The Confidential Report - March 2024

America

On Friday last week, Nvidia shares rose 4% on Wall Street to a new record high. The rise meant that Nvidia closed at a market capitalisation of above $2 trillion for the first time and that it has doubled its value in just nine months. The market is being driven higher by the general understanding that the next move in interest rates will be down and that this move is most likely to begin in June 2024. The economy is booming already, even when interest rates are at their peak and there is no talk of recession. Evidently, the Federal Reserve Bank has achieved its objective of bringing inflation down in the economy with a soft landing.

A key factor motivating investors has been the drop in bond yields with the US 10-year Treasury Bill (T-Bill) falling to an effective yield of 4,19%. On 19th October 2023 the yield was at 4,98%, the highest it has been in 5 years. The 2-year T-bill yield has also been falling but the yield remains in in inverted territory, but the inversion has narrowed from its peak of -1,08% to -0,35% on Friday last week. Our view is that yield on the 10-year will move higher than the yield on the 2-year fairly soon. If that happens then the yield will no longer be inverted, and the prospects of an economic recession will recede.

The primary factor driving both the economy and the stock market is the growing awareness that artificial intelligence (AI) is going to be a major factor in boosting productivity across all S&P500 companies and across all economies in the world. This new technology is gaining ground especially in America, but it will affect all economies in due course. Combined with the growing importance of robotics, especially humanoid robotics, AI is creating a new era of unprecedented prosperity.

On Friday last week the S&P500 hit yet another new record high at 5137. It has now been rising strongly for four months without a significant correction. This shows the extraordinary bullishness of investors in the market. Every time the S&P has shown the slightest sign of falling, the bulls have been there enthusiastically “buying the dips”. The fear of further interest rate hikes has completely evaporated and now the only point of discussion is when the Fed will begin to cut interest rates. The consensus is that rates will begin to fall from the June 2024 monetary policy committee (MPC) meeting. If that happens then investors will become even more bullish. Consider the chart:

Clearly, no upward trend like this can continue indefinitely and some sort of major correction is now overdue. That does not necessarily mean that the upward trend on the S&P is going to come to an end immediately, but it does mean that the probability of a correction is rising steadily as the market rises. If there is a correction it could take the S&P back to its January 2022 high of 4796 before resuming on its upward path. Such a correction would be both healthy and normal.

In January 2024 the US economy created 335 000 new jobs – more than double what economists were predicting. The unemployment rate remained very low at 3,7%. This means that everyone who wants a job in America is able to find one. Most of the new jobs were created in health care, professional services and retail. This shows that the economy is growing rapidly and there are no signs of a recession anywhere in sight.

Productivity increased by 3,2% in the last quarter of 2023, probably mainly as a result of improved technologies such as AI. Rising productivity levels will impact directly on the profits of S&P500 companies and hence on their share prices and price:earnings ratios (P.E.)

Average hourly earnings rose 0,6% between December 2023 and January 2024 showing that Americans are earning more. Over the last 12 months hourly earnings have increased by 4,5%.

Personal consumption expenditure (PCE) inflation over the last six months was under 2% in January 2024 and the inflation rate (CPI) in December 2023 was below 3%. This means that there is very little incentive for the Federal Reserve Bank to raise interest rates and rates are expected to remain where they are until June 2024 and then begin to fall.

In our view, the US economy is gaining momentum, not losing it. It is well to remember that it is an enormous $27 trillion economy. Its continued growth will have the effect of dragging up the other major economies of the world – most importantly Europe and Japan. The problems being experienced by the Chinese economy will also be mitigated by the growth in America. In time, even the South African economy will benefit as commodity prices improve and the market for our exports improves.

Ukraine

The death of Alexei Navalny in a Russian prison has been universally blamed on Putin. The refusal of the authorities to release the body immediately is a clear indication of the fact that his death was the result of some sort of dirty work. There have been widespread protests and international reaction. At least 400 people have been arrested at 32 organised protests against Navalny’s murder across various cities in Russia. At Navalny’s funeral thousands of Russians turned out and chanted anti-Putin slogans – risking arrest and persecution. This is a clear indication of the danger which Putin faces. Navalny was seen as Putin’s most serious rival in the elections coming up in March 2024. Navalny was serving a 30-year sentence in the Russian Arctic penal colony. In a blatant effort to contain the civil unrest and prevent it from spreading, the protests and arrests were not mentioned in Russian state media outlets which are government controlled. Apparently, Navalny was about to be part of a prisoner exchange when the murder took place. Clearly Putin did not want him free in the Western World immediately before the March 2024 elections. Of course, Putin’s decision to have Navalny murdered comes shortly after the murder of Yevgeny Prigozhin and is an indication that Putin is feeling very insecure. One possible effect of Navalny’s death might be to help with the passing of the US government’s $95bn aid package through the House of Representatives, $61bn of which is ear-marked for Ukraine.

Ukraine’s strategic withdrawal from the ruined city of Avdiivka after 4 months of constant Russian attacks is an indication of the extreme pressure their military is under due to the failure of America to supply them with sufficient arms and ammunition. Various estimates suggest that Russia is now firing at least 5 times as many artillery shells as Ukraine mainly because of ammunition shortages. The retaking of Avdiivka is being lauded by Putin as a major victory and a turning point in the war, but it is something of a Pyrrhic victory given the enormous Russian losses incurred in its taking. The Republicans in the US House of Representatives who are resisting the passing of a $61bn aid package to Ukraine are clearly assisting Russia to gain ground in the Ukraine war. They seek to link the aid package to the resolution of the border issue in America which Trump has said that he wants to use as an election issue in the run-up to the November 2024 presidential elections. The Speaker of the House, Mike Johnson, is refusing to bring the aid package before the house, even though he is aware that it has overwhelming bipartisan support.

The suggestion by the President of France, Emmanuel Macron, that France could deploy troops to Ukraine to assist with the war effort against Russia certainly raises the possibility of a further escalation. So far, NATO countries have firmly resisted any attempt to engage their forces directly in the war and have restricted themselves to supplying weapons, ammunition and other support. However, there has been a pattern of steadily approving more and more effective weaponry. First main battle tanks, then long range missiles and most recently, F16 fighter jets. Perhaps putting troops into Ukraine is the next logical step in this process. In each case, NATO countries at first resisted the idea, but then after a time ended up providing what Ukraine needed to keep Russia at bay. Perhaps the process will be the same with putting troops on the ground in Ukraine. If one NATO country puts troops into Ukraine, others are likely to follow – especially those in the region which have a common border with Russia and so are most at threat should Ukraine be overrun. Certainly, it seems that at the moment Putin is taking advantage of the hesitation by the US to continue supplying particularly ammunition to Ukraine. Our view is that sooner or later, if the war continues for much longer, NATO will eventually be forced to supply troops – and, of course, those troops will be equipped with the very latest military hardware. Already the Estonian Prime Minister, Kaja Kallas, has said that her country is ready to send to troops to Ukraine, not to fight, but to provide support and training. The Netherlands, Lithuania and even Canada have said that they are also willing to send troops to Ukraine for training and support. To us this looks like NATO troops on the ground in Ukraine is an almost inevitable escalation, which is now in its initial stages. Putin’s predictable reaction to threaten the use of nuclear weapons was as predictable as it was unlikely. Any use of nuclear weapons in the war would result in the immediate and complete destruction of Russia.

Politics

The date for this year’s elections has been set as the 29th of May. It will probably be the most important election in the 30 years since the ANC took control of the country as the ANC could lose its parliamentary majority. The combination of continuous loadshedding for the past 16 years, lack of service delivery and general economic mismanagement have led to high levels of unemployment and poverty. There is even a possibility that the DA’s coalition could scrape together enough votes to displace the ANC completely. Alternatively, the ANC may be forced to make a compromise with one or more of the smaller parties to remain in power. Whatever the outcome is, the impact on the South African will ultimately be substantial and the final result may have significant implications for private investors on the JSE.

Standard Bank’s predictions indicate that the ANC will lose its parliamentary majority in this year’s elections. Their forecast indicates that the ANC will be returned with 47,5% of the vote while the DA will get 23% and the EFF 11%. If they are right, these numbers would not have a major impact on the running of the country and the economy because the ANC will form an alliance with one of the smaller parties and continue to hold the reins of power. However, these estimates are sharply different from the latest Ipsos polls which are showing that the ANC will only get 38,5% of the vote – but that same poll shows that the EFF would come second with 18,6% and the DA would fall back to as little as 17,3%. The DA’s own internal polling suggests that their support will grow past 32% and that together with their alliance partners they could actually unseat the ANC completely. Polls are hardly conclusive because they are always based on a so-called “representative sample” and their predictions can vary substantially from one week to the next - but they are an indication. It seems that all of them are presaging a continuing decline in ANC support and gains for the other parties. A major factor will be the number of voters who choose to vote on the day. That could be as low as 40% or as high as 70% depending on a variety of issues on the day such as the weather and the affordability of transport. The electoral commission says that there are about 27,4m voters registered in South Africa with 6,4m in Gauteng, 5,7m in Natal and 3,4m in the Eastern Cape.

The decision by the Constitutional Court not to allow the ANC to appeal a judgement which forces it to disclose the process which it used to appoint government officials is crucial for South Africa to become a meritocracy. The ANC has a record of appointing people to high positions based purely on their loyalty to the party rather than their skills and experience. Judge Raymond Zondo said, at the end of the state capture enquiry, that the practice of “cadre deployment” was both “illegal and unconstitutional”. The policy is widely viewed as being at the heart of state capture. The ANC has had had to release records of the processes they went through to appoint key officials to the DA going back to 2013. The fallout from this could be substantial.

Finance Minister, Enoch Godongwana, was very upbeat in the delivery of the budget speech on 21st February 2024 – which is surprising in the face of the overwhelming economic difficulties which South Africa currently faces and the need to take R150bn out of the gold and foreign exchange contingency reserve account (GFECRA) in order to balance the books and compensate for a R56bn reduction in tax collections as well as a 7% increase in the civil servant wage bill. All in all, the budget can be seen as an election budget aimed at minimising the ANC’s poor performance over the past decade, especially in the area of service delivery and the management of state-owned enterprises (SOE).

The ANC’s election manifesto says that they plan to reintroduce prescribed assets if re-elected. Prescribed assets means that the various financial institutions will be forced to invest a portion of their funds into government bonds to finance economic development and infrastructure. The National Party developed this policy, forcing pension funds to invest as much as 77% of their cash into government bonds and state-owned enterprises. The policy was scrapped in 1989. In South Africa today, financial institutions invest into those assets which offer the best return based on their risk profile. They already invest a portion of their funds into government bonds and certain other government projects, but on the basis that they offer a good return in relation to their risk. Making such investment compulsory would relieve the government of the need to ensure that the projects being invested in offered a market-related return. Clearly this is another pre-election populist move. Perhaps the ANC sees the additional funding being used for such dubious projects as the National Health Insurance (NHI) project.

The death rate of women during child birth is twice as high in the Eastern Cape as it is in the Western Cape. The Western Cape, under DA management, is running at 62 deaths per 100 000 while the Eastern Cape is averaging 125 deaths. The comparison is a stark indicator of the difference between DA run hospitals and those run by the ANC. One district in Limpopo province is recording almost 200 deaths per 100 000 births. Figures like this, taken across government services generally will have an impact on the outcome of the elections at the end of May this year.

Budget

In the budget the Minister of Finance announced that the government is to use R150bn of the profits on the gold and foreign exchange contingency reserve account (GFECRA) to bolster its balance sheet and reduce its interest bill by R30bn. With the help of this R150bn transfer, the government was able to project budget deficits of 4,9% in 2023, 4,5% in 2024 and 3,7% in 2025. The ratings agency Fitch says these projections are unrealistic because they do not consider further Transnet subsidies which will be required in the coming years. These profits on the GFECRA arise from the depreciation of the rand against hard currencies since 2006. The funds will be created by borrowing from the commercial banks and will require the government to pay interest at the repo rate – so no actual reserves will have to be realised, and a lower rate of interest will have to paid on the amount.

The out-going CEO of Firstrand, Alan Pullinger, has said that South Africa is basically running out of money which explains the R150bn transfer from reserves to the Treasury. This transfer involves considerable “moral hazard” because it opens the door for future use of the country’s reserves to meet budget shortfalls. It will likely become the ANC’s go-to strategy to cope with enormous government over-spending. The transfer weakens the economy and will negatively impact the rand going forward. In our view, the R150bn transfer is a clear acknowledgment that the ANC cannot discipline itself to operate within its budgets – a fact which is amply demonstrated by the fact that the party itself is virtually bankrupt.

The additional funding from GFECRA will enable the government to meet the R56bn expected drop in tax revenues and meet the higher cost of the civil service as a result of its 7% pay increase earlier this year. The decrease in tax revenues is mainly a result of lower tax collections from the mining sector as commodity prices have fallen, impacting on their profits. The government will also use the injection to avoid tax increases and continue with its debt consolidation program.

The budget has been criticised as an “election con” by analysts who say that the transfer of R150bn from reserves will make it more difficult to control imported inflation in the future. The government has taken an asset belonging to the Reserve Bank and used it to shore up its balance sheet. It has in effect taken on a new loan to pay excessive expenses and pay down another loan, but that does not change its state of high indebtedness. Taking the R150bn from the Reserve Bank’s assets has enabled the government to declare the first “budget surplus” since 2008/9 when Trevor Manuel finally managed to overcome the huge budget deficit which he inherited from the National Party. That sounds good on paper, but it is a falsehood which obscures the fact that this government has presided over the systematic decimation of the South African economy for the past 15 years.

Economy

The National Treasury announced on 5th February 2024 that the budget deficit had increased to 6% of gross domestic product (GDP) in December 2023 – up from 5,7% and the highest level it has been at for 24 months. Our Minister of Finance, Enoch Godongwana, is having a very hard time keeping ANC spending in check in the run-up to the elections while at the same time trying to present a picture of “fiscal consolidation” to investors and the ratings agencies. The main cause of the deterioration is lower tax revenues – combined with the increased civil service wage bill and the interest costs on the government’s debt. All the bailouts for state-owned enterprises (SOE) are coming home to roost – and without the R150bn from the Reserve Bank, radical cuts would have been essential.

South Africa’s gross gold and foreign exchange reserves stood at $61,18bn in January – which is about R1,155 trillion rand at current exchange rates. A large chunk of this, about $8,2bn is held in gold bullion and goes up and down with the US dollar price of gold. There had been suggestions, in recent months, that the government use some of these reserves to reduce the size of its deficit, but such a move undermines the relative stability of the rand. The level of reserves is used to provide import cover and is measured by the number of months which the reserves can cover. At the end of January 2024 the reserves were sufficient to cover 5,5 months of imports – which is well below the world average of 9 months and the BRICS average of over 10 months.

The S&P purchasing managers index (PMI) for January 2024 came in at 49,2 – slightly above December 2023 which was 49 and still below the neutral level of 50, indicating contraction. The crisis at Durban port is impeding both imports and exports while loadshedding continues to take a toll. New orders were down sharply as consumer confidence waned. The ABSA PMI fell sharply in January 2024 to 43,6 from 50,9 implying a rapid contraction of manufacturing activity.

Stats SA reports that manufacturing output grew by a meagre 0,7% during the 2023 with production down 1,7% in December month from November. The production decline in December was extensive, with significant declines in the production of motor vehicles and cement production. Manufacturing now contributes only about 11% to gross domestic product (GDP) – down from about 22% before the ANC took over. Obviously, the decline in manufacturing is due to the steady destruction of the South African economy by the ANC since it took power – endemic corruption, persistent loadshedding and now massive logistic problems at Transnet.

The mining industry is critical to the South African economy, creating hundreds of thousands of jobs and contributing massively to government funds. For example, in 2021 the industry produced more than R1 trillion worth of product, contributed R481bn to gross domestic product (GDP), employed 459 000 people and contributed R78bn in taxes. The total contribution to the fiscus, including PAYE, was over R135bn – R9bn up on the previous year. However, mining production has been declining and contributed only 6,2% of GDP in 2023 – down from 2022’s 7,3%. The number of people employed has increased to 477 000. There are three major factors constraining mining production – legislative uncertainty, loadshedding and logistics.

Retail sales rose by 2,7% in December 2023 when compared with December 2022. This is far better than the average of economists’ predictions of a 0,7% growth. This was despite the fact that average take-home pay was down 4,7% in 2023. The best performing sectors in December 2023 were clothing and footwear up 7% and general dealers up 3,5%. Hardware was down 2,8% and pharmaceuticals fell 1,9%. Over the whole year of 2023, shopping activity fell by 1%. Obviously, the reason for lower spending 2023 was the rise in interest rates.

Sanral reports that the huge increase in the use of heavy trucks to transport goods since the decline of Transnet’s rail system is causing major damage to various key highways – especially the N2 from Ermelo to Richards Bay. Apparently that highway was designed to handle about 200 trucks a day but is now handling more than ten times that number.

Stanlib reports that overseas investors have taken more than R1 trillion out of the South African bond and share markets over the past decade. This was partly caused by the ratings agencies’ downgrades which have taken the country to well below the investment grade which it used to have. The level of corruption, the parlous condition of the major state-owned enterprises (SOE) and the level of government debt have also been major factors. Obviously, if that investment capital had remained in the country, our economic position would have been enormously better than it is.

The number of taxpayers in South Africa declined since 2018– which means that less than 10% of the population paid 40% of the country’s total tax revenue. This lopsided tax burden and the steady decline in the number of tax-paying South Africans, combined with the sharp drop-off in mining taxes due to falling commodity prices means that the Treasury will find it almost impossible to fund the National Health Insurance bill (NHI) which has been approved by parliament and just requires President Ramaphosa’s signature to come into law. Despite this, given the ANC’s falling support levels, the president may still make the NHI law in order to use it as a populist measure to garner additional support. It will then almost certainly be challenged for its constitutional validity in court preventing it from being implemented for years.

The unemployment rate ticked up in the 4th quarter of 2023 to 32,1% from the 3rd quarter’s 31,9%. 128 000 jobs were lost in the formal sector while the informal sector added 124 000 new jobs. In general, the economy was struggling with higher levels of loadshedding, higher interest rates and the difficulties of Transnet in getting exports to port. The platinum sector has begun to announce large-scale retrenchments as commodity prices fall. None of this does the ruling party any good in the run-up to the general elections this year.

In January month, South African imports rose by 2,5% while exports fell by 12,9% leading to a deficit of R9,4bn on the trade account. This is stark evidence of the sharp decline in commodity prices and the impact which that is having on the economy and the rand. A major part of the problem is the difficulty which exporters now have in getting their goods to port and onto a ship. The drop in exports was also due to a decline in vehicle exports where export sales dropped by 2,1% compared to January 2022. The weakness of the global trading environment is also a factor.

Eskom

The 600-page report by the German consortium “vgbe” indicates that Eskom is far from overcoming load-shedding and that vital maintenance needs to be done to avoid what they call a “catastrophic failure” of the grid. Among the work that needs to be done urgently is the maintenance of the raw water treatment plant that provides water to both the Medupi and Matimba power stations. If that facility were to cease operating then 12 units with a total capacity of 10 gigawatts would stop producing power – and that is just one of the major threats which the system faces. Continuous crisis management and a lack of planned maintenance have led to a situation where the grid is very fragile. This means that South Africans who are investing in alternative power solutions are not wasting their money. It remains essential for both businesses and consumers to get away from their reliance on Eskom as far as possible.

The Rand

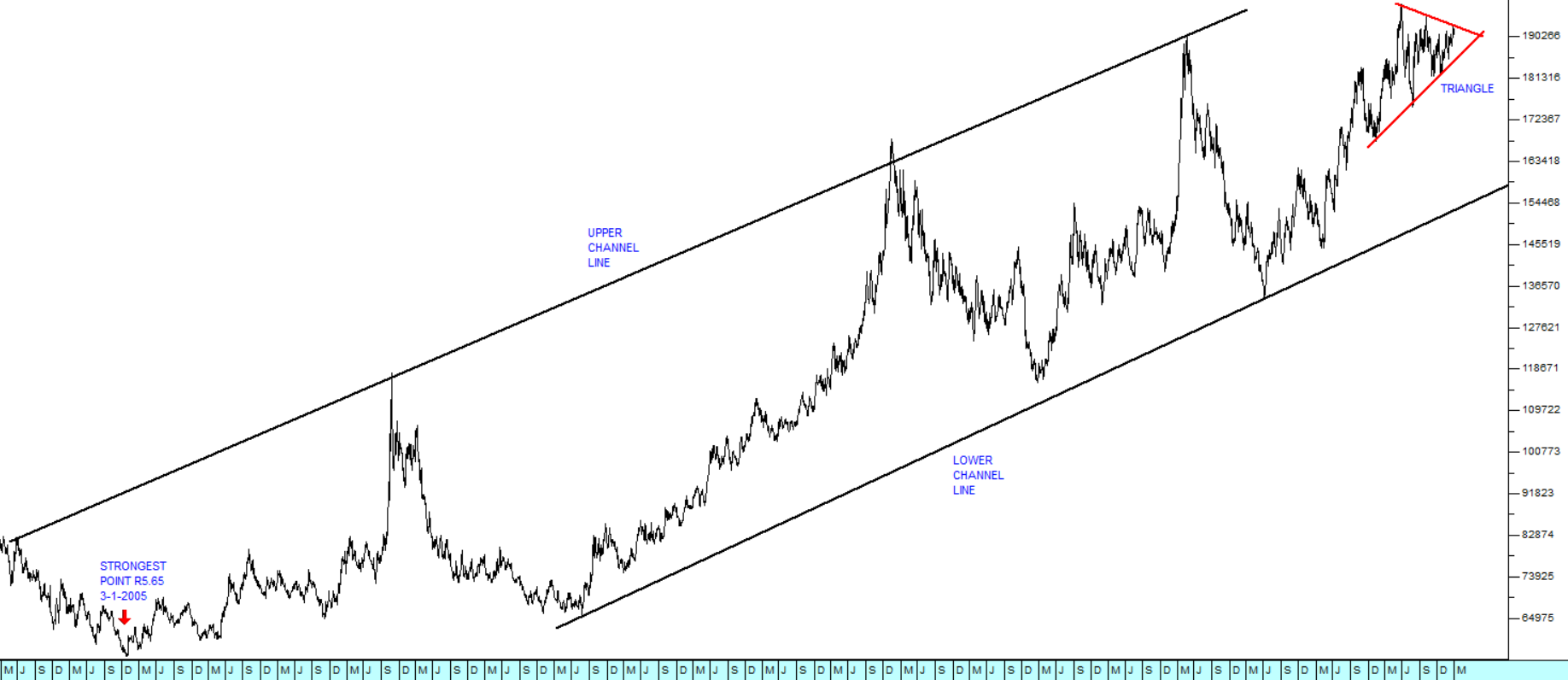

The rand has been in a long-term weakening trend since the beginning of 2005. The weakness is defined by the clearly defined channel in the chart below with parallel upper and lower channel lines.

On 3rd January 2005 it reached its strongest level at R5.65 to the US dollar and it has been falling steadily ever since.

Since the middle of 2023 the rand has been fluctuating within a triangle. The triangle is defined by upper and lower trendlines which are converging. A triangle occurs when the market goes through a period of declining uncertainty. The fluctuations become smaller and smaller until eventually either the upper or lower trendline is broken – indicating the direction of the trend going forward. In our view, the rand will break decisively down against the US dollar sometime later this year and in the process break through the psychological barrier at R20 to the US dollar.

The further weakening of the rand will benefit rand-hedge shares while prejudicing those shares which are dependent on imports. It will also cause inflation to increase as the price of petrol in rands increases.

The long-term weakness of the rand is a direct reflection of the general mismanagement of the South African since 2005. The currency of a country is like the shares of a listed company. If a company is expected to do well and make profits, its shares will go up and vice versa. If a country is expected to do well and be profitable then its currency strengthens against the currencies of other countries in exactly the same way.

General

According to the Treasury, only about 6% of South Africans have sufficient savings to cover their retirement and less than 10% will be able to maintain their standard of living after they stop working. Most will have to continue working or will have to cut back sharply. Most will end up living off the government’s old age pension of just over R2000 a month. In our view, most South Africans generally do not live within their income and so do not save. Many live to the full extent of their credit and are in constant financial distress as they desperately borrow from one source to pay what they owe to another. They also end up paying a considerable amount of their income in interest on their debts and many of their debts are unsecured so the interest rates are excessive and unaffordable. They have little or no reserves to fall back on if they have an unexpected expense or suddenly lose their job.

The agreement reached between government, Transnet and ArcelorMittal SA (ACL) to keep the long-steel production facilities in New Castle and Vereeniging open is welcome. ACL warned in December 2023 that due to the inefficiencies at Transnet it would be forced to close the manufacturing facilities which would result in the loss of 3500 jobs directly and others at sub-contractors The closure would have had a major impact on the local communities. ACL is dependent on the efficient transport of iron ore and coking coal by rail to produce long-steel products like rebar, wire rods, merchant bars and railway tracks. It supplies the construction and mining industries and the motor manufacturing industry takes about 70 000 tons of its production each year. Many other local production industries are dependent on supplies from ACL. Since 2022 the company has been forced to use road transport which is far more expensive than rail and it has estimated that the additional cost was about R1,1bn in the year.

The floods in Natal in 2022 are considered to be a direct result of climate change. They are estimated to have cost about R38bn and caused 460 deaths. There was extensive damage to infrastructure. President Ramaphosa, in his “State of the Nation” speech to both houses of Parliament said that a fund will be established to counter the effects of climate change such as droughts, fire and flooding. Notably, January 2024 was the hottest month on record and that 2023 was the hottest year since records began in 1850. Climate change is rapidly becoming a reality which is impacting government and private sector costs. We expect it to gradually become a more and more important factor in share assessment over the next decade.

The fact that no one has yet been convicted for state capture in South Africa reflects badly on the Ramaphosa administration. He says that there are more than 200 people being prosecuted, but the South African public wants to see some high-level convictions. R14bn worth of assets have been frozen by the Asset Forfeiture Unit and about R8,6bn of ill-gotten gains has been returned to government. The South African Revenue Service (SARS) has also collected about R4,8bn as a result of the work done by the Special Investigating Unit (SIU) and a further R64bn is the subject of civil litigation. Our view is that most voters believe that the response to state capture has been far from adequate – and many will make their feelings known in the coming election.

Bitcoin has been surging since the beginning of 2024. It broke up through the 200-day moving average in mid-March 2023 and has been climbing ever since. Consider the chart:

Since cryptocurrencies do not represent any kind of asset or income stream, they cannot be analysed fundamentally. This means that the only way to assess their possible future performance is technically. In our view, Bitcoin is now at very high levels which makes it highly risky. Our advice is, if you have it, sell it and, if you don’t have it, don’t buy it. If you are determined to hold it, then watch for technical signs of a slow-down in the current upward trend and certainly do not ignore your stops.

Commodities

Gold is probably the most effective and historically proven hedge against the weakness of paper currencies. If inflation is seen to be rising or about to rise, gold will go up. It responds positively to any type of political risk, and especially war or the possibility of war.

The chart shows the US dollar price of gold over the past five years, and as you can see, it appears to be in the process of breaking above previous long-term resistance at around $2060. We can see two possible causes of this rise:

- The potential for an escalation in the Ukraine war as some NATO countries begin talking about putting troops on the ground in Ukraine.

- The potential for rising world inflation as the American economy heads into boom phase, stimulated by rapid increases in productivity due to artificial intelligence and accumulated impact of decades of quantitative easing.

The rand price of gold is likely to be even more bullish as the rand depreciates against first world currencies.

Companies

For some time now we have been advocating investment in various property shares and real estate investment trusts (REIT's). Examples include Balwin, Calgro, Dipula and Fortress. Indeed, the entire property sector has turned around and is now in an upward trend:

The chart shows that since October last year, the property index has been rising steadily and is now close to breaking above its previous cycle high at 349 made on 6th January 2022. We expect property shares, many of which trade as much as 50% below their net asset values (NAV) to continue to perform well. Certainly, there can be no doubt that the big institutions are filling their pockets with these shares at the moment.

ADVTECH

ADvTECH is a company which specialises in providing education to South Africans. It is filling the gap as the quality of government-provided education has deteriorated. It has a schools division (Crawford, Abbots and Trinity House) and a tertiary division (Varsity College, Rosebank College and Vega amongst others). The great advantage of the education industry is that traditionally students pay for their education in advance. This means that ADvTECH has a very low or even negative working capital and excellent cash flows. In its results for the six months to 30th June 2023 the company reported revenue up 16% and headline earnings per share (HEPS) up 24%. These are excellent results given the difficulties in the economy at the moment. The company has been in a strong upward trend since August last year. We added it to the Winning Shares List on 14th August 2023 at 1975c. It closed on Friday last week at 2757c – a gain of almost 40% in just over 6 months. Consider the chart:

We believe that ADvTECH will continue to perform well in the future.

TRANSCAP

As a private investor it is very important to study the key developments in the market and consider carefully how they impact on the prices of the specific shares involved. The progress of the Transcap (TCP) share price over the past three years offers some useful lessons in how the Johannesburg Stock Exchange (JSE) works and how you can profit from it. Consider the chart of Transcap and think about what you can learn from it:

Lessons:

- The importance of institutions: The JSE is dominated by the large institutions such as pension funds, insurance companies and unit trusts. Collectively, the institutions account for about 90% of all trades done on the market – which means that private investors are only responsible for about 10%. Institutional funds are managed by fund managers who are very highly paid and highly qualified employees of the big institutions. They tend to operate collectively – “when one sheep crosses the bridge, they all cross the bridge”.

- Volatility at the top: When a quality share has been rising in a strong upward trend for a long time it must be an institutional favourite. Towards the top of that trend it will become increasingly volatile. You can see on the above chart how the upward trend becomes noticeably more volatile as it reaches its peak.

- Size matters: The biggest problem that institutions have is the massive size of the funds which they manage. This means that they cannot buy in or sell out quickly. On the chart above, you will notice the long period of downward movement which I have labelled “institutional off-loading”. During this phase the fund managers become increasingly uncomfortable as the share price falls. They do not know what is wrong, but consider it safest to reduce their holdings.

- The trigger: This is normally either a public announcement by the company or sometimes an article in the financial media which reveals the full extent of the disaster. In the case of TCP it was their trading statement of 13th March 2023 in which they revealed that they had made a significant loss in the six months to 31st March 2023.

- The collapse: This is usually very dramatic because the fund managers suddenly realise that they are sitting with huge quantities of the share which are now worth a fraction of what they paid for them. They scramble to sell as much as they can, as quickly as they can.

- Bull traps: The downward trend is brough to a temporary halt by the first “bull trap”. This is caused by those shareholders who cannot get their heads around the massive value destruction that has taken place. They believe the share has fallen too far and they seek to take advantage by buying in at bargain prices. There can be several bull traps.

- Capitulation: This is the point at which even the most optimistic investors simply give up hope. In a word, they “capitulate” and sell out for whatever they can get. It marks the lowest point in the downward trend and is the signal for the “smart money” to begin accumulating the share. Of course, it is very difficult to know exactly when this point has been reached.

- The 65-day E: One of the best ways to avoid getting caught in a bull trap is to apply a 65-day exponentially smoothed moving average and wait patiently for an upside break. By the time the share price breaks up through its 65-day E the bad news has usually been fully discounted and the smart money is steadily buying up the share.

- Buying signal: As a private investor you should wait until the share price breaks clearly up through its 65-day E. In the case of TCP this occurred on 6th November 2023 at a price of 577c. Since then, the share has risen to 973 – a gain of 67% in less than 4 months.

When a high quality share like Transcap collapses your first consideration should be to decide whether you think the company is on track to be liquidated eventually (as may still happen to Steinhoff) – or whether it will recover after a period of reorganisation and restructuring. As we indicated in our article on TCP on 15th May 2023, we never thought that Transcap would go into liquidation for a variety of reasons. When that is the case then obviously, the share price must at some point turn and begin going up again – the only important question is, “When?”.

The other important consideration is your stop-loss strategy. If you held Transcap when the downward trend began in May and June 2022, when exactly would you have sold it? Obviously, holding the share through the downward move doesn’t make any sense – so you must have an effective stop-loss that gets you out of any share at some point. Your stop should not be more than 20% from the highest point that the share has reached since you bought it. In the case of Transcap that would have got you out at 4177c at the latest and so you would have preserved the bulk of your capital and whatever gains you had made until that point.

← Back to Articles