view it is one of the better options in the mining sector.

PURPLE GROUP

Purple Group (PPE) is a trading platform and asset manager that has had some considerable success with its Easy Equities brand. In its results for the six months to 29th February 2024 the company reported revenue up 29,3% and headline earnings per share (HEPS) of 0,78c compared with a loss of 0,84c in the previous period. The company said, "Our active client base continues to expand year after year, a testament to the robustness of our platforms and the trust our customers place in us, even when economic tides are rough." We advised applying a 65-day exponentially smoothed moving average to the chart and waiting for a convincing upside break. That break came on 27th March 2024 at a price of 66c. Since then, the share has moved up to 85c. We see the share as continuing to climb. Consider the chart:

You can see here that after a “double top” in 2022, the price of PPE has been falling. The 65-day exponential moving average has proved to be a very good indicator of the various “bull traps” in the downward trend and was only finally broken in March this year. We believe that this signals the start of an upward trend.

BARLOWORLD

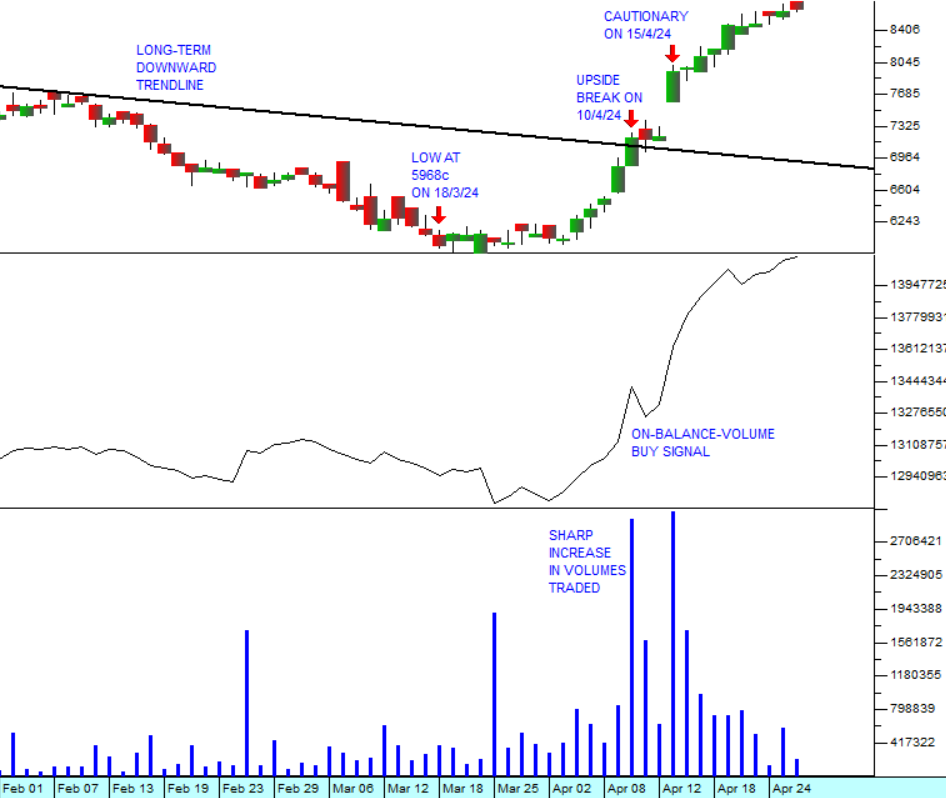

Barloworld (BAW) is an international supplier of heavy earth-moving equipment and vehicles to the mining, agriculture, infrastructure, power, automotive and logistics sectors. Its best-known brands include Caterpillar, Avis, Massey-Ferguson, and Challenger. It operates in 16 countries, especially in Southern Africa, Russia, and other emerging markets. The share has been in a downward trend since the start of 2022, partly because of the war in Ukraine and the downgrading of its Russian business. We advised applying a long-term downward trendline and waiting for an upside break. That break came on 10th April 2024 at a price of 7200c, but before that the share gave a strong on-balance-volume (OBV) buy signal. If you are not clear on OBV, re-read our lecture module.

Consider the chart:

Here you can see three charts. The top chart is a candle stick chart showing the low point for BAW at 5968c on 18th May 2024 and the break up through its long-term downward trendline on 10th April 2024 and then a cautionary announcement by the company published on 15th April 2024. The middle chart shows the OBV over the period giving a clear buying signal on 10th April 2024. The bottom chart is a histogram of the daily volumes traded showing the sharp increase in volume which also occurred on 10th April – five days before the cautionary.

Clearly something important is happening in BAW. It could possibly be a takeover bid. The insiders were snapping up any loosely-held shares they could get their hands on - well in advance of any public statement. That shows the great importance of watching the volumes traded and looking for sharp increases in volume accompanied by small rises in price which often signal insider trading.

We still do not know what is actually happening with BAW – no doubt we will find out in the coming weeks – but the charts are signalling that there is a definite opportunity for private investors to profit. The share has already gone up 45% from its low.

SIBANYE STILLWATER

Sibanye Stillwater (SSW) is a mining house which has been on a rapid acquisition trail accumulating platinum and gold mines in South Africa and America and is now broadening its scope to include base metals and minerals, especially so-called "green" metals. The company is run by Neal Froneman who is well-known in the mining industry for his toughness, expertise, and experience.

As you can see, Sibanye has suffered along with all mining companies from the decline in commodity prices which has been happening for the last few years. We advised applying a downward trendline and waiting for an upside break. As you can see from the chart, the share made a “double bottom” formation in November 2023 and March 2024 and has been rising off that support. On 28th March 2024 it broke up through its long-term downward trendline and looks to be entering a new upward trend. Of course, its progress is highly dependent on the international prices of the commodities which it produces, but if you buy it at these levels (just over 2200c), you are certainly doing much better than the institutions that were filling their pockets with Sibanye at 7500c back in March of 2022. We have great confidence in Froneman and his ability to build this company.

← Back to Articles