The Confidential Report - November 2024

America

It is no exaggeration to say that the US elections currently taking place are the most critical in that country’s history from a political perspective. The outcome will determine the long-term future and policy direction of America and the world for years to come.

Speaking from experience, one major factor in determining voting trends is likely to be the progress of the S&P500 index in the three months immediately prior to the election. Historically, if the S&P rises in that 3-month period, the incumbent party (in this case the Democrats) wins about 80% of the time. This is because almost all Americans have a 401k investment plan – which is similar to our tax-free savings account (TFSA) where they save for their retirement. Most 401k’s are heavily invested in equities – so when the stock market is rising Americans feel much better off – and they inevitably give the incumbent party the credit for that.

In our view, the election result is unlikely to have an immediate or direct impact on the S&P500, aside, perhaps, from some increased volatility. In the short-term international investors are more interested in whether the US monetary policy committee (MPC) will reduce interest rates by 25 or 50 basis points at their next meeting, two days after the election. And that decision will not be a function of the election result. Rather it will be concerned with whether the MPC still believes that the US economy is slowing down sufficiently to keep inflation under control.

The volatility of the labour market has made assessing the state of the economy more difficult. Just 12000 jobs were created in October 2024 – far less than the 100 000 expected by analysts. The unemployment rate remained unchanged at 4,1% while job creation for September and August were revised down by a combined 112 000.

The recent hurricanes and a strike at Boeing impacted directly on the October numbers making it difficult to perceive a pattern. The Federal Reserve Bank’s monetary policy committee will make a decision on interest rates on 7th November – and the low job creation in October may well result in them reducing rates by a further 25 basis points – rather than leaving rates unchanged. This outcome is now seen as the most likely and has been perceived as positive by investors.

A critical factor in the S&P500 last week was the quarterly results from five of the seven big tech companies on Wall Street. And these were a mixed bag. The week began with Google’s parent company, Alphabet reporting cloud revenue of $11,35bn. This was a massive 35% improvement on the same quarter in 2023 – and well ahead of expectations. The news caused the company’s shares to rise 5% in a single day last week and other tech shares to rise in sympathy. Earnings per share rose to 212c – well above the 185c expected by analysts.

This was followed by a mixed bag from Microsoft, Meta and Apple which took the S&P down sharply. Then the week ended off with good results from Amazon which enabled the market to recover some of what it lost to end the month down 2,3% from its all-time record high made on Friday 18th October 2024. And these results came on top of Tesla’s 22% one-day gain on very strong guidance.

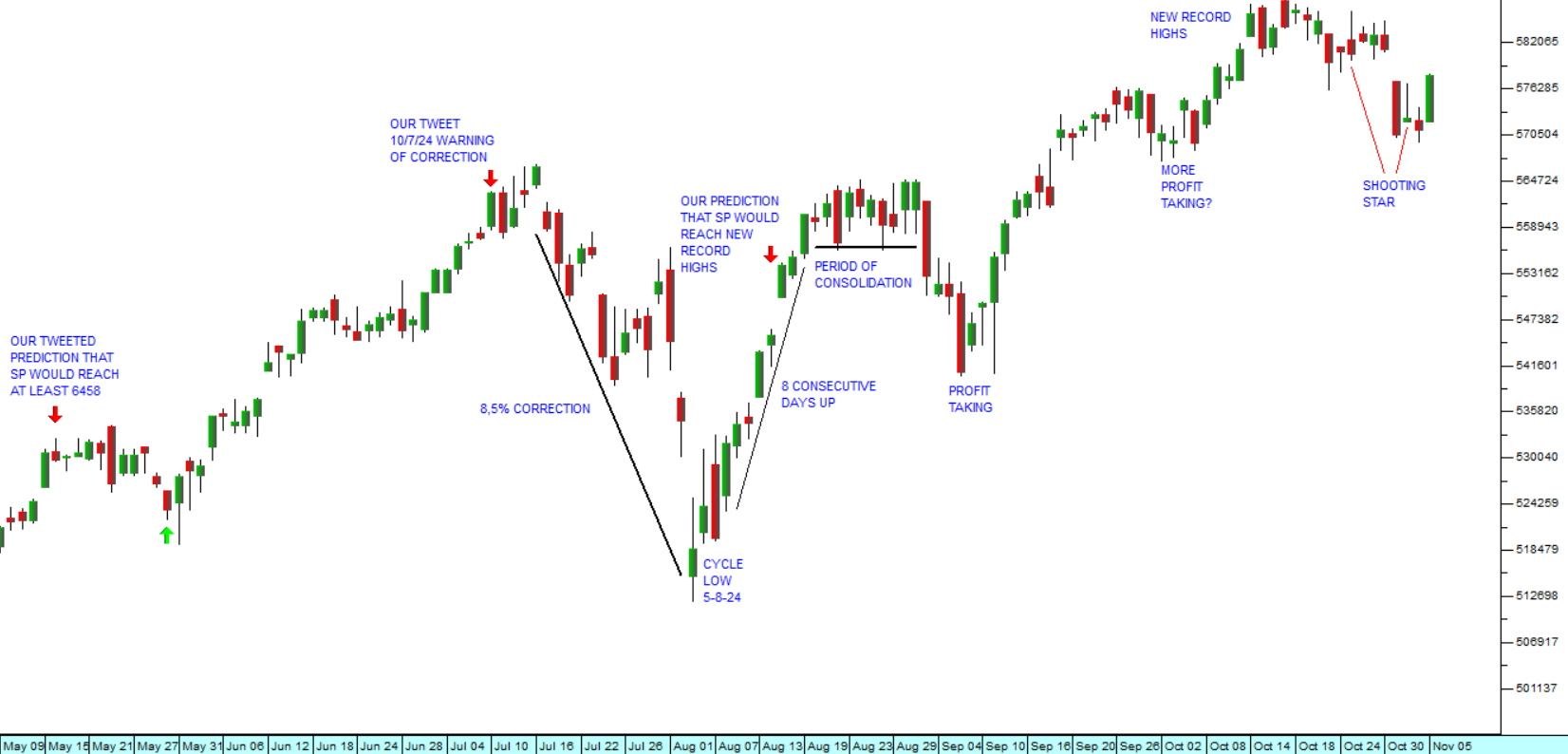

Another major factor is the yield inversion which has now reversed because the effective yield on the 10-year T-Bill rose to 4,38% on Friday 1st November 2024 – above the yield on the 2-year T-bill which was 4,21%. A couple of weeks ago, the inversion together with the rising unemployment rate were used to support the view that the MPC had waited too long before reducing interest rates. The fear was that the US economy was headed into recession. The jobs number in September and the shift in the yield on the 10-year T-bill have more-or-less put those fears to bed. The S&P has been hovering in the vicinity of its all-time record high during most of September and October. Consider the chart:

The chart shows the progress of the S&P500 index since the 9th of May 2024. This period has been characterized by growing uncertainty regarding the US elections, the start of a declining interest rate cycle and increasing enthusiasm for high tech shares. Notably, the month of October passed by without anyone worrying seriously about a crash. Despite this there has been some profit-taking by those investors who think it wise to stay out of the market until after the election. The S&P is currently in a mild correction. It is 2,3% below the all-time record high recorded on Friday 18th October at 5864.67. In our view, as soon as the election is over there will be a new surge of investor optimism which will take the index to further new record highs. Typically, there is a Christmas rally once October month has passed and we expect that to be the case this year.

The inflation rate in America fell further to 2,4% in September 2024 from August’s figure of 2,5%. This is the sixth consecutive month that the rate has fallen and provides the monetary policy committee (MPC) with the room to reduce rates by a further 25 basis points. A major factor was energy costs which fell 6,8% with the decline in the oil price – with petrol falling 15,3%. This is further good news for the Democrats as they face the November election. Generally, news which is good for the economy favours the incumbent party. Core inflation remains sticky at 3,3% but it should fall further in the coming months.

The Trump election campaign has been suffering a number of self-inflicted wounds, mainly as a direct result of Trump himself making damaging statements at his rallies. The insult to Puerto Ricans at Trump’s rally at Madison Square Gardens is very negative. There are 5,9 million Puerto Rican’s living in America and Puerto Rico itself is part of the US and so Puerto Ricans are almost all voting citizens of America. It seems insane that Trump would put someone on the podium who was going alienate such a large chunk of the voting public just before the election – but he did. The Trump campaign have sought to distance themselves from the insult, but the damage was done, and many prominent Puerto Ricans have now publicly proclaimed support for Harris.

His recent threats against Liz Cheney are considered by many to be illegal and an investigation has been launched into whether he can be charged with a crime in this regard. Such a crime is almost certainly sufficient to eliminate the bail which he currently enjoys on the two criminal indictments and one criminal conviction that he has.

Ukraine

The movement of about 11000 North Korean troops to Russia for deployment in the war against Ukraine has been marked as a significant escalation of the conflict by various world leaders. Our information is that these troops are probably not going to make a great difference on the battlefield. They are poorly trained and certainly not highly motivated. At best, they will become more cannon-fodder for Ukraine to destroy. However, the fact that Russia has seen the need to take this step shows the difficulties they are having in conscripting more Russians to the army. It also potentially opens the door for NATO countries to consider sending their troops to support Ukraine.

In the last two weeks Russia has lost more than 10 000 troops that have been killed, wounded, or captured. The reason for this is that they have been throwing men at the front lines in all the areas of conflict. They are attacking along almost the entire 1200km line in the hope, perhaps of influencing the US elections. Perhaps Putin hopes that he will make it possible for Trump to claim that he is the only one who can prevent World War III. Whatever the reason, they are attacking during the rainy season in Ukraine when it is very difficult to move heavy vehicles because of the mud. They cannot possibly hope to sustain this rate of losses for very long.

Gazprom, Russia’s leading producer of natural gas made a $7bn loss in 2023 compared with a $22bn profit made in 2022. The Russian government is a 50% shareholder in Gazprom and received $9,6bn in dividends and taxes from the company in 2022. Clearly, this is due mainly to European sanctions which have almost stopped Russian exports of gas to Europe. Beyond this, in the first 9 months of 2024 Gazprom made a further loss of $3,2bn.

The Russian central bank has also just hiked interest rates to 21%. This is the highest that rates have been since the invasion of Ukraine began in March 2022 and it is certainly causing both businesses and consumers considerable financial difficulty. The Russian central bank justified the rise in rates because inflation was running much higher than they had expected. The Russian economy is also suffering from the various conscriptions which have taken an estimated one million men out of the economy to fight in Ukraine. In our view, Putin and Russia are close to collapse and his only hope is that Trump will win the US election and take some of the pressure off him.

Middle East

For the moment, the war between Israel and Iran has taken centre stage in international news. Iran has again launched hundreds of missiles at Israel, most of which were shot down by either the Israeli iron dome or by the US. This is the second such attack this year, and, predictably, Netanyahu promised “painful” retaliation. Recent satellite footage of twelve border towns in Lebanon shows that Israeli bombing has completely destroyed them. Israel claims that they are being used as bases by Hezbollah – which Hezbollah denies. The danger is that this conflict together with the Ukraine war could enable Donald Trump to claim that he is the only one who can prevent World War III because of his relationships with Putin and Netanyahu.

There can be little doubt that some American voters see the conflict in the Middle East as the fault of the current Democrat administration and vice-president Kamala Harris. This could negatively impact support for the Harris in the election. Our view is that after the election, if Harris wins, these conflicts will probably subside, and both ultimately be resolved. If Trump wins, then Putin will get what he wants in a Ukraine peace accord - and Europe will become a far more dangerous place to live.

Commodities

One of the initial consequences of the war brewing in the Middle East is that the price of Brent oil jumped to $80 per barrel, but it has subsequently fallen back to $73. A sustained high price for oil could have a major impact on the world economy and the South African economy. Consider the chart:

The charts shows the established support level for North Sea Brent oil at $72 per barrel and the downward trend in prices over the past year. It is now clear that oil will remain close to the $72 support level at least until after the US elections – which benefits the Democratic Party as the incumbents.

Conflicts like those in the Middle East and Ukraine are also, of course, typically good for the price of gold. Over the past month, gold has continued to make new record highs and will probably continue upwards in the coming months. The rising price is surprising given that the yield on the US 10-year Treasury Bill has increased to above 4,3%. Gold offers investors no return at all – so a rising return in US T-Bills is usually negative for the precious metal.

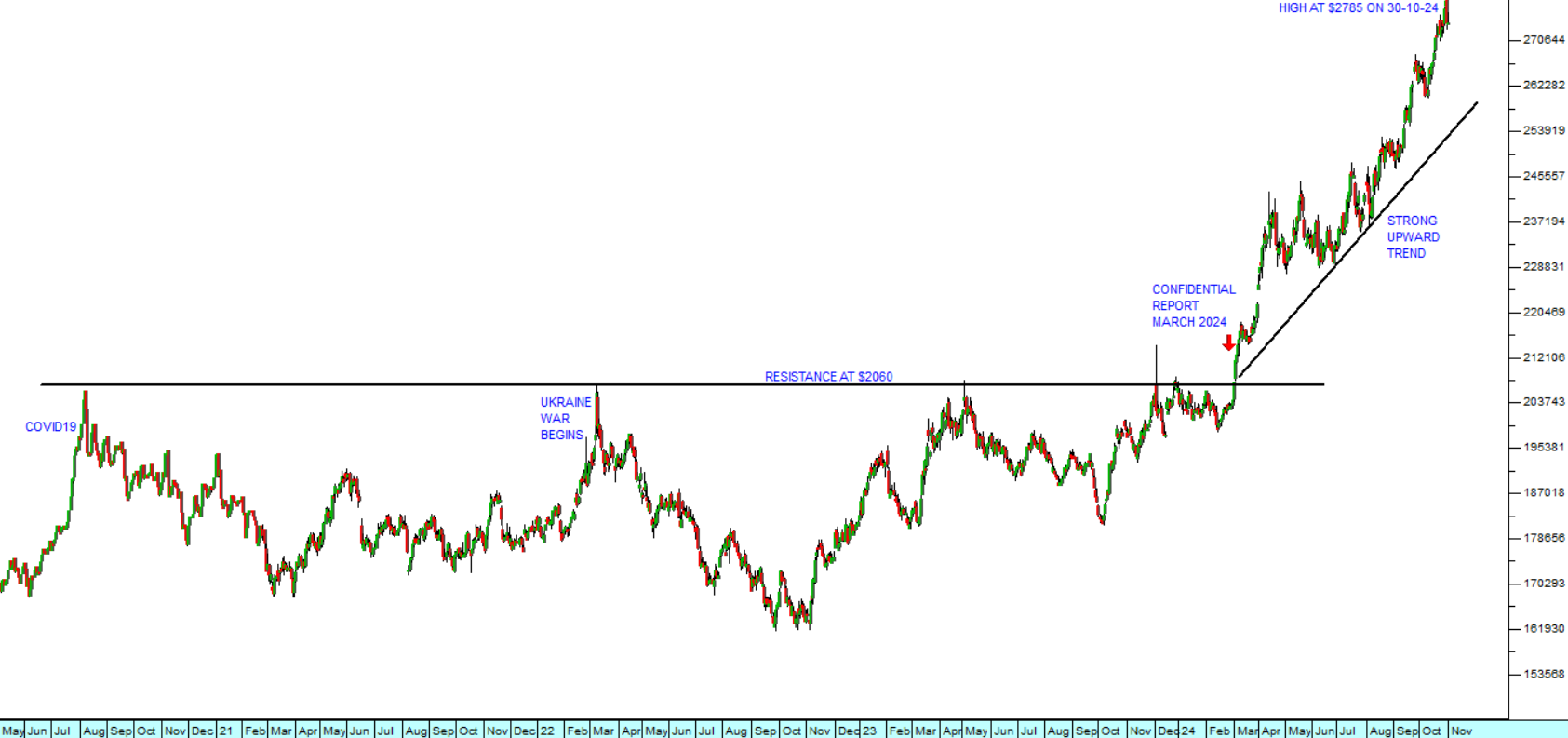

Gold rose to more than $2785 per ounce over the past week – which is over R49000. This is obviously good for those gold mines in South Africa which are still in operation, like Harmony. It also points to the international perception that there is higher uncertainty in world markets, especially considering the conflict in the Middle East and the imminent US Presidential elections. Consider the chart:

The chart shows the long-term resistance level in gold at $2060 – and the break above that level which we drew your attention to in our Confidential Report of March 2024, seven months ago. We added Harmony (HAR) to the Winning Shares List (WSL) long before that on 16th November 2023 – almost a year ago. In that time it has gone up by over 90%.

Political

The first poll after the appointment of the government of national unity (GNU), conducted by the Social Research Foundation, shows that 60% of South Africans believe that the GNU is doing a good job. It also shows that support for both the ANC and the DA has increased while support for the EFF has dropped sharply to 6% from the almost 10% that it had at the election. These results show that South Africans have firmly turned their backs on populism. The MK party’s support has remained more or less the same, but that support is probably mostly tribal, centred primarily on a sect of the Zulu nation in Natal. Needless to say, this outcome is extremely positive for the South African economy and the JSE.

The National Health Insurance (NHI) is probably the greatest stumbling block to the continued success of the government of national unity (GNU). With the South Africa Private Practitioners Forum (SAPPF) launching a legal action against it in the Pretoria High Court. This legal action now joins the legal actions taken by the trade union, Solidarity, and the Health Care Funders. A few other organisations are also considering legal action. The NHI was signed into law by the President just two weeks before the election in what many saw as a desperate attempt to shore up the ANC’s falling support with a populist measure. While there are many concerns about the NHI, the greatest concern is the necessary funding. Hopefully, the President will find a way to reach a compromise.

The mid-term budget policy statement (MTBPS) was significant mainly because the two major parties in the government of national unity (GNU) were both satisfied with it and agreed that debt consolidation “must take place.” Their ability to come to terms with each other and agree on a way forward is very encouraging for investors, companies, and consumers. It adds a layer of optimism to the economy that was always missing under the ANC’s rule. In our view, the stage is now set for steady improvement in the economy as more and more areas are reformed.

Economy

Government debt is now seen as peaking at 75,5% of gross domestic product (GDP) and then declining from 2026/7. The cost of interest on that debt will reach 22% of total revenue before it begins to fall. Debt service costs are now the largest single component in the budget, and they are increasing more quickly than GDP. The revenue shortfall is expected to be about R22bn this year. R11bn will be spent on early retirement packages to reduce the size of the civil service by 30 000 employees over the next 2 years. This move is painful in the short term but will pay off in the medium to long term. On the other hand, the South African Revenue Service (SARS) and the Justice Department are both to get badly needed additional funding. The Department of Mineral Resources and Energy will be split into two departments by April 2024.

The underfunding of the South African Revenue Service (SARS) in particular is short sighted. As things stand now SARS has a “tax gap” of over R1 trillion which it cannot collect because it does not have sufficient resources and staff. The tax gap amounts to 32% of the country’s total tax liability of R2,54trillion. This compares to Australia with a 7% tax gap and the UK with less than 5%. Clearly, if even half of this money could be collected it would make a huge dent in the government’s debt. It is difficult to understand the logic of not giving SARS sufficient funds to collect tax revenue. Hopefully, the advent of the government of national unity (GNU) will help to address this foolish and unnecessary anomaly.

About 25% of the government’s debt in the form of government bonds is held by foreign investors. This has dropped from over 40% because of the downgrading of South Africa to below investment grade by the three international ratings agencies (Fitch, Moody’s and Standard & Poors). With the sharp improvement in business conditions in the last few months, there has been a reversal of this trend, and foreign funds are beginning to flow back into the country. With expectations that the annual growth will be above 1% for 2024 and accelerate to 2% or more next year, it should be possible for government debt levels to be reduced resulting in more positive ratings from the ratings agencies. Hopefully, the new government of national unity (GNU) will be able to reverse much of the self-inflicted damage created by previous administrations.

Notably, the MTBPS allocated no further funds for state-owned enterprises (SOE) as bailouts. This includes Transnet, which desperately needs about R150bn. Transnet is currently paying R1bn a month in interest on its existing debt and it needs funding to rebuild the rail network to facilitate the recovery in the economy. In our view it is highly likely that the Treasury will have to provide additional funds to Transnet fairly soon and the omission of this from the MTBPS damages its credibility.

The consumer price index fell further to 3,8% in September 2024, down from August’s 4,4%. The major cause of the lower inflation was the falling price of petrol. Transport costs fell 1,1% in the month. Fuel was 9% cheaper in August 2024 than in August 2023 while food inflation was unchanged. The lower inflation figure makes a 50-basis point cut in interest rates in November possible, but we believe that the monetary policy committee (MPC) will, once again, be cut by just twenty-five basis points to keep South African bonds competitive internationally. We expect inflation to continue falling in October possibly to as little as 3%. The lower inflation figure also makes Eskom’s suggested 36% price increase even more absurd.

The latest projections by the Reserve Bank show that inflation will remain close to 4,5% but fall to as little as 3%, if the rand continues to strengthen over the next two years. This could enable the Bank to reduce interest rates by as much as 2% from current levels. The Bank’s intention has always been to reduce inflation expectations to the point where they are more in line with our major trading partners. This would mean reducing the target range to between 3% and 4,5% over time. The Bank now expects growth to be 1,1% in 2024, rising to 1,8% next year. This compares with the IMF’s prediction that growth this year will be 1,1% and 1,5% next year. We believe that these forecasts will prove to be conservative. We are expecting growth to be at least 2% next year and perhaps much higher depending on the on-going impact of the government of national unity (GNU). President Ramaphosa said that the GNU must remain stable in order for it to achieve its ambitious goal of 3% growth in 2025. Key to that is Operation Vulindlela which expects to create 130 000 jobs per annum. The two-pot retirement system is expected to result in R40bn being released into the economy this year following its implementation on the 1st of September 2024 and then R20bn per annum thereafter.

Adrian Gore, CEO of Discovery, says that it is possible for the South African economy to grow by as much as 3% in 2025 and to create 2,5 million jobs over the next 5 years. The new government of national unity (GNU) is working closely with business to overcome the major bottlenecks in the economy. President Ramaphosa is fully committed to this process and addressed a meeting of 150 leading business executives at Sandton on 1st October 2024. He said South Africa was entering a new era of “hope and promise”. Gore says that the growth will come from improved sentiment and from four megawatts of additional power added to the grid.

A JP Morgan analyst in London said that South Africa needs two years of 2% growth or better to attract serious overseas investors. This is clearly within our reach, starting in 2025. We have said previously that we expect 2025’s growth to be 2% rather than the Reserve Bank’s more conservative 1,8%. Since the GNU came into power and loadshedding ended the international investor attitude towards South African investments has improved dramatically. Money has been flowing into South African bonds and equities. The yield on our long government bonds has dropped by an impressive 150 basis points and could fall further. The rand has strengthened significantly, and Goldman Sachs is now talking about the rand having a fair value of R12 – R14 to the US dollar. Obviously, all of this is particularly good for our shares. Combined with the record-breaking trend on Wall Street, the positive attitude of overseas investors should keep pushing the JSE to new record highs.

Transnet moved 149m tons in 2022/23, 152m tons in 2023/4 and is aiming for 170m tons in 2024/5. In phase 2 of the government/private sector partnership launched on the 1st of October 2024, a goal of 193m tons was set. This will obviously require the private sector to inject some funds to fast-track improvements to the infrastructure. The improvement in Transnet’s performance is critical for the economy, both for imports and exports. Certain industries have been hard hit by their inability to get products to port. Kumba had to adjust its production guidance down recently because of Transnet’s inefficiency. If the bottlenecks are cleared away, there will be a significant improvement in the economy.

Private sector credit extension (PSCE) increased by 4,6% in September 2024, slightly less than August’s 4,9%, but ahead of economists’ forecast of 4%. Business credit extension was up 5,6% showing a resurgence of confidence since the end of loadshedding and the advent of the government of national unity (GNU). The growth in credit reflects an economy that is returning to growth as confidence levels improve. The GNU’s plans to achieve 3% growth in 2025 are probably a bit optimistic. We expect growth to be between 2% and 3%.

Retail sales rose by 3,2% in the year to the end of August 2024, following July’s growth of 1,7% and June’s 4%. This is a sharp improvement on last year and shows the impact of the end of loadshedding, the drop in the petrol price over the last 3 months and the prospect of reduced interest rates going forward. The largest growth came from household furniture and appliances at 10,5%. Consumers do not buy big ticket items like furniture and appliances unless they are feeling more secure financially. The availability of credit has improved with the downward trend in interest rates, and this has made large purchases more affordable. We expect consumer spending to continue to accelerate into next year.

The ABSA purchasing managers index (PMI) came in at 52,8 in September 2024 – substantially up from August’s figure of 43,6. Both local and export demand are rising which is good for the manufacturing sector. Obviously, the end of loadshedding has been a major factor for manufacturers despite the high cost of electricity which recently increased by 12,4%.

New vehicle sales fell by 4,1% in September 2024. Car sales were up 2% while pick-up and minibus sales fell by 17,1%. In the year to the end of September, sales were down 5,8%. Vehicle exports were down 38% in September compared with a year ago. Due to demand from the rental sector and an outstanding contribution from the passenger car segment, new vehicle sales reported their best performance of the year in October, increasing by 5.5%. 47924 vehicles were sold, beating the previous best month, July, by 3695 units. This was also ahead of October 2023 by 2506 units. The prospects of the vehicle industry are improving with lower interest rates, the end of loadshedding, lower fuel prices, declining inflation, and the appointment of the new government of national unity (GNU). As the economy picks up vehicle sales should improve steadily. Although the October sales have made the year-to-date market look more hopeful, sales are down for the 10 months by 4,7% compared to the same period in 2023. At 425,806 sales for the year so far, the market should comfortably exceed 500,000 units but will probably not outperform 2023.

Estimates of the world’s motor car market in 2025 show that the production of vehicles is expected to rise by 2,3% to just over ninety-seven million. Of these, about 20% will be electric vehicles (EV) and EV production is set to increase by about 16%. This shows how quickly EVs are taking over from conventional internal combustion engine vehicles. Obviously, this trend has long-term implications for the oil industry as the demand for petrol and diesel should begin to fall in tandem. It also has implications for the South African motor industry which needs to move quickly towards the production of EVs to avoid being left behind.

The informal sector in South Africa is essentially a euphemism for tax evasion. Hundreds of thousands of small businesses, many of them one man/woman operations, operate completely with cash, submit no returns to the Receiver of Revenue and pay no tax. But that situation is changing. More and more South Africans now have a bank account and are operating digitally. If their business activities are substantial enough this will bring them within the Receiver’s purview sooner or later. As technology improves and the benefits of moving money digitally become more apparent, the informal sector should begin to shrink. Notably, the amount of money in coins and notes actually decreased by 08% in 2023. Usually, the cash portion of the economy increases more or less in line with the growth in gross domestic product (GDP). The Governor of the Reserve Bank, Lesetja Kganyago is urging all South Africans to move away from cash.

The agreement signed between Northam Platinum and an independent power producer (IPP) to supply 220 gigawatt hours of power per annum from a solar power facility to be built at Zondereinde in Limpopo shows how the mining industry is moving away from Eskom, despite the end of loadshedding simply because solar power is both cheaper and potentially more reliable. The extraordinary and completely unjustifiable cost of Eskom electricity is driving both businesses and consumers to build alternative solutions. The fact that the cost of coal has dropped from $450 a ton in 2022 to the current price of around $113 while the cost of Eskom electricity has been going up steadily is criminal and completely unjustifiable. Eighty percent of Eskom’s power is produced from coal. One benefit of the shift away from Eskom is that South Africa’s carbon footprint is improving rapidly. The Zondereinde facility hopes to drop its carbon footprint by 60% by 2030.

It is notable that the board of Attacq (ATT) have deemed it necessary to begin planning for water outages of up to 5 days at their Waterfall complex, the Mall of Africa, and other developments. They say that water availability in certain areas and especially around Gauteng is becoming a problem. Redefine (RDF), another listed property company, is also preparing for water outages and intends to spend R200m on water tanks and water backup. Watershedding is already being applied in parts of Johannesburg and is expected to become worse. The delays in bringing the second phase of the Lesotho Highlands water project online will have major consequences for businesses and consumers in the Gauteng area.

Eskom has now avoided loadshedding since 26th March 2024 and has reduced unplanned outages to 7,3 gigawatts – down from its peak level of eighteen gigawatts. The challenge now is to provide the newly separate transmission company with sufficient funding to build sufficient transmission lines. A plan is being formulated to allow the private sector to participate in this building which is similar to the independent power producers (IPP) program for renewable energy. Obviously, South Africa needs to find a way to break Eskom’s monopoly and reduce the cost of electricity. Notably, the National Energy Regulator (NERSA) registered two gigawatts of new renewable energy projects in the third quarter of 2024. This shows that the move towards alternative energy sources continues despite the end of loadshedding – mainly because of the high cost of Eskom’s electricity. The total registered renewable energy is now at 8,7 gigawatts with 6,43 gigawatts already installed.

The DA’s Siviwe Gwarube, now the Minister of Basic Education, has drawn attention to the fact that there is a R32bn shortfall in provincial education budgets. Over the last 5 years the number of new students attending government schools has increased by 300 000, but the number of teachers has remained the same. This is resulting in much larger class sizes and poorer standards of education. The government has been forced to cut back all departmental budgets to make space for the above-inflation civil service wage increases that were agreed to in April 2022. In the long term, education is the key to the growth and prosperity of the South African economy – so cutting back in this area is short-sighted.

Mergers and acquisitions in the mining industry increased dramatically in 2023 to $10bn – up from 2022’s figure of $2,5bn. Apparently the increase is an international phenomenon which is a function of the search for metals like copper and gold which have been in high demand. The so-called “strategic minerals” which are used in the world’s transition to fossil-free energy are the most in demand. Platinum group metals (PGM) and coal have seen their prices drop by over 35% in the past year and are out of favour. The lower prices of these metals have also resulted in acquisitions and consolidation.

The copper price has risen above $10 000 per ton because of the 50-basis point cut in interest rates in America on 18th September 2024 and the recent stimulation of the Chinese economy. China relaxed rules for homebuyers and moved to lower mortgage rates to support the troubled property market. This could have a strong impact on construction and construction materials like copper. The People’s Bank of China also slashed banks’ reserve requirement ratio by 50 basis points last week, which is expected to free up 1 trillion yuan in capital. They also lowered medium- and short-term interest rates which will encourage borrowing. Chinese demand accounts for about half of the world demand for base metals.

The Rand

The rand has continued with the strengthening trend that it established after it broke out of its triangle formation in April and May 2024. The strength comes from the improved prospects for the South African economy following the appointment of the government of national unity (GNU) and the general shift in international sentiment towards “risk-on” as the US economy continues to perform well, and US interest rates continue to fall. Our expectation is that the rand will continue to strengthen in the medium term. This will have the effect of reducing the cost of fuel and keeping inflation low. It will benefit importers and prejudice exporters. In general, however, the strength of the rand is a major factor in improving business and consumer confidence. Consider the chart:

The chart shows the accelerating strengthening trend from April 2024. Obviously, the rand is volatile because it is favoured by international investors due to the liquidity of our currency market. This means that any move towards “risk-off” in international investor sentiment is immediately reflected in a fall in the rand – even if the shift has little or nothing to do with South Africa.

Companies

NEW LISTING – BOXER

Boxer is currently a highly successful subsidiary of Pick ‘n Pay designed to appeal to lower income groups. It is planning to be separately listed later in 2024 with the abbreviation “BOX”. In the first 6 months of the 2025 year (to end August) Boxer grew turnover 12% to almost R20bn with a trading profit of R809m. Boxer currently has 489 stores and plans to open a further 53 stores this year. Pick ‘n Pay is expecting to raise between R6bn and R8bn through the listing. In our view, Boxer will become a blue-chip share with good long-term potential.

WEBUYCARS (WBC)

When this company was spun out of Transaction Capital (TCP) and separately listed on 11th April 2024, we were pretty certain it would turn into a winner.

Companies which come to the market for the first time often have some shareholders who received the shares for a preferential price before the listing (such as important customers, suppliers and staff members etc.). Some of those people inevitably have no interest in keeping the shares as an investment and so sell them as soon as they can on the open market. They are known as “stags” and they often cause the share price to fall in the first few weeks after the listing. In the case of WBC, the stagging lasted until 29th April 2024 and then the share began to appreciate.

We added it to the Winning Shares List (WSL) a few days later on 3rd May 2024 at a price of 2085c. It closed on Friday last week at 3672c – a gain of 76% in just over 6 months – or 151% per annum. We really hope that you took advantage of this very low risk opportunity to buy into this solid blue-chip share.

In a trading statement for the year to the 30th of September 2024 the company estimated that core headline earnings per share (HEPS) would increase by between 21% and 26%. The once-off cost of the listing was R45m. Consider the chart:

In our view, this share will continue to perform strongly in the future.

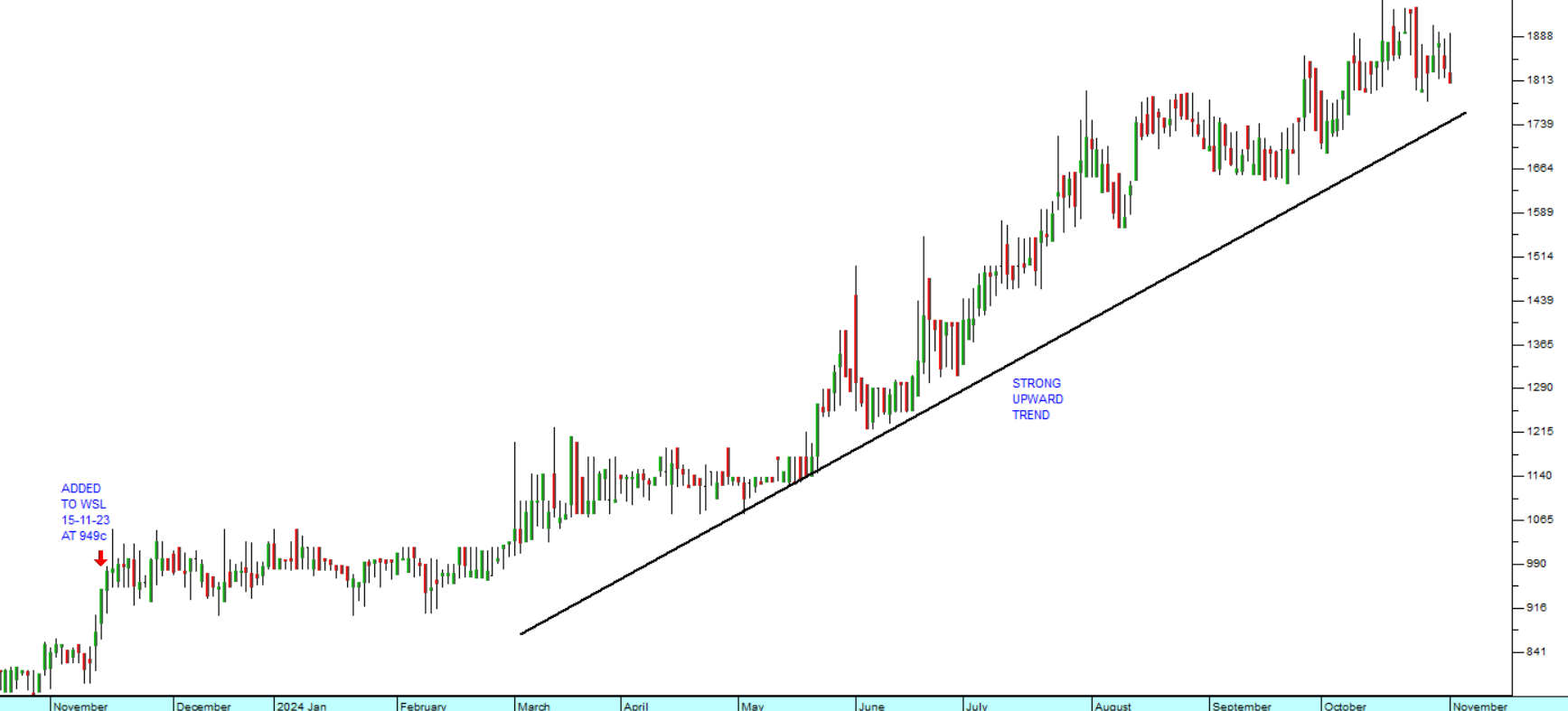

ALTRON (AEL)

Altron describes its business as “...using technology to transform today into a simpler, safer and smarter tomorrow.” They are a leading platform and IT services business in their chosen markets. The company operates in fintech, health tech and vehicle tracking. In a trading statement for the six months to the 31st of August 2024 the company estimated that headline earnings per share from continuing operations would increase by between 171% and 189%. Investors, anticipating these excellent results, have driven the share price up for the past year. The company has the added advantage of being a good rand hedge.

We added the share to the Winning Shares List on 15th November 2023 when it began its new upward trend. The share was then trading for 949c. It has subsequently risen to 1812c. That is a gain of almost 91% in just under a year. Consider the chart:

Again, we believe that the upward trend will be sustained.

WBHO (WBO)

This is one of South Africa’s more successful construction companies that has managed to survive the decimation of the construction industry by selling off assets, cutting costs and paying off debt. Its astute management decisions and conservatism began to pay off about two years ago and we finally added it to the Winning Shares List (WSL) on 18th September 2023 when the share was trading for 12087c. It closed last Friday at 21408c, but it has been as high as 23419c just over a month ago.

In its results for the year to 30th June 2024, the company reported revenue up 15,8% and headline earnings per share (HEPS) from continuing operations up 20,4%. The company said, “The strong growth in South Africa reflects the high levels of work currently on hand within the Roads and earthworks division which achieved 46% growth in the region.” Consider the chart:

You will note the selloff in WBHO’s shares over the past month or so. We regard that as a potential buying opportunity.

LEWIS (LEW)

Lewis is a retailer of furniture and appliances with 840 stores most of which are inside South Africa. In addition to making a profit on what they sell, they offer finance to prospective clients and then charge interest on the outstanding balance. They are very efficient at controlling and managing their large debtors’ book. Their business is naturally sensitive to the level of consumer spending and the level of interest rates. They have a policy of keeping debt levels to a minimum which gives them the balance sheet strength to ride out difficult economic times and to make highly advantageous acquisitions from time to time (like the Beares group). In their financial statements for the year to 31st March 2024 the company reported revenue up 9,8% and headline earnings per share (HEPS) up 7,1%. The most impressive aspect of their financials was their balance sheet which had a debt/equity ratio of just 11,7%.

In a trading statement for the six months to 30th September 2024 the company estimated that HEPS would increase by between 45% and 55%. This is an extraordinary result for a business which is on the coal face of consumer spending in South Africa.

We added Lewis to the Winning Shares List (WSL) originally on 1st December 2023 at 4150c. The share closed on Friday at over 7207c – a gain of 73,66% in just under a year.

This is a company that will definitely benefit directly from the falling interest rate environment which now exists, and the economic growth expected to result from the appointment of the government of national unity (GNU). Consider the chart:

There has been some volatility in the share price in recent weeks, but we believe that on a P:E of 7.8 and a dividend yield (DY) of 5,55% the share remains a bargain.

← Back to Articles