Exponential Growth

The S&P 500 index is important because all the stock markets around the world tend to follow it. If the S&P is in a bull trend then London, Tokyo and the JSE will also be in a bull trend – and vice versa.

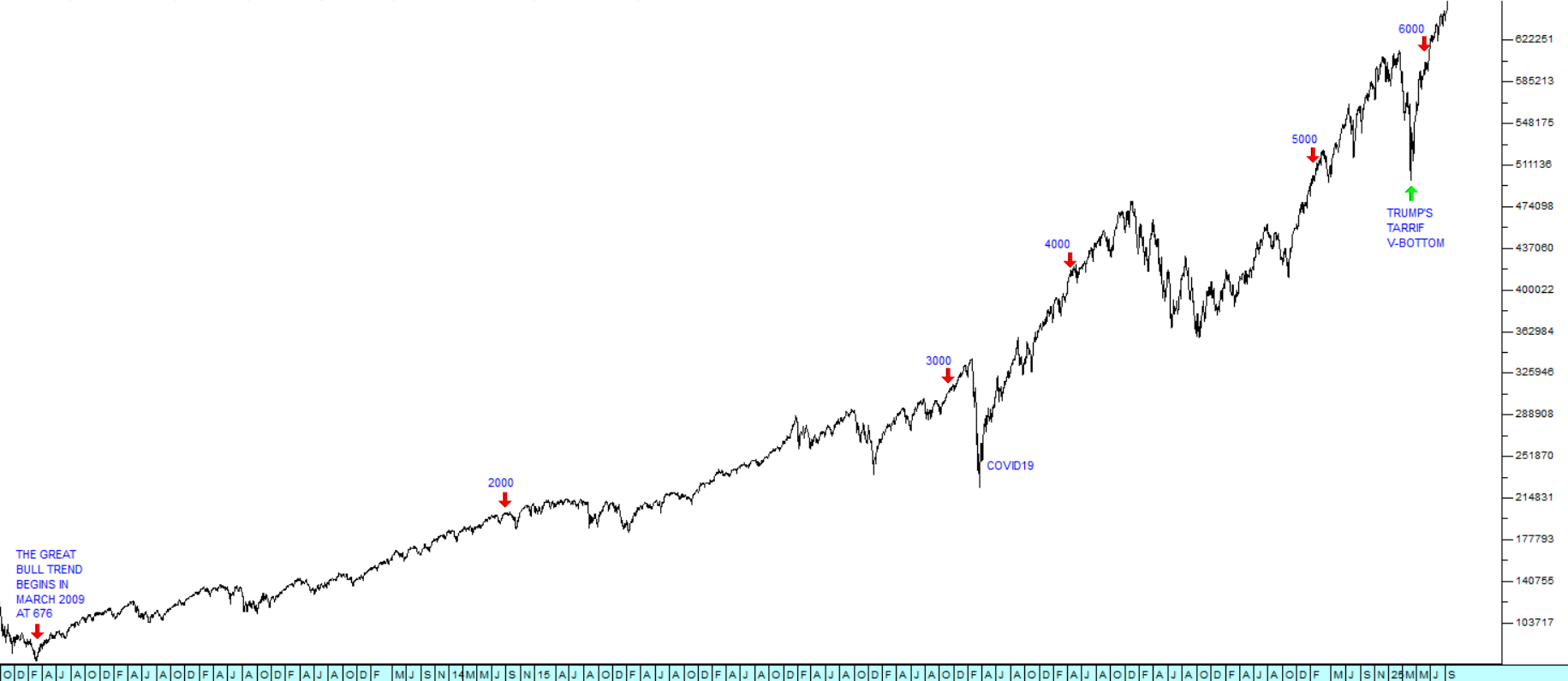

The S&P500 index began 68 years ago on 4 th March 1957 with an initial value of 43,73. It took nearly 41 years for it to reach 1000 (3rd of February 1998) and another 16 years to get to 2000 (29th of August 2014). The next thousand points to 4000 took just five years (12th of July 2019) and the next thousand took just 21 months (1st of April 2021). COVID-19 temporarily arrested the process and it took another 34 months to get to 5000 (19th of February 2024), but 6000 came 11 months later on the 27th of January this year. Since then, the index has risen a further 590 points. Consider the chart which shows the S&P500 since the start of the great bull trend 16 years ago:

My point is that the upward trend on the S&P500 is definitely becoming exponential. The index reflects investor perceptions of the real growth of the US economy plus the inflation rate.

The “black swan” event of COVID-19 and Trump’s tariff V-bottom slowed the progress down in the years after 2020, but the pattern is undeniable. The share markets of the world are caught up in an exponential rise due mainly to gathering excitement about the massive productivity benefits expected to flow from artificial intelligence (AI) and humanoid robotics.

Honestly, nobody can predict the medium- to long-term effects of the various new technologies on the economies of the world – especially when, in the background, there are major ideological conflicts taking place in the Middle East and Europe and the impact of climate change is only just beginning to be felt. There are simply too many unknowns.

Despite that, history and experience indicate that exponential trends like this one, especially in the share market, cannot persist indefinitely. At some point the expected gains will become heavily over-discounted and a correction will ensue. The question is, “When?”

In our view, the ultimate productivity benefits of the new technologies are still not clear. What is clear is that, far from slowing down, they will almost certainly gain momentum over the next ten to twenty years. For example, while there is much speculation and uncertainty about the impact of AI on jobs, there is virtually no uncertainty about its impact on the direction of profits among the S&P500 companies. All are expected to benefit to a greater or lesser extent.

From the lowest point of Trump’s tariff V-bottom at an index level of 4982 on the 8th April 2025, the S&P has risen 32% in just over 5 months indicating a strong degree of catch-up in equity valuations. With last week’s new all-time record high at 6587 on Thursday, shows that that rate of climb does not appear to be slowing down.

The bull market is being driven by strong expectations of the exceptional profits to be made by listed companies. In the 2025 average earnings per share (EPS) for S&P500 companies is expected to be at least 10% above the previous year and in 2026 this is expected to rise a further 14% above average for 2025 – and then a further 13% in 2027. These future gains, especially for 2027, are speculative but they are sufficiently strongly held to drive share prices up to new record levels.

The problem will come when company profits slow down and a gap begins to appear between the price of shares and the performance of the companies which they represent.

In our view that has not yet happened, and the investor excitement is warranted. Indeed, we are now expecting the S&P500 index to reach 10 000 in the relatively near future – probably within the next two years. So, our advice to private investors is to be fully invested, but to remain vigilant and maintain a strict stop-loss strategy.

← Back to Articles