The Confidential Report - February 2024

America

Gross domestic product (GDP) in America in the fourth quarter of 2023 grew by 3,3% and comes on top of the whopping 5,2% growth in the third quarter. That is an extraordinarily strong growth for an economy which has interest rates up 5% and which is only expecting rates to begin falling in the second half of 2024. The average of economists’ predictions were for growth around 2% - so this number shoots the lights out.

At the same time, the US economy created 353 000 new jobs in January 2024 – a cracking start to the new year and double the average of economists’ predictions of 176 500 new jobs. Unemployment came in at 3,7% and has now remained below 4% for 24 months in a row. Investors are now no longer looking for any kind of recession because of the higher interest rates. In fact, they are not even talking about a “soft landing.” The US economy is booming and the only talk now is of how long the Federal Reserve Bank’s (The Fed) monetary policy committee (MPC) will keep interest rates at their current high levels before bringing them down. The probability of a rate cut in March has now dropped to 21% and investors are talking about rates beginning to fall on the 1st of May 2024 MPC meeting.

The stock market has made a series of new all-time record highs this year culminating in Friday’s gain of just over 1% on the S&P500. Consider the chart:

The records are being driven mainly by high-tech shares like Nvidia, Meta and Amazon. Microsoft gained 1,8% on Friday to a new all-time record high of $411.22. According to Jared Bernstein, a White House economist, the high level of job creation is powering what he describes as a “virtuous cycle” where there are an increased number of people working and their wages are beating inflation – leading to rising consumer demand. Consumer spending in America accounts for about 70% of gross domestic product.

American voters are at last beginning to give President Joe Biden some credit for what really is a remarkable economic recovery and performance. Since January 2021, the economy has created a massive fifteen million new jobs. This will undoubtedly have an impact on voting in the November elections, especially when you consider that wages have also been rising in real terms. Voters have been slow to accept the economic “miracle” which is unfolding around them, but consumer confidence is now rising steadily and jumped 13% in January 2024. The Republican’s talk of a depressed economy is beginning to look foolish. Both Nikki Haley and Donald Trump have been predicting a depressed economy. They are being proven wrong by the procession of highly positive numbers coming out of the economy. Our view is that Joe Biden will win the elections in November and beat the Republican nominee (probably Trump) by an even wider margin than he did four years ago.

The only negative in the US economy has been the yield curve inversion. Inverted yields mean that the 10-year US Treasury Bill (T-Bill) is trading at a higher effective yield than the 2-year – and that implies that investors are expecting rates to rise in the short term – which is generally recessionary. However, in the current situation, interest rates are already remarkably high and are expected to fall from current levels. The yield curve has been inverted in America for 18 consecutive months – indicating that the country would move into a recession during 2024. The originator of the concept of yield curve inversion as an early indicator of recession is Professor Campbell Harvey, an economist at Fuqua School of Business, Duke University. The last eight recessions in the US were accurately predicted by a yield curve inversion – and the recession began on average 13 months after the inversion began. So, this is a significant prediction which should be taken seriously. However, this time the yield inversion may well prove to have been incorrect in predicting an economic recession, especially given the recently announced GDP growth of 3,3% in January 2024. The yield on the 10-year T-Bill fell below that of the 2-year on 8th July 2022 and reached a maximum inversion on 8th March 2023 at -1,07%. It has since moderated to -0,33% and will probably move into positive territory relatively soon.

In our view, the bull trend on the S&P500 and in all stock markets across the world is ultimately a function of the massive quantitative easing which took place after the 2008 sub-prime crisis and was then continued and amplified in response to the COVID-19 pandemic. Trillions of dollars were literally printed and injected into the world economy, especially the US economy, and that huge injection of cash is now being felt in unexpectedly high levels of economic activity and corporate profits. At the same time, productivity has and is being boosted by radical new technologies like smart phones and artificial intelligence. We expect further new technologies to continue to boost productivity going forward - especially the advent of humanoid robots which can learn to perform mundane and repetitive tasks previously done by people. Until the productivity gains of this and other new technologies is fully discounted, we can expect the great bull market in equities to continue. Our prediction made on X (Twitter) on 25th January 2024 indicates that the S&P will rise to at least 6458 – a gain of at least 30% above last Friday’s close at 4958.61. The timing is not predictable, but we believe it will happen sooner rather than later.

China

The Shanghai index (SSU) has fallen about 40% over the past 3 years reflecting the fact that the Chinese economy is in deep trouble. Consider the chart:

This downward move is the opposite of what is happening on other world markets which are generally following Wall Street up to new record highs. There has been some scepticism over China’s claimed 5,2% growth in gross domestic product (GDP) in 2023 and its projection of 5% growth in 2024. There is a major problem in the real estate market, which accounts for roughly a quarter of Chinese GDP, and which has been experienced a 25% fall in sales for the last 7 months. New house prices are dropping and now the government is considering a $290bn bailout package for the stock market. Such a bailout is, of course, blatant market manipulation and can only halt the downward trend temporarily. The recently announced liquidation of China’s largest property company, Evergrande, with 270bn euros of debt is having a major negative impact on the SSU. Obviously, the downward trend in Chinese shares has had an impact on Tencent and hence on Prosus and Naspers. It remains to be seen whether the decline in the Chinese economy will have a negative impact on Europe and America, but so far there does not seem to be much concern on that score. Our view is that China will respond positively to the powerful growth of the US economy in time.

Ukraine

The war in Ukraine is now approaching its second anniversary. Many in the West have expressed the concern that it has reached a stalemate and that no significant progress was made last year. In our opinion, however, Ukraine has had some major achievements in 2023. Using its ingenious sea drones and long-range missiles given to it by the UK and other countries, it has virtually taken control of the Black Sea, forcing the Russian fleet out of the area, and making it possible to resume commercial exports from Odessa and other Black Sea ports. Ukraine has also taken effective control of the air with the recent downing of a Russian A50 command and control aircraft and the destruction of many Russian fighter jets and attack helicopters. The arrival of 60 F16 fighter jets from the US and various European sources means that air superiority, especially over Crimea, is a distinct possibility – and that will enable and facilitate a possible ground offensive. Ukraine should now be relatively well positioned to establish a bridgehead in Crimea. With control over the air and the sea it could well land troops on the peninsula opening a new front for Putin to worry about.

If that happens, Putin will be forced to make some very difficult decisions about where to position his forces. Right now, he has about 600 000 poorly trained and demotivated troops spread over a 1000km front line. He has been forced to shift the battered Russian economy onto a war footing with as much as 40% of GDP now devoted to the production of military equipment and ammunition. Russia is producing or repairing up to one hundred tanks a month and it is firing about five times as many artillery shells as Ukraine – but the strain on the economy is enormous. The Russians have lost at least four thousand tanks in the war so far and probably more.

By way of contrast, the motivation, training, and equipment of the Ukrainian forces means that they are being far more effective and suffering far less casualties. This was recently well illustrated by an American Bradley destroying a T90 Russian tank in a recent encounter. The Bradley is really a vehicle designed for transporting troops and should not be able to destroy a main battle tank like the T90 – so this result is a clear indication of the quality of the Ukrainian troops and their Western equipment.

To us it looks like Putin is desperately trying to hang on until the November elections in the US in the tenuous hope that Trump will win. He is hoping that the American R61bn aid package to Ukraine will continue to be held up by his Republican friends in the US congress and that Ukraine will not launch a major new offensive in the spring. The European Union’s recent announcement of a 50bn euro aid package for Ukraine is bad news for him. And we believe that Congress will not be able to hold up the US assistance for much longer.

This war has been far more protracted than anyone expected, but it now seems likely that it will reach a conclusion during 2024 and that conclusion will be substantially in line with Ukrainian aspirations.

Political

With the DA now expecting to get about 32% of the vote in this year’s general elections, there is considerable interest in whether their coalition might get enough support to control parliament. Into that mix has stepped the former chairperson of Firstrand, Roger Jardine. Jardine has apparently met with the leader of the DA, John Steenhuisen, and suggested that he would be willing to be the figurehead of the coalition. He is in favour of a “laissez faire” approach to government where the private sector leads the turnaround of the economy and government is kept to a minimum. These are radical thoughts in a country which has been dominated by the ANC for the past 30 years. Change brings with it uncertainty and that is not always good for investors or the JSE. What is certain is that the political landscape will look quite different after this year's elections. Of course, there is the possibility that the ANC is returned with a slim majority or gets sufficient support to make an alliance with one of the smaller parties to continue its dominance of parliament. Nobody can accurately predict the result – but the ANC is probably going to take a beating. Of course, a further five years of ANC dominance would be seen as highly negative by markets because of their obvious on-going incompetence, corruption, and pervasive inertia.

The passing of the National Health Insurance (NHI) bill by the National Council of Provinces (NCOP) is being lauded by the ANC as an “historic achievement,” but the reality is that it opens the way for an even worse health service in South Africa and further corrupt bureaucracy. It has been widely opposed by the business sector, and especially the medical aid providers like Discovery who claim that it is simply impractical and unaffordable. Now all that is left is for President Ramaphosa to sign it into law – and no doubt he will receive many requests from Business not to do that. But the election is looming, the ANC will want to hold the NHI up as one of their populist achievements at a time when they have very few achievements to talk about.

The decision by Jacob Zuma to support the newly formed uMkhonto we Sizwe party in the 2024 general election and the ANC’s decision to remove him from the Party will have a major impact on the ANC’s support base in Natal. In our view, the ANC was already likely to lose a large chunk of support in Natal, even before Zuma made this surprise announcement – but this will undoubtedly exacerbate the problem. Of course, it probably also means that other parties in Natal like the IFP, which is a member of the DA’s recently-formed alliance, will benefit – and that might bring the coalition within striking distance of parliamentary control.

The sudden resignation of the deputy president of the ANC’s Veteran’s League, Mavuso Msimang, comes at a critical time for the ANC immediately before the elections this year. Msimang said that the corruption within the ANC was impacting on the poorest communities in South Africa. He said the corruption was a source of “great shame” for the organization that he has been a member of for more than 60 years. The ANC has deteriorated significantly since it came to power 30 years ago and no longer has the high moral standards implemented by Nelson Mandela. A week later Msimang confirmed withdrawing his resignation after discussions with party leadership. Msimang said he has relinquished his position as ANC Veterans League deputy president and will be an ordinary member of the party.

The letter from a bipartisan group of more than two hundred members of the US congress condemning South Africa’s case against Israel for genocide in the International Court of Justice could have significant consequences for this country and its economy. Once again, South Africa appears to be endangering its relationships with its largest trading partners. From an economic perspective, taking the initiative to launch this case is potentially bad news for the country, irrespective of the merits of the case. Our view is that Israel has now carried its war against Hamas too far and Joe Biden’s support of their on-going activities there may endanger his support in the upcoming US elections. Let us hope that sanity prevails.

Economy

Gross domestic product (GDP) contracted by 0,2% in the third quarter of 2023. Growth was expected to be lower in the third quarter – but analysts were expecting +0,3%, not minus 0,2%. The difference is mostly because of problems at Transnet with the railways and ports. Obviously, loadshedding continues to play a part in restricting productivity. Manufacturing shrank by 1,3% in the quarter, Mining was down by 1,1% while agriculture fell by 9,6%. The news had a slightly negative effect on the rand, but fortunately the rand has been sustained by an international shift towards “risk-on” at the moment. Consumption, which is 66% of GDP shrank by 0,3%. In general, the figures are a sad reflection on the ANC’s desperate mismanagement of the economy and are likely to cost it dearly in the 2024 elections. Notably, the International Monetary Fund has revised its forecast for growth in 2024 to just 1% - down from its October 2023 estimates of 1,8%, citing Transnet's logistics problems and the high cost of servicing the country’s debt. By contrast, sub-Saharan Africa is expected to achieve a growth of 4,3% and the growth for the whole world is expected to be 3,1%.

The monetary policy committee (MPC) of the Reserve Bank left interest rates unchanged at 8,25% at its meeting in January 2024. This is the fourth meeting where rates have not changed as the MPC looks for evidence that inflation is “anchored” at the mid-point of the target range – in other words, at around 4,5%. The Bank expects inflation to be 5% in 2024 and then to decline in 2025 and 2026. Core inflation excluding food and fuel prices is expected to be 4,6%. The Bank also expects the economy to grow by 1,2% this year. Obviously, the Bank wants to retain attractive real interest rates in South Africa to continue drawing in foreign investment. This means that our interest rates are pegged to the levels of rates in first world countries, especially the United States.

Headline inflation was 5,1% in December 2023, down from November’s 5,5% and October’s 5,9%. Over the whole of 2023 the inflation rate came in at 6% - slightly above the Reserve Bank’s estimate. The main cause was a sharp drop in the price of fuel. That, in turn, was caused by a drop in the US dollar price of oil combined with a slightly stronger rand/US dollar exchange rate. Core inflation was 4,5% for the month and 4,8% for the whole year about half a percent up on 2022. The lower inflation figure will have an impact on the monetary policy committee (MPC) decision about interest rates, but several analysts are warning that the ANC government could go on a spending spree to try to bolster its results in the 2024 elections with lavish and unaffordable populist extravagances. Interest rates are expected to fall by seventy-five basis points beginning in the second half of 2024 – more-or-less in line with US interest rates.

The ABSA purchasing managers index (PMI) fell to 43,6 in January 2024 – down from December 2023’s level of 50,9. Business activity fell sharply, despite less loadshedding in January 2024 and new sales orders were all much lower. However, survey respondents were optimistic about the future with expected conditions in six months’ time to improve noticeably – probably because of the expected drop in interest rates in the second half of the year. The employment component rose, showing that companies are or expect to be taking on new staff.

Private sector credit extension (PCE) rose by 4,94% in December 2023 – well ahead of expectations for 4,1%. Household credit increased by only 4,3% - the lowest in almost 2 years. Overdrafts were down by 4,6% but instalment sales and leases edged up from 9.9% from 9.7%. The sharp increase in PCE shows that some consumers and businesses are using debt to finance their monthly expenses in these difficult times.

Retail sales in South Africa fell by 0,9% in November 2023 compared to the previous November. This follows October’s sales, which were down 2,3%. This implication is that Black Friday sales were lower than expected. The disposable income of households has been falling in real terms for 9 months. The decline is partly a result of much higher interest rates with the Reserve Bank raising rates by almost 5% in line with the Federal Reserve bank in America.

Mining production increased by 6,8% in November 2023 following October’s 3,6% increase and the 1,9% decline in September. Employment in the sector increased by 2% to about 470 000 and the sector contributed 1,9% to GDP growth in 2022. Platinum group metals (PGM) increased output by 15,2% and coal output was 10,6% higher. Iron ore was 20% higher while gold and manganese were down. The jump in mining production is good news for the fiscus which has been relying on taxes from mining companies to sustain increased spending. Despite the improvement, the sector remains in a downturn, dependent largely on a turnaround in Chinese demand for minerals – which may now be in doubt.

Manufacturing production increased by 1,9% in the year ending 30th November 2023 and by 0,8% in November month.

The Bankserv economic transactions index (BETI) showed that economic activity in December 2023 increased by 1,9% - due mainly to lower levels of loadshedding and lower fuel prices. Overall, the index was half a percentage point below 2022 which shows that overall growth in 2023 was flat or negative, with high interest rates and relatively high inflation. Gross domestic product (GDP) is expected to have grown by only 0,6% in 2023.

New Motor vehicle sales were 3,8% lower in January 2024 than they were in January 2023. This followed the 9,8% slump in November 2023, and was the sixth month in a row that sales were down year-on-year. Car sales were down 6,7% and exports were down 2,1%. The prospect of elections both here and in the US have introduced an element of uncertainty and both countries are labouring under high interest rates. Toyota is expecting growth of only 1,5% in 2024, mostly in the second half of the year as interest rates come down. The truck market is expected to be unchanged in 2024 from 2023. Vehicles sales are a good indication of consumer confidence – so, as 2024 begins, confidence levels are low. Higher interest rates and loadshedding are finally taking their toll as consumers battle to make ends meet and take on new debt for big ticket items. Bottlenecks at ports and on the railways have also impeded sales.

Consumer confidence as measured by the Bureau for Economic Research (BER) fell to -17 in the final quarter of the year – which is the worst level in 20 years. This means that consumers did not spend as much over the 2023 festive season as they have in the past – which is bad for retailers. Consumer spending accounts for about 65% of gross domestic product (GDP) so the decline in confidence may cause the economy to slip into a technical recession (defined as two successive quarters of negative GDP growth). This is not good news for the ANC who are facing an election this year. The drop in confidence is due to high interest rates and persistent loadshedding.

The Afrimat construction index shows that the construction sector is rebounding in South Africa. The index reached a 7-year high in the third quarter of 2023. The sector has created 145 000 new jobs this year and the consumption of building materials rose by almost 10% in the quarter. The sector has not been much affected by the problems with loadshedding and railway/port logistics as other sectors. This obviously bodes well for the economy and is a rare area of optimism in an economy that is otherwise in great difficulties.

Bank of America is predicting that interest rates in South Africa will begin falling in July 2024 and that there will be three 25-basis point cuts before the end of the year. They base this on the fact that inflation has come under control, especially with the lower fuel price. In addition, the international environment is moving towards rate cuts with America now expected to cut rates in May 2024. Loadshedding and the problems at Transnet may cause problems which interfere with the Bank of America's prediction, but the market is already pricing in ninety-four basis points of interest rate cuts in 2024. Headline inflation is expected to trend down to 5,1% by the beginning of 2024. The bank expects the US Federal Reserve Bank to cut rates by a total of one hundred basis points in 2024 – which is optimistic in our view.

The COP28 climate talks have revealed that the world is at or close to at least five “tipping points” in climate change. At 1,2 degrees Celsius above pre-industrial levels the world is still well below the limit set in 2015 of 1,5 degrees, but the effects of continued greenhouse gasses are having a greater and greater impact while efforts to shift to renewables have been insufficient. A new report from 200 climate scientists shows that the ice sheets in the Antarctic and Greenland are in danger of melting far more quickly than previously estimated because of warmer sea temperatures – and that these events are now irreversible. There is no “business-as-usual” path forward any longer. To be effective, change has now got to be radical to avoid a climate catastrophe. In our view, climate change is going to become an increasingly important factor in the world economy over the next few years and beyond. It will begin to impact directly on the profits of listed companies all over the world. Investors should begin to consider the vulnerability of the shares that they select to the various impacts of climate change. The experts tell us that emissions must fall by 43% in the next six years to have any chance of avoiding the 1,5 degree limit – and that appears highly unlikely to us. It is notable that the conference is being held in the United Arab Emirates (UAE), a major producer of oil and gas. OPEC members have resisted an effort to get the phasing out of fossil fuels included in the final COP28 agreement. Notably, OPEC believes that oil demand will increase from current levels around 102m barrels per day to 111,6m by 2045. The conference did, however, conclude with an agreement to gradually phase out the use of fossil fuels for the first time – but that looks like too little, too late.

The Minister of Trade and Industry said that with South Africa’s new electric vehicle (EV) policy that the country could be making electric vehicles within 3 years, but it could take a further 6 years before local consumers are incentivized to buy them. Eventually, the government sees the country moving away from internal combustion engines to EVs – perhaps by as late as 2032. For EVs to be produced, South Africa will have to develop a battery industry. Fortunately, most of the raw materials required for the production of batteries are available in the country.

The government and provinces are R11bn behind in their payments to suppliers. They are supposed to pay all supplier companies on 30 days from invoice, but the combination of incompetence, non-existent internal controls and general mismanagement means that 117160 invoices have not been paid which are older than 30 days. This obviously puts enormous pressure on supplier companies and even causes some to file for bankruptcy. The situation has worsened by 12% since the first quarter of 2023. Only 37,5% of national departments were able to comply with the 30-day payment requirement. The department of health was one of the worst offenders. 38,8% of the outstanding invoices were from Gauteng province alone.

The international ratings agency, Fitch, says that when the South Africa’s membership of the African Growth and Opportunity Act (AGOA), which expires in September 2025, will be renewed on better terms for South Africa than it currently enjoys. The agency gives SA’s new membership a 65% probability of being renegotiated on improved terms. This is since South Africa is Africa’s largest single exporter to the US and the US is the second largest exporter to South Africa after China. About 9% of SA’s total exports go to America and only about 20% of these benefit from AGOA, meaning that AGOA affects less than 2% of SA’s annual exports worth around $3bn. The decision by the SA government not to host Vladimir Putin in person at the BRICS conference in August 2022 was a major positive factor.

The Rand

Rand Merchant Bank (RMP) predicts that the rand will strengthen to R17.75 to the US dollar by the end of 2024 and most SA asset managers expect the rand to reach R17.30. Obviously, the outcome of the general election in South Africa this year could have a major impact as will the on-going loadshedding and problems at Transnet. Interest rates are expected to begin falling in South Africa later this year and in line with falling rates in America and elsewhere. The S&P500 is making new all-time record highs almost every day now and sentiment is definitely “risk-on”. That is having a strong positive impact on emerging market currencies and especially the rand. Consider the chart:

The chart shows that the rand has been weakening steadily against the US dollar over the past two-and-a-half years, since June 2021. The weakness would have been worse if international sentiment had not been as positive as it has been, especially since US equity markets rose to new highs.

In our view, the rand is probably a little oversold and might see some strength against hard currencies during this year, but over the medium to long term, more weakness appears inevitable. The sudden weakness on Friday afternoon last week is an indication that international sentiment may be turning against emerging market currencies after a period of relative stability.

Eskom

It is disturbing that the 2023 Integrated Resource Plan (IRP) has been described by experts as “...an admission of failure by the government in its efforts to eliminate loadshedding”. The report, published by the Department of Mineral and Energy Affairs at the beginning of January 2024, replaces the 2019 IRP. It apparently “lacks detail” and “fails to provide solutions to the energy crisis”. The inability to solve the energy problem, which has been in existence since the start of loadshedding in 2008, has become a major problem for the ANC and may well cost it its majority in parliament in the coming elections. The voting public will be disappointed to learn that the report suggests that loadshedding will continue for at least the next four years. Notably, Eskom’s energy availability factor (EAF) continued to decline in 2023 reaching a new low of 51% by year-end and averaging 54%, sharply lower than the previous year and the lowest average since the ANC took power 30 years ago. It is a damning indictment of the ruling party.

Eskom’s actual production of electricity in November 2023 was down 3,3% from November 2022. There were 630 hours of loadshedding compared to 263 hours in October. The energy availability factor (EAF) was 53% of installed capacity with 8,4 gigawatts of power under planned maintenance and 13,4 gigawatts off-line due to breakdowns. The Reserve Bank says that loadshedding may have reduced gross domestic product (GDP) growth by as much as 2% in 2023 – which compares with 2022 loss of 0,7%. The bank expects that 2024 will be better at a loss of 0,8% but we are not confident. Deloitte estimates that power outages over the past 14 years have cost the country as much as R3 trillion. It is becoming clearer that loadshedding and all its ramifications will be the major factor in the 2024 elections.

Our esteemed Minister of Mineral Resources and Energy, Gwede Mantashe, has said that his ministry is completing the seventh bid window for independent power producers’ (IPP) renewable energy projects. The sixth bid window was hampered by a lack of access to the grid and so ended up only getting about 1 gigawatt (gig) out of an original call for 5,2 gigs. The seventh bid window is looking for five gigs. So far, since its start, the IPP program has resulted in the procurement of about 12000MW, but only half of that is actually producing power. South Africa is moving steadily towards renewable energy and away from coal, but the process has been impeded by government red tape and mismanagement.

On a positive note, the National Energy Regulator (NERSA) registered more than 400 projects in 2023 with a combined generation capacity of over 4,5 gigawatts which is nearly three times what was registered in 2022. Altogether, South Africans imported R3,3bn worth of solar panels, inverters and batteries in the 11 months to end-November 2023. Eskom records show that private people and companies doubled their installations of solar powered systems to a total of 5,2 gigawatts in 2023. The investment has had a positive impact on the banking sector which has financed many of these systems. This is especially true of ABSA which has financed the lion’s share.

The amount of power being produced by solar panels in South Africa almost doubled to about 4,8 gigawatts during the year to 31st August 2023. About two gigawatts of solar panels have been installed during the 12 month period. Rooftop solar power is accelerating as businesses and consumers seek to get away from Eskom’s increasingly unreliable and expensive offering. The National Energy Regulator (NERSA) has approved nine hundred megawatts of power from ninety-eight projects in the 3 months to 30th September 2023. Only two of these projects involve battery storage.

In its results for the six months to 30th September 2023 Eskom reported that its sales of electricity had fallen by almost 6% when compared to the same period last year. This was due to the rapid implementation of alternative power solutions by the private sector, especially businesses. Despite the drop in demand, the number of days with loadshedding increased to 183 from last year’s 102 and the energy availability factor (EAF) dropped to 55% from last year’s 59%. The company revenue increased despite the lower sales because of the 18,65% price increase which it put through. At the same time its debt rose from R424bn to R443bn. Municipalities owed Eskom R70bn by 30th September 2023.

Transnet

The next state-owned enterprise (SOE) to require a substantial Treasury bailout is now obviously Transnet. It currently has debt of R130bn which is costing more than R1bn a month to service. The ratings agency Fitch has said that they expect the Treasury to inject R50bn sometime in the next 2 years to alleviate the problem. Providing a government guarantee will not solve the problem because the interest payments on the existing debt are already unsustainable. Like Eskom, Transnet has built this debt up through a combination of corruption and mismanagement of resources – while at the same time performing its allotted tasks with less and less efficiency and at greater indirect cost to the economy. Like Eskom, Transnet is too big and its function to vital to the economy to allow it to fail. This puts the Minister of Finance in an extremely difficult position because it makes his debt consolidation objectives less attainable. Transnet made a R1,6bn loss in the six months to 30th September 2023 and requested a R47bn injection from the government.

In 2023 Transnet delivered 48m tons of coal to the Richards Bay Coal Terminal (RBCT) – well below its contracted level of 60m tons. Prior to 2020 the state-owned enterprise (SOE) regularly delivered more than 70m tons to RBCT and that terminal has the capacity to handle up to 90m tons. In effect, RBCT is now operating at close to 50% of its capacity. The problems are security of Transnet’s railway infrastructure which is constantly vandalised and the subject of theft, the obtaining of spare parts from China for its locomotives and maintenance of the rail infrastructure. Obviously, Transnet’s poor performance is impacting on the coal industry and forcing them to make much greater use of road transport.

Transnet has a new acting CEO, Michelle Phillips, who is doing a good job and has been well-received by the business sector. The company has been given a R47bn guarantee facility by the Treasury to enable it to raise additional cash to meet its immediate debt obligations and to improve its infrastructure. The CEO and CFO of Transnet both recently resigned, and the company has a massive problem with its rolling stock because it cannot get spare parts from the Chinese company that supplied more than 1000 locomotives. In many ways, the future of our exports hangs in the balance as Transnet desperately tries to re-establish the movement of raw materials to ports and then onto ships. Many ships are now bypassing our ports because they cannot afford to be held up for as much as two weeks to take on cargo. Pravin Gordhan, Public Enterprises minister, says that Transnet had 4600km of copper cable stolen in three years to October 2023 and about 3600km of its railway tracks had fallen into disuse. The rolling stock situation has become so bad that the coal industry has now stepped in to pay for parts for two hundred locomotives that Transnet has standing idle.

Companies

From its cycle low on 27th October 2023, the JSE Overall index has been trying to follow Wall Street up towards a new record high. This means that there is considerable bullishness in the market and many of our shares have been rising strongly. We have covered some of these in our articles this year, including CA Sales and 4Sight .

ANGLOVAAL INDUSTRIES (AVI)

Anglovaal Industries is an iconic South African manufacturer of food products, clothing and cosmetics. It has many well-known brands such as I&J fish, Five Roses tea, Frisco, Provita and Yardley. An investment in AVI is an investment in South Africa and exposes the investor to the level of consumer spending in this country. From its peak in February 2018, the share has been falling and we advised waiting for it to break up through its long-term downward trendline. That happened on 8th November 2023 at a price of 7418c. It has subsequently moved up to 8565c – a gain of 15,4% in just over 2 months. We expect it to continue rising, especially given its recent estimate that headline earnings per share (HEPS) will rise by between 16% and 18% in its results for the six months to 31st December 2023. Consider the chart:

MIX TELEMATICS (MIX)

Mixtel is one of two vehicle tracking companies listed on the JSE, the other is Karoo. It has an international business offering a vehicle tracking and monitoring service to companies and individuals. In its quarterly report on the 3 months to 31st December 2023 the company said that it had added 52400 new subscribers to bring its total number of subscribers to 1 142 000. Revenue was up 6% and earnings before interest, taxation, depreciation and amortisation (EBITDA) was up 13% on an EBITDA margin of 24.4%. The important point about this company is that it has an international annuity income which is rising steadily. It is a service company with almost no working capital and a steady debit-order income. This makes it a very low risk investment. From its low point of 380c on 31st October 2023, the share has been rising steadily. We added it to the Winning Shares List on 28th December 2023 at 590c and it has since moved up to 735c – a gain of 24,5% in just over 5 weeks. Consider the chart:

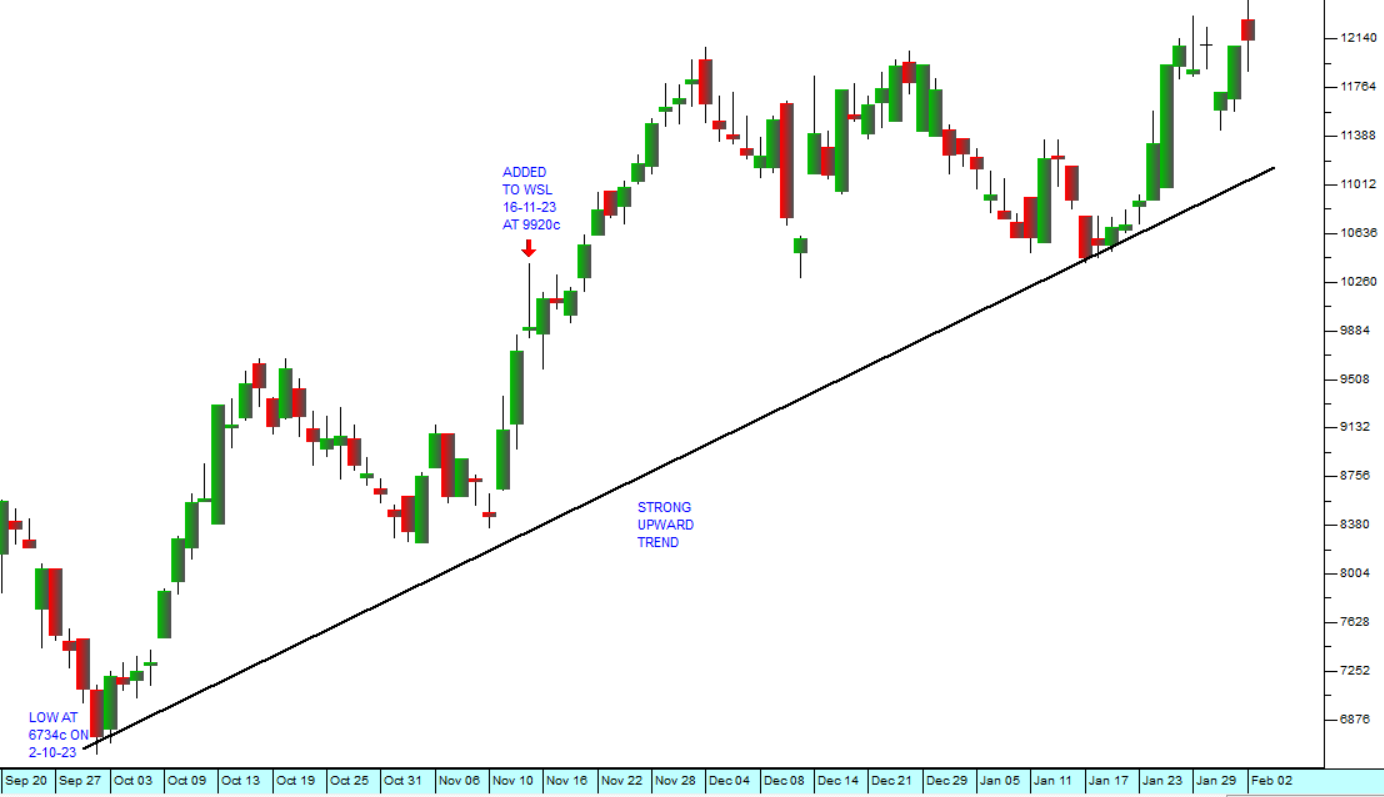

HARMONY GOLD MINING (HAR)

Harmony Gold is a relatively marginal gold mine. This means that its cost of producing gold is relatively close to the current gold price – which means that it operates on thin margins which can be easily wiped out or doubled by movements in the gold price – or the US dollar/rand exchange rate. In its recently announced update, the company said that it was producing gold at an all-in sustaining cost of between R830 000 and R855 000 per kilogram. At the current price of gold and rand/US dollar exchange rate the price of one kilogram of gold is R943 379.34 – which means that the company has a margin of about R100 000 per kilogram. However, if the gold price falls or the rand strengthens against the US dollar then that margin could be cut in half or even wiped out completely. This potential volatility in the company’s profitability is reflected in its share price – which makes it a relatively risky investment. However, right now, with the relative stability of the rand and the rising dollar price of gold the share is doing well. Consider the chart:

You can see here that Harmony made a low of 6734c on 2nd October 20234 and has been rising in a volatile upward trend ever since. We added it to the Winning Shares List on 15th November 2023 at a price of 9920c per share and it has since risen to 12140c – a gain of 22.38% in 10 weeks. It may go further and certainly it offers the investor a hedge against any potential weakness of the rand – but a strict stop-loss must be maintained.

BELL EQUIPMENT (BEL)

Bell (BEL) is a manufacturer and distributor of heavy equipment, earth-moving equipment to the mining construction, agriculture, and waste management industries. As such it is impacted by the climate-driven vagaries of the agricultural sector, the volatility of the mining industry and the prospects of the construction business. Despite this, Bell has proven to be a good hedge against the lock-downs of the COVID-19 pandemic and relatively immune to the problems associated with loadshedding. In a recent trading statement for the year to 31st December 2023 the company estimates that headline earnings per share (HEPS) will rise by 59% to at least 750c per share. This puts the company on a P:E of 3.82 – which is very attractive when compared to the JSE’s average P:E of 10,58. We added Bell to the Winning Shares List on 27th October 2023 at a price of 1875c per share. It has since moved up to 2315c – a gain of 23,5% in just over 3 months. Consider the chart:

This shows that, after an initial very strong upward trend, the share has been moving sideways since mid-November 2023. We believe, however that it will continue its steady upward trend in due course.

CALGRO-M3 (CGR)

Calgro M3 is a property developer which has diversified into developing memorial parks. Most of its income comes from developing residential units and selling them at an average margin of about 22%. In its results for the 6 months to 31st August 2023 the company was able to report that it had handed over 949 properties and had a further 2118 properties under construction. Revenue was up 13,5% and headline earnings per share (HEPS) increased by 38,4%. Clearly this is a property company which has developed a very effective sales route which generates good cash flows and is profitable even under the difficult economic conditions which pertain in South Africa. The company has been actively engaged in buying its own shares back in the open market. During the six months the company bought 22,6m shares back at an average price of 263c per share – well below the current price of 494c and against a net asset value (NAV) of 1199c per share. In our view this share is something of a bargain even at current prices. Consider the chart:

← Back to Articles