The Confidential Report - July 2024

America

After a 5,5% correction, the S&P500 has entered a strong new upward trend. We anticipated this in our tweet of the 3rd of June 2024 where we said, “We now expect the index to rise off that base to further new record highs.” It has broken above the resistance at the previous cycle high of 5254, and then returned to test that level, as a support. At that point there were three consecutive hammer formations that indicated that there was potential for the index to go much higher. The support at 5254 held and the index has duly gone on to make a series of new all-time record highs. Consider the chart:

Technically, we should now begin to prepare ourselves for the possibility of another correction, although there appears to be an excessive amount of bullishness evident in the daily market action. Do not forget – nothing in the markets moves in a straight line!

As the market goes higher, the bears are being eliminated. In a great bull market there will always be some “market experts” who from time to time will decide to call the top of the market. Then as the market goes higher, and the people who listened to them and sold out lose money, they lose all credibility. We call this process “The Elimination of the Bears” and it is a characteristic of the final stages of all great bull trends. Eventually, a point is reached where no one is willing to stake their reputation on calling the top of the market – and that, of course, is the point at which you should begin to quietly move back into cash…

But there are still plenty of bears around. For example, some of the “experts” that are or were bearish include:

- Barry Bannister of Stifel who says the S&P will fall 13% by year-end.

- Peter Berezin of BCA Research who says that all the leading economic indicators point to a recession.

- Tony Dye, better known as “Dr Doom” who has been predicting a crash for years even as the market kept rising.

- Russell Clark, hedge fund manager, who had to shut his fund down as a result of losses he made because the market kept on rising.

- JP Morgan strategist, Marko Kolanovic, who is expecting the S&P to fall 23% by year-end.

And there are others.

The point is that as the bull market keeps on posting new record highs, they all end up looking foolish – but their existence means that the bull trend is still in progress. It is when they disappear that you need to become worried.

In May of 2024, headline personal consumption expenditure (PCE) was flat on the month and up just 2,6% over the year. Core PCE, which is the Federal Reserve Bank’s (The Fed) preferred measure of inflation and excludes food and fuel, was 0,1% for the month and 2,6% over the year. This was in line with economists’ expectations and shows that the inflation rate is on track to reach the Fed’s goal of 2%. As a result, the market is now pricing in a 64,1% probability that the Fed will begin cutting rates in September and that perception is pushing the S&P500 index to new record highs. In the first six months to 2024, the index has climbed 14,5%. This was led by the NASDAQ which has increased by 18,1%, driven by the buying frenzy surrounding artificial intelligence (AI). In the first half of the year, Nvidia shares have gone up by 156%.

Interest rate cuts in Canada, Sweden, Switzerland and now the European Union (EU) are early signs that world interest rates are turning down after an extensive period of high rates. Investors are fully aware of this important fact. America is only expecting interest rates to begin falling in September – but the direction of the trend seems to be clear. There is no more talk of raising rates, and inflation metrics world-wide have been improving. Over time, lower interest rates must benefit equity markets around the world, including the JSE. In anticipation of lower rates and their impact on corporate profits, markets are breaking to new record highs. In South Africa, rates will come down in lockstep with America because we have to keep the return on our government bonds relatively attractive to keep bringing in foreign direct investment (FDI).

American non-farm payrolls increased by 272 000 in May of 2024 – more than 50% above economists’ expectations and well above April’s figure of 165 000. At the same time the unemployment rate rose to 4% from April’s figure of 3,9%. The labour market still looks strong, despite the high level of interest rates.

The consumer price index (CPI) rose by 0,3% in April month and 3,4% in the year to April 2024. This was slightly down on March’s figure of 3,5%. The figures are in line with economists’ expectations. Inflation at these lower levels is proving to be very “sticky”. For rates to be lowered in September, the monetary policy committee (MPC) will need to see some tangible evidence that the economy is cooling sufficiently for core PCE to be on track to reach its target of 2%. The CPI has been stuck between 3% and 4% for a year now.

The US monetary policy committee (MPC) is, as usual, on the horns of a dilemma. If they lower rates too soon then the inflation rate could begin to rise again – and, if they delay lowering rates for too long, they risk taking the economy into a recession. One point appears certain – the economy is booming and that is likely to continue at least for the rest of this year, which is good news for Joe Biden’s election campaign.

The poor showing by Joe Biden in his debate with Donald Trump has significantly damaged his prospects of winning in November. It was an unmitigated disaster for Democrats. In our view, the best hope now for a Biden win is that Trump damages himself further in the months between now and the election – which, of course, is entirely possible. It is, for example, possible that, against the advice of his inner circle, Trump decides to do a second debate with Biden closer to the election – and that Biden manages to give a significantly better performance. Trump’s ego could easily make him overly confident of winning again to consolidate his position.

In our view, the raised prospect of a Trump win in November, following that debate, will have a minimal impact on markets – at least in the short term. Wall Street has acquired so much upward momentum that it seems unlikely that anything Trump might do, even if re-elected, would derail it at least before the middle of next year. It is nonetheless very disturbing that Biden was so ineffective - and the longer-term consequences are not good.

Oil

One potential problem for American and world markets is the price of oil. Since the beginning of June 2024, the oil price has been rising because of increased tensions between Israel and Hezbollah, backed by Iran. The two sides have been exchanging an increasing number of attacks in recent weeks which has made oil investors concerned that they are moving towards an all-out war. The fear is that Israel will invade Iran to push Hezbollah back – and that might trigger a wider confrontation which would impact oil supplies.

The price of North Sea Brent oil has been reflecting these concerns. Consider the chart:

The recent upward trend in June month is obviously not good for world inflation and does not help Joe Biden’s campaign to retain the White House. It helps Russia in its war against Ukraine by making additional foreign exchange available to fund the continued prosecution of the war.

Ukraine

With the resumption of support from NATO and particularly America, the war is gradually moving back in favour of Ukraine. The flow of ammunition has been resumed and the Ukrainians have been given permission to use the long-range American ATACMS rockets to attack targets inside Russia. The effect has been to degrade the Russian military and oil infrastructure making it more difficult for them to mount an attack.

In fact, the Russian summer push towards Kharkiv, has all but failed with the Ukrainians regaining control of key areas around Chasiv-Yar and damaging Russia’s air defenses, especially in Crimea. With Ukraine’s newly acquired ability to hit targets deep inside Russia it is becoming much more difficult for the Russian to build up forces for a decisive attack on Kharkiv. The Russian Black Sea fleet has also been taking hits which are forcing it to relocate further away from Ukraine.

Ukrainian drone technology continues to be a major factor impacting oil infrastructure deep inside Russia. The Ukrainians are beginning to use their drones to destroy Russian drones destined for Ukrainian targets. This marks a new technological milestone in drone warfare, with drones fighting drones.

Crimea is becoming untenable for the Russians, especially as a logistic hub off which to mount and support attacks into Ukraine. On 10th June, a number of S300 and S400 air defence systems in Crimea were destroyed by ATACMS missiles. Then, the recent destruction of an S500 Promethius air defence system has made air defence of Crimea there more-or-less impossible. The Kirch bridge is looking increasingly vulnerable to Ukrainian attacks and could be completely destroyed.

Retaining control of Crimea is vital to Putin’s continued support within Russia and if it is lost, he will certainly have difficulty in trying to sustain the idea that he is winning his “special military operation” in Ukraine. We believe that if Ukraine can re-take Crimea Putin’s political future inside Russia will be in jeopardy.

The failure of the S300 and S400 systems in Crimea and elsewhere has demonstrated that Russian air defences are ineffective which has enormous implications for NATO and the balance of power in Europe. The Ukrainian ability to strike assets deep inside Russia means that Russia is very vulnerable to NATO weapons.

Political

In our September 2023 Confidential Report, nine months ago, we said the following:

“In our view, the ANC will probably get about 40% of the vote next year and will thus be forced to compromise with one of the other parties – probably the DA. Such a coalition will be uncomfortable for both parties but may see improvements in the management of some key sectors of the economy if the DA becomes more influential.”

That prediction has come substantially true with the new Government of National Unity (GNU). Our faith in the voting public in South Africa has been substantially vindicated. From the poorest squatter to the wealthiest business executive, they have sent a clear message that:

- Corruption in government is unacceptable.

- The ANC’s role in getting rid of apartheid does not guarantee its political dominance indefinitely.

- The DA represents an essential element of administrative and economic reform in the country, because it is seen as incorruptible and capable of excellent first-world administration.

- Extremism, populism, nationalization, and tribalism are on the radical fringes of political opinion in our society and can never gain control of the country.

- All race groups are essential to the future success of the country and must work together to find solutions to our problems.

It is also now clear that South Africa has a constitutional democracy that is working. There was almost no violence and the elections occurred smoothly and were generally accepted, both locally and internationally, as free and fair. This is something which cannot be said for many countries around the world, and especially those among the BRICS nations and in other emerging economies.

All of these outcomes are enormously good for the South African economy and our reputation with international investors. The result has been a surge in the value of the rand and JSE. We cannot expect the coalition of the ANC and DA to be smooth. They have been archenemies for thirty years. But now the electorate has insisted that they find each other and create a workable compromise. Of course, we must not lose sight of the fact that the rand is also benefiting from a massive shift towards “risk-on” as Wall Street and the stock markets of the world are breaking new record highs.

There already have been significant areas of disagreement among the various parties which make up the GNU. The ANC and DA already disagree on such important issues as the recently implemented National Health Insurance (NHI), policies of affirmative action and the redistribution of land without compensation. However, we see more areas of agreement than disagreement and we believe that compromises can and must be reached.

A further complication is that there are now ten parties in the GNU and even the EFF is seeking to be a part of it. This will complicate the ability of the GNU to make decisions and will make the allocation of cabinet positions difficult. It is easier to get decisions from four parties (which is where the GNU began) than from ten and the EFF’s inclusion might be a deal-breaker for the DA and some other parties resulting in the agreement falling apart.

The GNU will face a difficult task to implement reform in South Africa. That task must begin with the appointment of competent people to key positions in government and in state-owned enterprises (SOE). Those appointments must be based on merit and not on race or political affiliation. In a word, South Africa must become a meritocracy. The Vulindlela program initiated by President Ramaphosa in 2020 has had significant success in streamlining and improving various areas of the economy. It is supported by both the ANC and the DA as a collaboration between government and the private sector to fix areas of the economy that are broken. Its most notable success to date has been to open the way for the private sector to implement large scale renewable energy projects and so put an end to loadshedding. But it has also improved the visa application system, improving tourism and is working on Transnet to improve logistics in the rail and port system. Its next key project could be to investigate the dozens of malfunctioning municipalities to try and improve their performance.

The greatest single problem that the GNU will face is the question of debt consolidation. In inherits a fiscus where R1 in every R5 collected in taxes (20%) has to go to just pay the interest on the national debt. The new government will have to manage its expenses very carefully to continue with debt consolidation. The continued appointment of Enoch Godongwana as Minister of Finance and the stability of the leadership at the Reserve Bank are a major factor in ensuring this. But there will not be much spare cash to fund new “feel-good” initiatives and the members of the GNU will have to make difficult compromises to balance the books and keep the national debt from spiralling out of control.

On the positive side, the potential for further private/public partnerships should now be much greater than it has been. The private sector has already shown what it can do in the electricity sector and is poised to improve Transnet’s logistics and port management. We see this type of improvement as the key to future economic reforms that will lead to lower unemployment and stronger tax collections going forward. The danger is that the GNU will not be sufficiently stable to allow these reforms to reach fruition and to become entrenched. Both the ANC and the DA will have to make significant ideological compromises to keep the GNU in place.

In South Africa between 2002 and 2010, every 1% increase in the annual growth of gross domestic product (GDP) results in a 0,67% improvement in the unemployment rate. This shows the strong relationship between the growth of the economy and the level of employment. Indeed, the only lasting way to create more jobs is to increase the size of the economy more quickly than the working population is growing. After 2010, the South African economy entered a period of significant decline with the average GDP per person falling from $8200 to the current level of $6400. Investors, both local and international, are now hoping that the government of national unity (GNU) can reverse that decline.

The Center for Development and Enterprise (CDE) advocates that senior people in the government should have to re-apply for their positions in the GNU from scratch. They could then be judged on their past performance and proven areas of competence. This would obviously be ideal because it would force the existing incumbents to justify their continued involvement. However, it seems more probable that these critical positions will be allocated as a result of “horse-trading” mostly between the ANC and the DA. Hopefully, President Ramaphosa will take this opportunity to get rid of some of his most radical and damaging opposition within the ANC like the Minister of Minerals and Energy, Gwede Mantashe.

The Rand

The rand is a direct reflection of two sometimes opposing forces:

- The evolving political situation in South Africa

- The current significant shift towards “risk-on” among international investors

The news that the ANC and DA had had a disagreement took the rand down about 50c against the US dollar between 21st and 27th June so that it reached R18.50. That problem appears to have been somewhat ameliorated now and the currency has strengthened to R18.20. At the same time the rand has benefitted from Wall Street’s series of new record highs which has encouraged overseas investors to take up some of South Africa’s high-yield bonds and cheap equities.

The balance between these two forces fluctuates daily, but in our view, both will resolve themselves such that the rand strengthens against hard currencies – at least in the medium term. The immediate dangers are that Wall Street enters a new correction and/or that the DA decides to walk away from the GNU (which seems unlikely to us).

The GNU could easily herald a new era of rand strength as overseas cash pours into this country to take advantage of relatively high returns and reduced political risk. If this occurs it will be good for both the inflation rate and share prices.

Economy

Gross domestic product (GDP) shrank by 0,1% in the first quarter of 2024 after growing just 0,3% in the fourth quarter of last year. The only sector that was positive was agricultural output, which rose 13,5% in the first quarter. The second quarter is expected to be much better overall, because there should be no loadshedding. Growth for the whole of 2024 is expected to come in at around 1%. Economic growth is still well below the levels needed to absorb school-leavers into the labour market. Obviously, the development of the GNU will have a major impact on future growth prospects.

The petrol price fell R1.25 last month and looks set to fall by at least R1 this month. The lower price will give consumers some welcome relief and help to keep the level of inflation down. 93-octane fuel is expected to fall by over R1 per litre and diesel is coming down 30c a litre. Consumers, who are battling with high interest rates and other difficulties in the economy, will now have a little more cash for discretionary spending and businesses will benefit from a noticeable drop in transport costs. For the price declines to remain, the rand will have to continue to perform well against the US$ and the oil price will have to remain where it is at around $85 per barrel (for North Sea Brent). The uncertainty surrounding the GNU will have a major short-term impact on the rand.

The level of employment in South Africa fell by 67 000 jobs in the first quarter of 2024. Full-time employment fell by 29 000 jobs and part-time employment dropped 38 000 jobs. Salaries and wages fell by 0,8% on average during the quarter. Over the year to 31st March 2024, however salaries and wages rose by 5%. Christmas bonuses fell by 25% at the end of 2023 which led to a decline in year-end spending. Over the whole year to the end of March 2024 bonuses were up by 0,5%.

The positive outcome to the election has substantially reduced the risk in the South African economy and improved its prospects. According to Standard Bank, this should mean that interest rates are reduced twice before year-end by a total of fifty basis points. This forecast is in line with expected rate cuts in America and follows a trend towards reduced rates in other countries. Falling interest rates is generally positive for equities because it means lower interest bills and an increased availability of loan finance. The JSE is already following other markets to new record highs, and we expect that trend to continue. The Reserve Bank is expecting inflation to return to the mid-point of the target range (4,5%) in the second quarter of 2025.

“Operation Vulindlela” has been very successful in removing red tape and bureaucratic impediments to business in South Africa. This is especially true in the area of electricity generation where the private sector has moved rapidly to build massive new renewable energy installations. The continued implementation of these reforms could see growth accelerate and the rand strengthen. The Bureau for Economic Research (BER) says that the countries new administration simply needs to continue with Vulindlela to improve growth prospects, especially now with projected reforms at Transnet.

The World Bank regularly ranks the various ports around the world according to how efficient they are and their turnaround times. In the latest ranking of 405 ports, Cape Town is the worst port and Durban is ranked 398. Coega (Ngqura) is the second worst with Gqeberha at 390. These rankings show that Transnet is seriously holding back the South African economy by preventing exports from leaving and imports from arriving. There are efforts now to get the private sector involved. The private sector has been consistently replacing various previously government functions in South Africa – such as the Post Office, health care, education and electricity generation. We expect that trend to continue and gain momentum.

The Afrimat Construction Index showed that activity in the construction sector in the first 3 months of 2024 slowed down – due to the high level of interest rates and uncertainty over the results of the elections. For the last three quarters of 2023 the index showed significant growth as public/private partnerships financed the implementation of renewable energy projects. Only two elements of the index showed any growth and the value of building plans passed fell by 23%. The construction industry is a major employer, so the lower level of activity is having an impact on the unemployment level.

Agriculture is a key component of the South African economy. It is a major employer and its success or failure impacts on the lives of the millions of people who depend on a few acres of subsistence farming for food. The El Nino weather phenomenon has a direct impact on crop levels and the drought this year had a significant impact on the production of summer grains and oilseed. The drought combined with Transnet’s logistics problems and a lack of municipal service delivery resulted in a drop in confidence in the sector. There have also been some problems with disease with certain farm animals. Despite all these problems agricultural exports rose by 6% in the first quarter, mainly due to livestock, wine and horticulture.

The Reserve Bank says that both the equity market and the bond market in South Africa are less liquid than they used to be. Government bonds now make up 81% of all bonds as opposed to 60% in 2008. The share market too has far fewer listings and has seen a drop-off in volumes traded. By 31st March 2024 foreigners held only 27,6% of local shares while local institutions had doubled their holdings of overseas equities. This shift away from South African markets can be partly blamed on the high level of interest rates. It means that local institutions are carrying much more of the risk in the local bond market. One factor is South Africa’s “grey listing” by the Financial Action Task Force (FATF) in March 2023. Steps are being taken to get South Africa off that list, but progress has been slow.

A recent United Nations report shows that 23% of children under five in South Africa are starving and at risk of malnutrition. This situation is a severe indictment of the ruling ANC – despite the massive and pervasive social grants system in this country. What it shows is that social grants are in no way a replacement for gainful employment. Unemployment rates of above 30% of the working population are a result of inefficient management of the economy and excessive red tape and bureaucracy. The rampant poverty in South Africa explains the ANC’s poor performance in the recent elections. Ramaphosa has spent too much time trying to resolve problems within the ANC and not enough time working to reform the economy.

Bitcoin

In the Confidential Report for May 2024, published two months ago at the Bitcoin cycle low, we pointed out that the price had made a descending “double top”. Then, on the 24th of May, three weeks later, we pointed out that the double top had become a descending triple top - which is probably the most bearish charting formation you can get. After that, the price of Bitcoin made a third lower top and has been falling steadily ever since. Consider the chart:

The chart shows the three tops – each lower than the previous – which is a sure indication that the smart money is selling out of Bitcoin in anticipation of a significant fall. At the same time, the Bitcoin price has broken back below its previous record high of $68536. Technically, the coin is now in a steady downward trend and is moving towards its cycle low of $59059 made on the 2nd of May 2024. If that low is broken, then you can expect the price to collapse.

So, once again, we advise that if you have them, sell them - and if you don’t have them don’t buy them.

Comparative Relative Strength

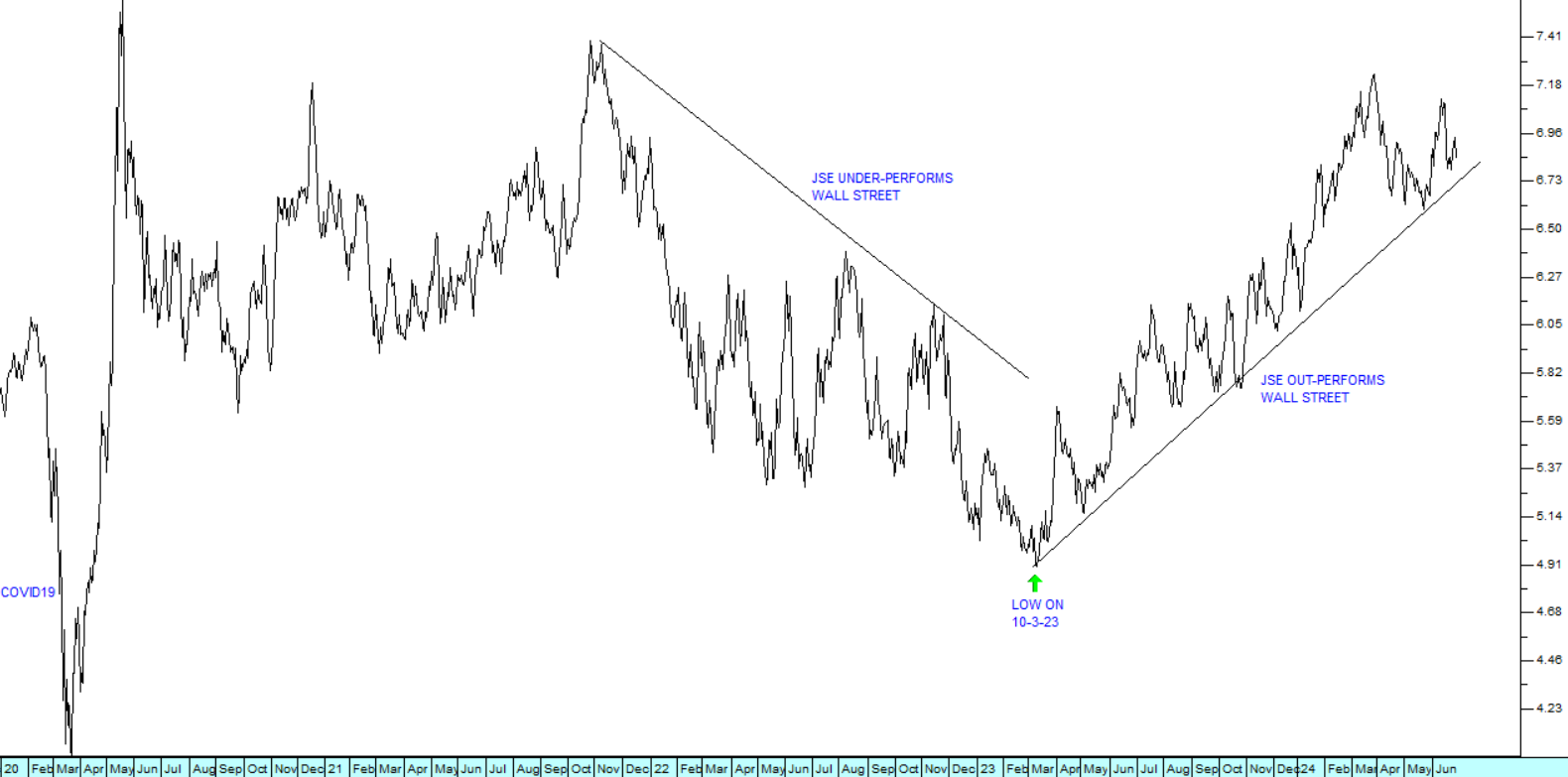

The comparative relative strength indicator (CSRI) is one of the most interesting indicators in your charting software. It is calculated by dividing one data stream by another and then drawing a chart of the result. For example, if you divide the S&P500 index by the JSE Overall index then the result looks like this:

This shows that when COVID-19 became a major factor in equity markets in March of 2020, the JSE under-performed the S&P500 because international investors became very risk-averse and moved their money out of emerging economies and into safe havens. Then in the following 2 months from 20th March to 20th May 2020, the JSE performed far better than Wall Street.

The chart also shows that from November 2021 until March 2023 Wall Street was doing better than the JSE – and then the trend changed and for the past 18 months the JSE has been beating Wall Street fairly consistently.

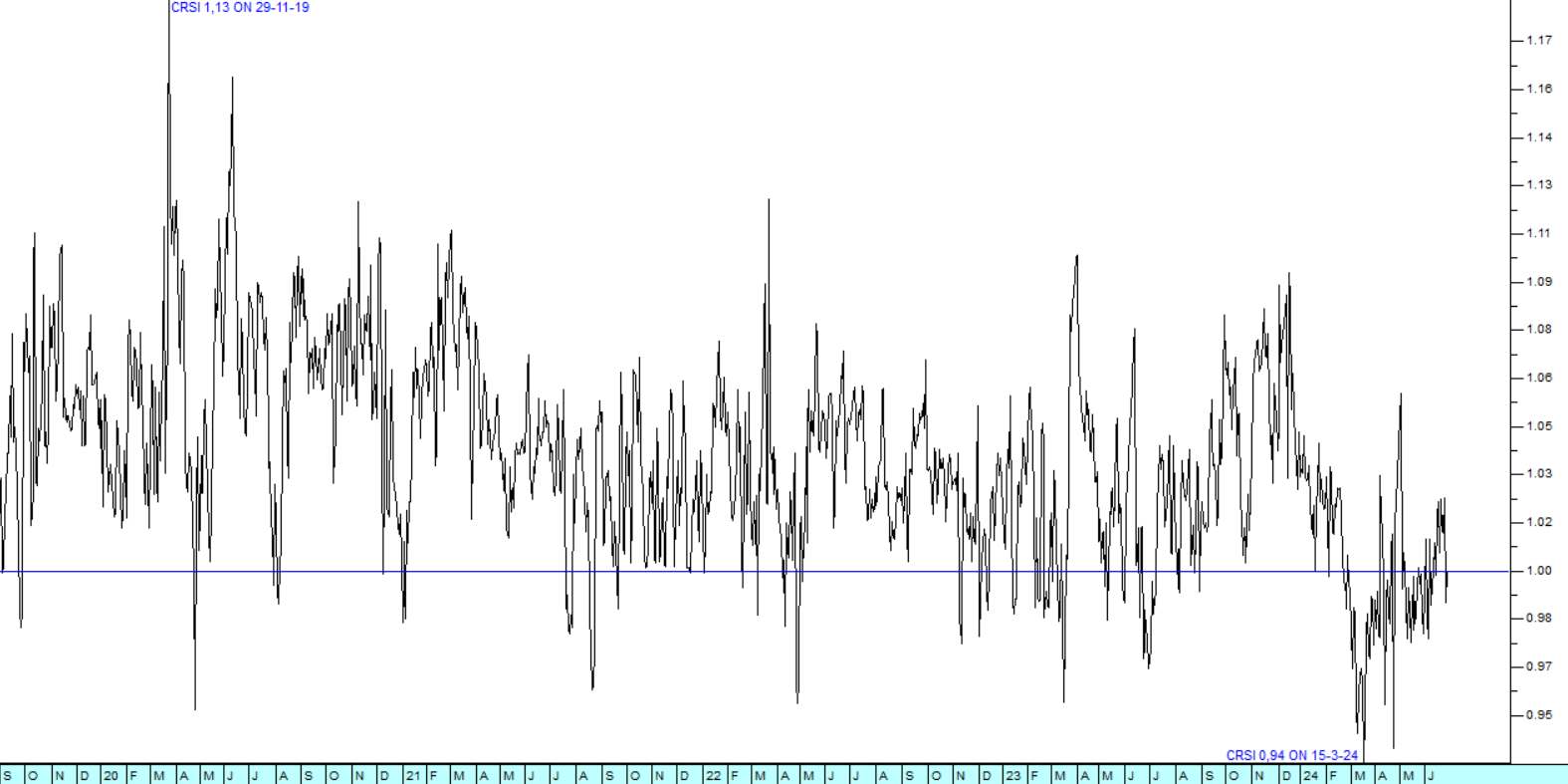

This illustrates the use of the CSRI to show when one data stream is out-performing another. Let us consider another example – the price of the Krugerrand divided by the rand price of gold.

Logic would suggest that the price of the Krugerrand should be very much in line with the rand price of gold. In other words, when the gold price goes up in rands the Krugerrand price goes up and vice versa. But when you look at the CRSI you see that there are times when the Krugerrand is actually cheap in relation to the rand price of gold – and times when it is expensive. Consider the chart:

This chart shows that on the 29th of November 2019 the Krugerrand price was 13% higher than the rand price of gold and on the 15th of March 2024 it was 6% below it. The blue horizontal line shows where the two indicators were at parity. In general, we would expect the Krugerrand to trade slightly above the price of gold bullion because it in a much more convenient and tradable/transportable coin form. But it is interesting to note that there are times when Krugerrands are both under-priced in terms of the rand price of gold and significantly over-priced.

This relationship would obviously have great significance for an investor seeking to either buy or sell Krugerrands.

The CRSI can be used to identify and exploit any relationship between any two data streams in your software.

Companies

RCL (RCL) and RAINBOW (RBO)

The unbundling and listing of Rainbow Chicken on the JSE with effect from the 26th of June 2024 show the enormous release of shareholder value which can come about as a result of this type of activity. In its financials for the six months to 31st of December 2023, published in the Stock Exchange News Service (SENS) on the 4th of March 2024, the board of RCL expressed the opinion that both RCL and Rainbow would benefit from an unbundling of Rainbow. This was the first official indication that the investing public had of this unbundling.

The chart below shows the fact that a few days before the announcement, the share traded enormous volumes at a slightly better price. In the 30 trading days before the 29th of February 2024, the average volume traded every day was 52 060 shares. On February the 29th 2024, 36,44 million shares changed hands – and the price ticked up to 1020c. Small increments in price combined with massive increases in volume are a sure sign of insider trading.

The result was a strong On-Balance-Volume (OBV) buy signal on 29th of February 2024. The increase in volume on the 29th of February 2024 is clearly a consequence of people inside the company, who knew what was about to happen, buying up as many of the share as they could lay their hands on before the public announcement. Such trading is illegal, but it is a common feature of the JSE and other markets.

Whenever there is a significant event that is likely to have a strong impact on the share price (usually the announcement of some sort of corporate action) there is always a group of people inside the company who are privy to that information before an announcement is made. Some of them will almost always use that privileged inside information to their advantage in the market, usually indirectly so that the trades cannot easily be traced back to them.

The point is that these insiders cannot hide their activities because they will always be visible in the volume traded. The OBV indicator is specifically designed to highlight such trading and exploit it. Consider the chart of RCL:

The top chart is a simple candle-stick chart showing each day’s trade and the long-term downward trendline which was broken on the 1st of May 2024. The middle chart is an OBV chart which shows the buy signal given on the 29th of February 2024, 4 days before the publication of the company’s financials in which the board’s position was made clear (that happened on the 4th of March 2024). To understand how the OBV is calculated read our article - On Balance Volume.

The bottom chart is a volume histogram showing the number of shares which changed hands on each trading day. The massive spike on the 29th is clearly visible.

Notably, we added RCL to the Winning Shares List (WSL) on the 1st of May 2024 at a price of 1050c. Following the unbundling the share price last Friday (28-6-24) was 1005c and Rainbow closed at 469c. This means that investors who bought RCL when we added it to the WSL made a profit of 40% in two months.

MURRAY & ROBERTS (MUR)

A company’s debt is critical in establishing the risk inherent when investing in its shares. High debt levels expose the company to high interest and capital payments and can swallow up a large part of whatever profits it makes. Low debt levels give the company the headroom to invest in further growth either organically or by acquisition.

At one time, Murray and Roberts (M&R) was one of South Africa’s largest construction companies and a favourite institutional stock. On the 29th of October 2007 its share price reached a peak of R108.25 which gave it a market capitalisation of almost R360bn. On the 31st of August 2023 it shares were trading for just 58c and it had a market capitalisation of R257m.

The collapse of a blue-chip company can always present the private investor with an opportunity – provided the company is not going to end up being liquidated. The trick is to first establish that the company will survive and then to pick the right moment to buy in - and the danger is that you buy in too early, before all the bad news has been discounted.

But whatever happens, you always have the comfort of knowing that in 2007 there were institutional fund managers filling their pockets with M&R at R108 per share – so buying in at these lower levels, you are doing far better than them. And, of course, if your timing is off and the share falls further then your stop-loss will get you out with a minimal loss.

Technical analysis provides the best mechanisms to give you a reasonable assurance that the bottom is behind you. This is because the chart reflects that activities of the insiders in the company who will always know far more than you do about what is going on.

Consider the chart:

Here you can see that the M&R share price reached a bottom between September and December of 2023. There was an extended island formation which began and ended with low points (the red arrows) at 58c on the 31st of August 2023 and 59c on the 7th of December 2023.

A formation like this, followed by an upside breakout, shows that all the bad news has almost certainly been fully aired and discounted. It indicates that a point of capitulation has been reached where even the stale bulls have accepted that the company is hopeless. The upside breakout came a few days later when the share surged to 106c – and that was when we added it to the Winning Shares List (WSL).

Since then, it has more than doubled to close last Friday (28/6/24) at 214c.

From a fundamental perspective, the company has managed to sell off assets and so reduce its debt to manageable levels. This substantially reduces the risk for investors, making the share far more attractive.

On the 31st of December 2022, the company had debt of just under R2bn which compared to its market capitalisation of R1,3bn. A year later, on the 31st of December 2023, it had managed to reduce that debt to just R247m and had a market capitalisation of R644m.

One final point. With the newly elected Government of National Unity (GNU) there is a significant opportunity for companies like M&R to win contracts to rebuild South Africa’s dilapidated infrastructure – so we believe that it is well positioned to take advantage of a flood of both local and international investment capital into this country.

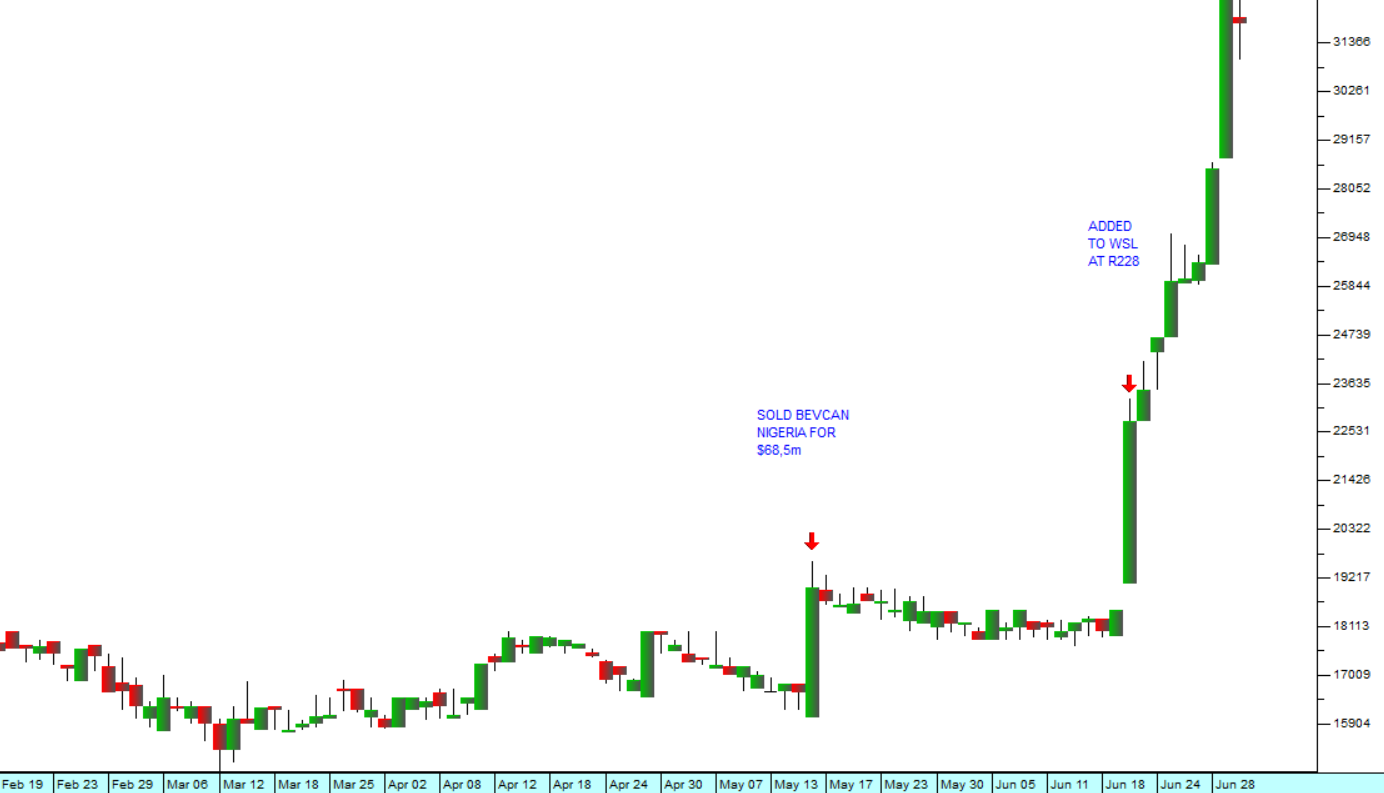

NAMPAK (NPK)

In November 2014, Nampak had a market capitalisation of R32bn. Five and a half years later, by the time COVID-19 had decimated equity markets world-wide in March 2020, that had been reduced to less than R1bn. And in the ensuing 4 years it has never really managed to recover. But like all large international blue-chip companies that have fallen out of favour, it eventually undertook a major restructuring and began to see some significant benefits.

From an investor’s perspective, the turnaround became important with the announcement on the 16th of May this year of the sale of its Nigerian Bevcan operation for $68,5m. This enabled the company to reduce its debt to more manageable levels.

At the same time the company has been making strides in improving its working capital management and reducing its costs.

On the 16th of May 2024, with the sale of Bevcan Nigeria, the share produced a strong on-balance-volume (OBV) buy signal at R190 per share. That was followed on the 20th of June 2024 by a second more consistent OBV buy signal.

As a consequence of this second OBV signal, we added it to the Winning share List at a price of R228 per share. On Friday last week it closed at R285.50 per share – a gain of over 25% in just 9 days. Consider the chart:

We believe that Nampak will continue to improve steadily over time.

← Back to Articles