The Confidential Report - April 2021

America

The S&P500 index closed above 4000 for the first time on Thursday 1st April 2021 at 4019.

.png)

You can see the impact of the COVID-19 V-bottom, which we regard as an extraneous non-economic factor, and the subsequent acceleration of the S&P. Obviously, the rapid roll-out of vaccines in First World countries will result in the steady elimination of the economic impact of the virus.

Large round numbers like 4000 often present a psychological barrier resulting in considerable “backing and filling” (visible over the last three months) before they are convincingly broken.

The immediate driver for the market was the announcement of President Biden’s latest stimulus package in which the government will spend around $2 trillion on infrastructure over the next 8 years. This will be funded by a rise in the corporate tax rate to 28%. The stimulus comes on top of Biden’s initial $1,9 trillion package which took the form of $1400 cheques sent out to every American.

The S&P was primarily driven by high-tech stocks with Microsoft announcing a massive $22bn deal with the US military to supply 120 000 devices over the next 10 years. The unemployment rate has now fallen to around 6% and is moving down rapidly with the economy creating more than 600 000 jobs a month.

The unprecedented fiscal stimulus must be seen in the context of the massive monetary policy stimulus which has been on-going since the 2008 sub-prime crisis and which forms the foundation of the record 12-year bull trend in shares. This further stimulation of the US economy is made possible by the low levels of US and world inflation – and that, in turn, is partly a function of much lower energy prices. While North Sea Brent oil has ticked up in recent months, it is still trading at around half the price that it was at ($125) in March 2012. Consider the chart:

.png)

You can see here the fall in the oil price from the high of $126 in March 2012, culminating in the sell-off in March 2020 as a result of the pandemic. Since then the oil price has bounced back, but hit resistance at around $70 per barrel. In the longer term, the rapid adoption of electric vehicles in the major economies of the world will continue to exert downward pressure on oil prices going forward.

In the document Our Background Approach we have outlined how this type of continuous stimulation of the US and world economies, combined with lower energy costs, would result in an exponential rise in share prices on all stock markets – including the JSE.

Our expectation is that the S&P will continue to rise, although some sort of correction becomes more likely as it goes higher. Usually, a psychological resistance level (like 4000 on the S&P) later becomes a support level for a following correction. But the breaking of this level is confirmation of the underlying massive 12-year long bull trend which we think still has some distance to run.

Political

The student riots at Wits and elsewhere are once again pressurizing government to invest further in higher education. This year, with the budget constraints, there have been cutbacks in the Department of Higher Education which have reduced student subsidies. In the past, student unrest could be seen as one factor contributing to the fall of Jacob Zuma as President. With the municipal elections on the horizon, it is possible that the Treasury will have to find the additional funding demanded by students. In the meantime, it is a further headache for an already stretched administration. Notably, Ace Magashule, ANC Secretary General, chose to march with the students.

Ex-president Jacob Zuma’s refusal to participate in the Constitutional Court hearing into his contempt of court charge must surely result in his imprisonment. The charges seem very simple and clear – he directly disobeyed a Constitutional Court order to appear before the Zondo Commission. Notably, President Cyril Ramaphosa has publicly said that he will be appearing before the Zondo Commission in April. The Constitutional Court’s decision on this matter will obviously have critical political ramifications. If Zuma does not receive an appropriate sentence, then the authority of the Constitution and the Constitutional Court are brought into question. If he is appropriately sentenced then there may be unrest and it could impact on the coming municipal elections.

The parliamentary vote to establish a committee to investigate the Public Protector is the next step in the battle within the ANC between the Zuma and Ramaphosa factions. If the committee recommends her removal it will then take two-thirds of parliament to put that into effect. With the support of the DA, it is possible that the Ramaphosa faction will muster sufficient votes to achieve that. If they do, it will be a major psychological victory for Ramaphosa. Ace Magashule has said publicly that those ANC parliamentarians who voted against investigating the Public Protector, and in opposition to the party’s requirement, did the right thing.

The ANC’s National Executive Council (NEC) debated the “step-down” rule that was established by them in February 2021 and how it would be implemented in the case of Ace Magashule. The local government elections which are due to take place in 2021 are at stake. Ace Magashule has apparently got some considerable popularity at a grass roots level. If he is forced to step down, then it may harm the ANC’s position in those elections. The battle lines between the Ramaphosa camp and what is being called the “radical economic transformation” camp are being drawn. The latest NEC meeting was inconclusive and no decision on Magashule was taken. This may force the NEC to move away from its tradition of always reaching a consensus by taking a vote on the issue.

Economy

There has been much talk about a third wave of the pandemic which is expected to begin as early as Easter this year and will probably dominate the winter months. Gatherings of people over the Easter weekend as well as further travel between provinces could easily result in a rapid spread of the virus. The vaccination program, so far, appears to be somewhat slower than the government’s projections and the goal of vaccinating 40 million people by the end of 2021 is now clearly unattainable. The third wave is expected to result in 25% more hospital admissions than the second wave. The slower implementation of vaccines has been accompanied by the emergence of a new variant (501Y.V2). The government was urged to return to restricting alcohol sales to Mondays to Thursdays, returning the curfew to between 10pm and 4am and reducing the number of people allowed at a gathering from 250 to 100. In the end they decided to only ban alcohol sales over the Easter weekend. The average number of new cases has dropped from around 18500 to around 1200 since January 2021 but more than 52 000 people have died from the disease so far. Just over 300 000 health workers have been vaccinated so far.

The Consumer Price Index (CPI) came in at 2,9% for February 2021 – down from January’s 3,2% and below the low point of the Reserve Bank’s target range of 3% to 6%. It was also below the average prediction of analysts, which was 3,1% - so it was somewhat better than expected. It is unlikely to result in any further decline in interest rates, however. The drop was caused by a lower-than-expected increase in the cost of medical insurance at 4,7% compared to the average of 9%. The price of oil has been rising this year and ultimately that must negatively impact the level of South African inflation. The stronger rand has, to some extent, mitigated that effect. Electricity also rose by 15,6% from the 1st of April 2021 and that will increase inflation later on this year. Interest rates were left unchanged by the Monetary Policy Committee (MPC) on 25th March 2021 and are expected to remain unchanged until the beginning of 2022. The MPC expects headline consumer inflation to average 4,3% in 2021 – which means that they are anticipating higher levels of inflation later in the year.

Old Mutual has joined Goldman Sachs in predicting that South Africa’s GDP growth will be much higher than is predicted by the consensus of economists or the Reserve Bank. Old Mutual is predicting a 5% growth off a low base against a consensus of economists at 3,5%. Our feeling is that Goldman Sachs and Old Mutual are probably right. They base their prediction on the growth of the world economy and the continued rise in the demand for base metals and precious metals. They also assume that South Africa will benefit from significant Foreign Direct Investment (FDI) looking for the high real rates of return offered by our government bonds. If growth is going to be higher than was forecast in the budget, then tax collections will also be better, meaning that the government deficit will be lower as a percentage of GDP than has been forecast. We have already seen R100bn of extra tax collections above the budget predictions as a result of the rise in precious metals prices and there is no reason to believe that that surplus will not continue through the year. The 7% contraction in 2020 was slightly better than expected with a strong 6,3% jump in the last quarter. Despite this it will take some years for the economy to return to the levels it was at prior to the pandemic.

Tax collections are even better than was projected in the recent February budget. SARS has collected about R30bn more resulting in the shortfall (from the October 2020, budget) being reduced from R213bn to R183bn. This will result in a slightly lower debt to GDP ratio. We expect that collections will continue to be good as commodity prices remain high and the economy recovers leading to more business recovery and higher personal incomes. This means that the current budget projections are probably too conservative.

Vulindlela (which means “open the road” in Zulu) is a project established by Finance Minister, Tito Mboweni, to accelerate delivery on key government functions and to clear away administrative and bureaucratic impediments to economic growth. To date the project has been successful in a number of areas, including making it easier for companies to engage in their own electricity generation, the freeing up of broadband and the easing of restrictions on tourism and immigration of skilled people. Clearly, this is a vital function in a country which has plenty of wonderful plans, but constantly falls short on implementation.

Expropriation of land without compensation is once again becoming a negative in the South African economy. The international norm is that expropriation can only take place if adequate and fair compensation is provided. To the extent that South Africa departs from this norm or is expected to depart from it, foreign direct investment (FDI) here will be curtailed. Obviously, the racially skewed land distribution in South Africa has its roots in history but adjusting it should not be seen to significantly interfere too radically with ownership rights, because that introduces an element of uncertainty. Uncertainty will scare off international investors and result in lower growth and curtail job creation. So far, efforts to redistribute land have been characterized by a sharp reduction of agricultural productivity and the usual corruption. Probably, a gradual shift towards system of long-term (99 year) property leases for all agricultural land would be the most effective and least disruptive approach.

Credit extension came in below most analysts’ expectations in February 2021 – showing that consumers and businesses are not taking on additional debt, despite the exceptionally low level of interest rates. Private sector credit extension in February was just 2,6% compared with January’s 3,3% and economists’ forecast of 3,4%. This shows that South African’s are still hoarding cash and repaying debt in a situation which has considerable uncertainties. Nobody knows if there will be a third wave of the virus with concomitant lock downs and a further restriction of economic activity. Those businesses and households that have survived are naturally conservative and are reducing expenses wherever possible while repaying debt. In our view, this attitude will probably continue for the rest of this year but will begin to improve as the year progresses. Much will depend on the perceived progress of the vaccination program and whether there is a third wave. The latest South African Reserve Bank (SARB) bulletin shows that household consumption shrank by 5,4% in 2020 while the level of household debt fell as a percentage of disposable income from 5,8% to 4% as households cut expenses and repaid debt.

The annual Bank of America investment conference at Sun City surprisingly had a record attendance this year. Investors generally regarded South African assets as relatively cheap and anticipated a 50% jump in earnings from last year’s depressed figures. 40% of attendees were from the America’s while 50% were from the UK and Europe. A major motivating factor was the high levels of commodity prices which began a bull run at the start of 2016. So long as commodity prices continue to rise, the South African economy will attract overseas investment and the rand will remain relatively strong.

The Rand

The rand has been in a strengthening pattern for the past year, and we believe that pattern will continue. Obviously, it is volatile and subject to various international forces (such as the alternation between “risk-on” and “risk-off”). Nonetheless, the underlying trend is becoming clearer. There is substantive support at about R15.30 to the US dollar and some resistance consistent with the lower rising trendline at about R14.40. We believe that the rand will strengthen through this level and go on to test the previous cycle low at just under R14.

.png)

As always, the rand is a very heavily traded emerging market currency which is a favourite among international currency traders. Any movement in international sentiment towards emerging markets tends to impact the rand directly. Sometimes these shifts in sentiment have little or nothing to do with the South African economy but rather reflect perceptions of emerging markets generally.

We believe that investors should probably take the position that the rand, while volatile, will gradually strengthen over time, now that the US elections and the pandemic are receding as major risk factors in international markets.

State-Owned Enterprises

The Deputy-President, David Mabuza’s remarks in parliament regarding Eskom are noteworthy. He suggests that since Eskom is now producing less electricity than it was in 2008, the doubling of its staff compliment cannot be justified. How right he is! Efforts to reduce the staff at Eskom have always run foul of the unions and so have been abandoned by the ruling party as being too politically sensitive. Now at last it appears that the ANC are beginning to understand the relationship between productivity and employment. Eskom has 46000 employees costing about R32bn per annum – and it is known to be heavily over-staffed especially when compared to electricity utilities of other countries. Mabuza says the intention is to reduce Eskom’s staff by 6000. Clearly, the unions will not stand by idly while this takes place – if it ever does.

The statistics on load-shedding in 2020 are a source of concern. The Council for Scientific and Industrial Research indicates that as much 10% of power production was affected by load-shedding. This obviously has a huge impact on productivity and ultimately the level of GDP and unemployment. The statistics showed that about 10% of South Africa’s power is now provided from renewable sources (variable or otherwise), 83% from coal and about 5% from nuclear. It is also apparent that South Africa’s fleet of coal-fired power stations are gradually failing and producing less and less electricity. Demand for Eskom’s electricity has also been declining about 1% per annum as more and more consumers and businesses seek to implement alternatives. The 15,63% increase in Eskom Tariffs from 1st April 2021 will accelerate the move away from its product. From our perspective it appears that Eskom is gradually, but inexorably dying.

Eskom CEO, Andre de Ruyter has indicated that planned maintenance will take priority over the supply of electricity to the economy. In other words, the planned maintenance program will continue even when that means having to resort to load-shedding. Over time, this will result in the entire fleet of power stations becoming more reliable, but in the short term it means more pain for users. He also said that South Africa should expect some level of load shedding to continue sporadically for a further five years. Eskom is catching up with years of deferred maintenance. De Ruyter did however say that the risk of load-shedding would decline after September 2021. Clearly, the reliability of supply is a critical factor for the economy and will encourage more industries to seek their own solutions and move away from Eskom. One major improvement was the availability of coal stocks which have reached 52 days (excluding Medupi and Kusile) thus eliminating one of the major causes of load-shedding in the past. What seems to be clear is that de Ruyter is steadily moving Eskom onto a more businesslike and efficient footing. Despite this, it appears to us, that this behemoth is almost beyond saving.

The steady rise in electricity prices combined with the unreliability of supply have had the effect of virtually stopping new mining projects in South Africa and endangering the viability of more marginal operations. In the short term the rise in commodity prices since 2016 has protected the industry to some extent, but funding for new projects has all but dried up. The latest 15,6% price implemented from 1st April 2021 may push some mines to the edge of closure. Electricity prices have risen about 700% in the last 12 years. They now make up about a quarter of the costs of a gold mine and about 13% of a platinum mine, on average.

The retrenchment of 621 staff from the SABC despite union opposition and opposition from the Minister of Communications may indicate a new trend in dealing with state-owned enterprises (SOE). The SABC’s largest expense is its 3000 highly paid staff, many of whom are redundant. The reduction in the salary bill will go some distance towards making this SOE self-sustaining. The retrenchment may also set the pattern for other SOE's like Eskom, which are clearly over-staffed and relying on government grants to stay afloat.

The Land Bank struggled to restructure its debt of R40bn before the end of March 2021. It had to meet a court ordained deadline to repay R400m to Standard Chartered by that time after defaulting on repayments a year ago. The bank’s creditors have expressed frustration with the slowness of the negotiation process which has dragged on for almost a year. The Treasury made available R7bn in the February 2021 budget to deal with the Land Bank’s most pressing needs. The Land Bank’s debt is no longer rated by Moody’s because it says it no longer requires a rating, but this is contrary to what was previously agreed with creditors. The negotiations between the Land Bank’s creditors and the Treasury seem to be becoming more and more difficult. The “crisis” has been in process for more than a year and there is no solution in sight yet. Creditors complain that each proposal is worse for them, increasing their risk. Obviously, how the Land Bank debt position is resolved will have an impact on perceptions of how the Eskom debt problem will be dealt with. The Treasury is obviously short of funds and looking for the best solution, but it must be one which the creditors can accept.

Companies

HAMMERSON

Hammerson is a real estate investment trust (REIT) which owns shopping centres in the UK. It is listed on the JSE and the LSE. It recently gave a strong on-balance-volume (OBV) buy signal between the 23rd of February and the 16th of March 2021. Volume traded increased sharply with small increments in price – which indicates that the “smart money” is buying the share on weakness. Consider the chart:

.png)

With the double impact of Brexit and the pandemic, this share has become cheap enough to be bought out, probably by JSE-listed Resilient. Resilient’s CEO, Des de Beer, is also a director of Hammerson and Lighthouse, while Lighthouse owns 15% of Hammerson. Maybe something is happening?

AFRIMAT

Ten months ago, in May 2020 during the worst of the COVID-19 pandemic and lockdown, we suggested that construction materials and mining company, Afrimat, was a good buy at 2900c. Since then, the share has risen to 4645c – a gain of 60% in ten months.

The reason for this rise is that Afrimat made the shrewd decision to move away from the construction industry and get in the mining of base metals by buying a defunct iron ore mine for R450m and then spending a further R450m to bring it back into operation. That mine, Demaneng, is now a steady generator of profits. Consider the chart:

Here you can see that the smart money has been steadily accumulating the share since May last year.

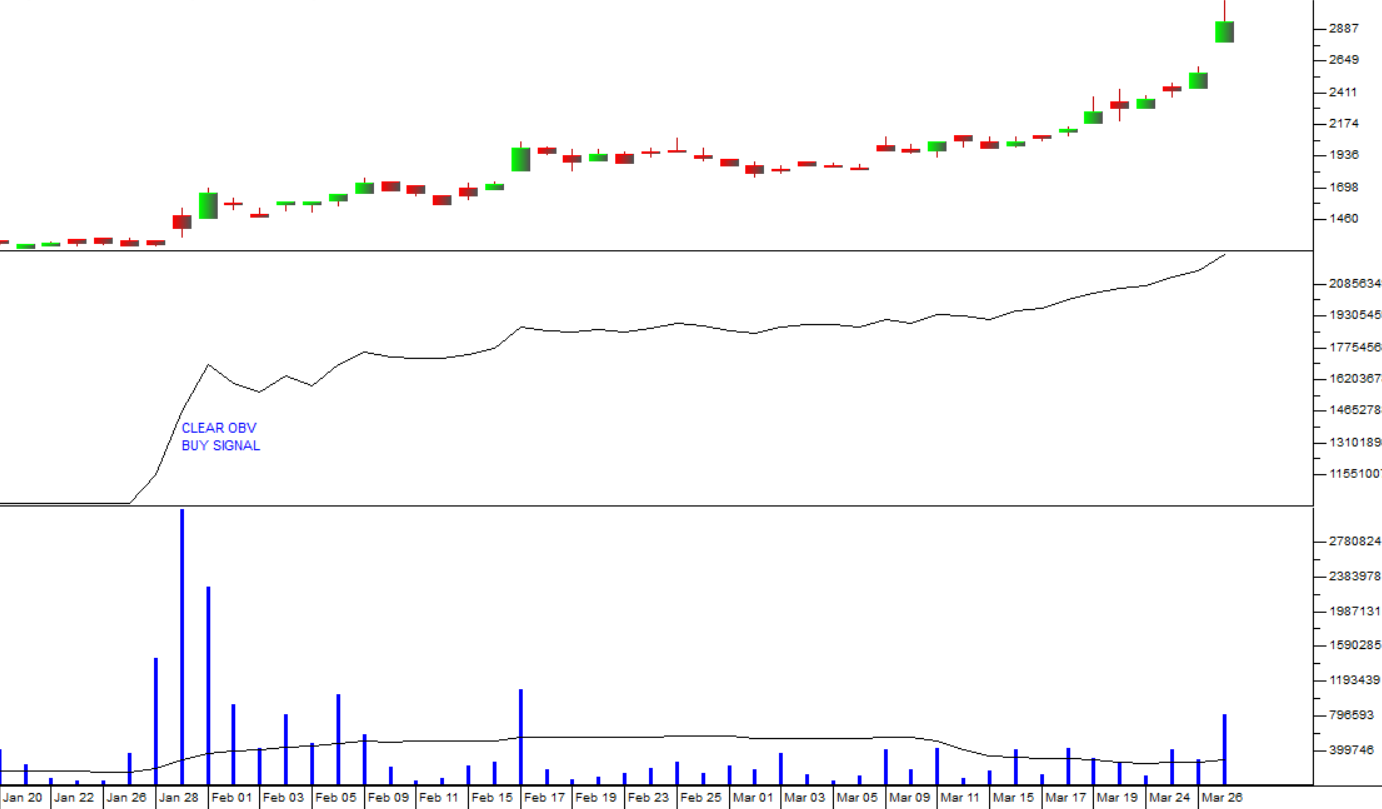

RENERGEN

Renergen is a natural gas and helium exploration company which has just announced a very promising find of helium at its P007 test well. The share price rose by 15% on the day of the announcement. What is interesting is that this share gave a very clear strong on-balance-volume (OBV) buy signal a month ago on 1st February 2021. Consider the chart:

You can see here that the clear buy signal given when the OBV chart spiked up at the beginning of February 2021. That was followed by a period of sideways/upwards movement during February and March – and then a spike upwards when the announcement was made 29th March 2021. If you had bought the share on its OBV buy signal on 1st February 2021, you would be up 77% in just two months. The OBV principle is that “volume leads price” – in other words, when something is going on in a share, the volume will spike up accompanied by small increments in price. This causes the OBV chart to move up sharply giving a buy signal – usually well before the news is made public – as in this case.

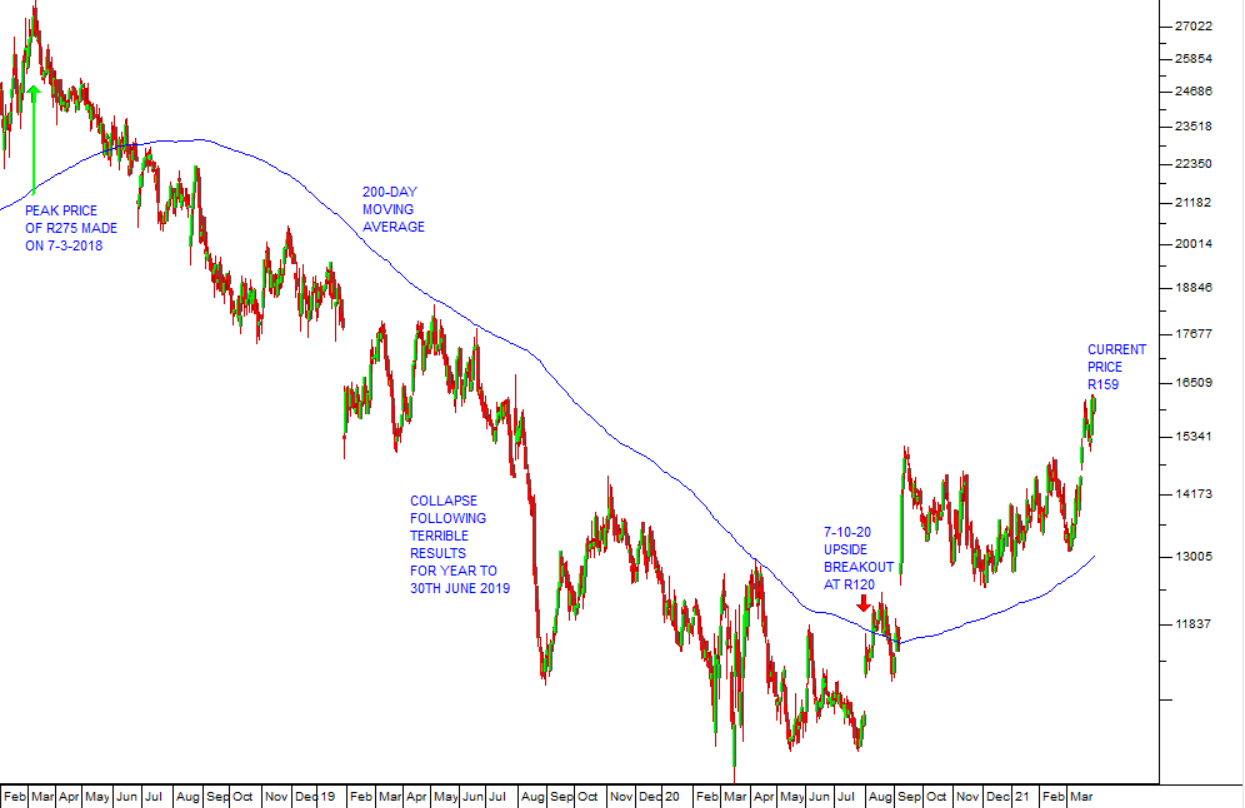

SHOPRITE

In the Confidential Report presented on 7th October 2020 we suggested that it was a good time to buy some Shoprite shares. This assertion was based on the clear upside breakout above the share’s 200-day simple moving average which happened on 8th September 2020. Since then the share has climbed strongly to its current price of R162 – a gain of 25,6% in five months. Consider the chart:

Shoprite’s operational update for the six months to 27th December 2020 which was published on 15th February 2021 showed sales growth of 5,6% and a 10,4% increase in headline earnings per share (HEPS). This enabled them to increase their dividend by over 22% - an excellent performance in a period dominated by the impact of the pandemic and related lock-downs. The key to being successful in the share market is to find and buy high-quality blue-chip shares when they are out of favour – as Shoprite was in October last year.

YORK

York timbers is one of the oldest companies listed on the JSE. It is a manufacturer of timber products owning plantations and timber mills. It is the largest producer of plywood and timber in South Africa. The company has suffered with the general demise of the construction industry over the last ten years and then has been impacted by the pandemic in 2020. Consider the chart:

You can see the impact of being linked to the construction industry and then the final fall in March last year with the lockdown. The share then formed an “island” between support at around 78c and resistance at about 110c. That island has been convincingly broken on the upside with a new upward trend being confirmed this year. We see this share as continuing to climb with the general recovery of the South African economy and the construction/home improvements industry.

BALWIN

With the general demise of the property sector on the JSE since the beginning of 2018, most property shares have taken a hammering. Some of them now appear cheap to us. Such a share is Balwin which specializes in developing secure sectional title properties in South Africa. The company made a strategic decision to get into the rental business at the beginning of 2019 and has since been keeping some of the properties that it develops and generating a rental income from them. This is a sound strategy which provides the company with a steady annuity-type income.

The share looks cheap to us with a net asset value of 631c against a share price of 461c. In addition, it has made a strong upside break through its long-term downward trendline. Consider the chart:

In its results for the six months to 31st August 2020 the company said, "The Group continued its focus on capital allocation and is pleased to report that cash on hand for the Group improved to R427.7 million. The Group's long-term debt to equity ratio at the end of the reporting period was 25%". This makes it one of the least geared property companies on the JSE.

GRAND PARADE

Grand Parade’s decision to get out of the fast-food business is paying dividends. The company sold its Dunkin Doughnuts and Baskin Robbins franchises in February 2019 and Burger King in 2020 as well as its 10% stake in Spur. These moves resulted in it being less exposed to COVID-19. The share has a net asset value (NAV) of 403c and is trading for 275c – which makes it a takeover target. The turnaround specialists, Venture Capital Partners recently increased their stake in the company to over 20% and may be interested in obtaining control.

The share price has broken convincingly up through its long-term downward trendline and looks set for an upward move. Consider the chart:

← Back to Articles