EOH Collapse

23 October 2023 By PDSNETThe story of EOH over the past 22 years on the JSE is very instructive for private investors.

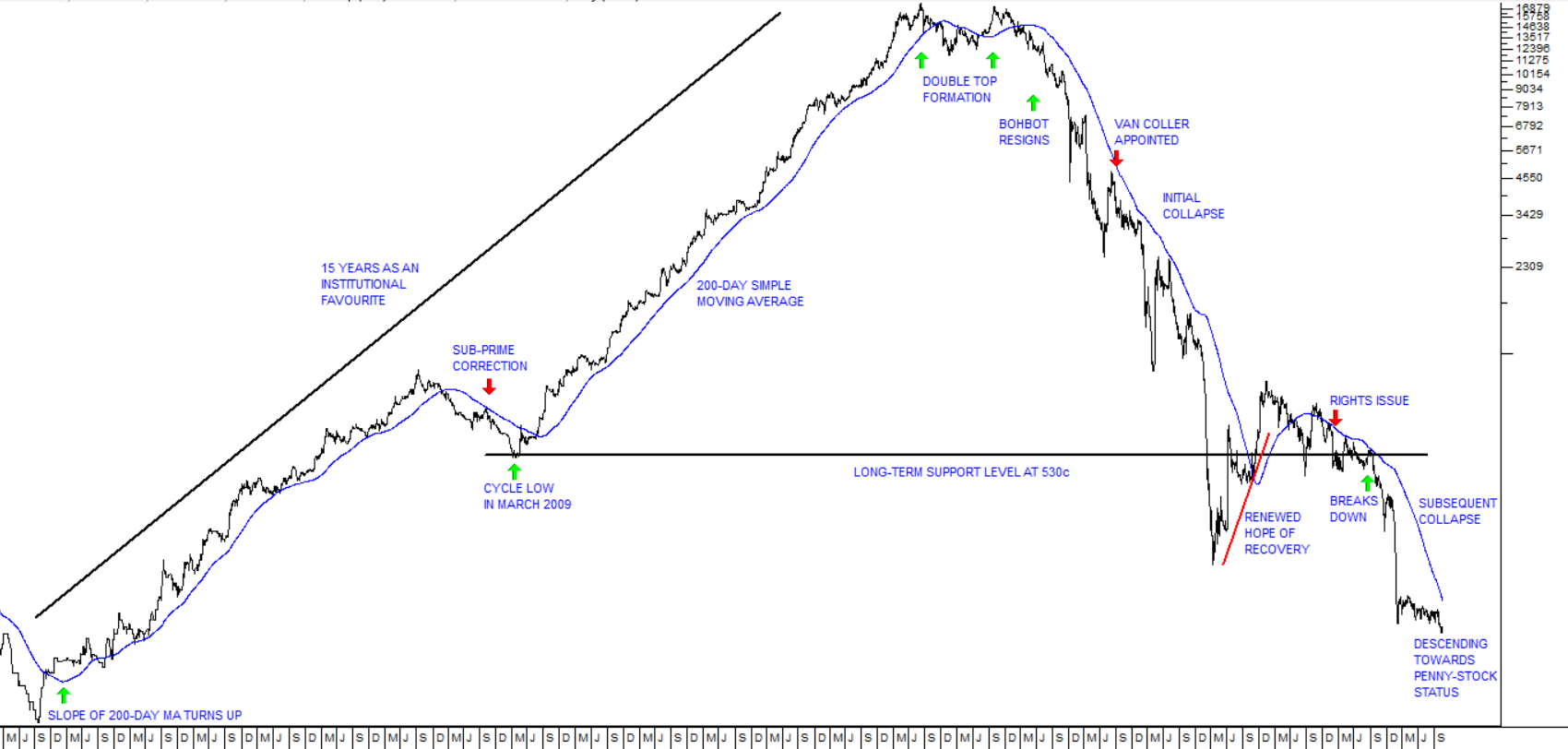

On Tuesday, 18th September 2001, 22 years ago, EOH shares closed at 70c a share. They eventually reached a high point of R174 a share at the end of September 2016. During those 15 years, interrupted by the sub-prime crisis in 2007/8, EOH had become an institutional favourite and was part of every large portfolio in South Africa.

The founder of the company, Asher Bohbot, was CEO for 19 years from August 1998 until June 2017. The company listed on the JSE in the middle of the “dot-com” crash of 1998 and was one of the few survivors. It grew rapidly by acquisition, mopping up a wide variety of start-ups and hopefuls in the IT sector.

Then, in 2016, rumours began to circulate that the company had obtained government contracts through bribery and corruption. Eventually, Bohbot was forced to resign and the share collapsed. It fell to a low of 267c in March 2020 with the added negative of the COVID-19 pandemic.

On the 3rd of September 2018, Stephen van Coller was appointed as CEO to clean up the mess and turn the company around. He restructured the business completely, rationalizing the hundreds of subsidiaries into four divisions, selling off non-core assets, and finally this year conducting a rights issue and reducing the company’s debt.

The effects of van Coller’s efforts can be seen in the share price, which rallied back to above 930c in January 2021 on renewed hope that the company could be saved. Consider the chart:

From when the 200-day moving average turned up in February 2002, this was one of the best shares to own on the JSE. Its meteoric rise was only temporarily interrupted by the melt-down as a result of the 2007/8 sub-prime crisis.

Technically, it made a clear “double top” formation with highs in the middle of 2015 and then 2016 signalling that the bull trend was probably over. The smart money was clearly dumping their shares while the going was good. The resignation of its much-vaunted CEO in June 2017 confirmed the bad news and the share plummeted.

The market began to believe in the new CEO’s efforts to turn the company around in 2020, once the shock of COVID-19 began to fade, however the reputational damage had been substantial, and the recovery was slow and difficult.

In its results for the year to 31st July 2023 the company announced that van Coller was to resign as CEO. At the same time, it reported that it had managed to reduce the company’s loss from 62c a share in the 2022 year to just 20c in 2023.

Looking at the balance sheet, the company still has R762,5m worth of intangible assets – mostly consisting of the goodwill arising from various acquisitions. The company’s total equity was just R587,7m – which means that if the intangible assets are disregarded, the company still has negative equity. And this is after having conducted a very diluting rights issue to raise R500m in February this year.

Investment analysts are not optimistic. Van Coller’s resignation leaves a company which still has a very shaky balance sheet and is still loss-making. From a private investor’s perspective, the share is technically again in a downward trend. It has broken down through the long-term support level at 530c and may well fall much further. The best approach is to wait at least for it to break up through the 200-day moving average before investigating further.

DISCLAIMER

All information and data contained within the PDSnet Articles is for informational purposes only. PDSnet makes no representations as to the accuracy, completeness, suitability, or validity, of any information, and shall not be liable for any errors, omissions, or any losses, injuries, or damages arising from its display or use. Information in the PDSnet Articles are based on the author’s opinion and experience and should not be considered professional financial investment advice. The ideas and strategies should never be used without first assessing your own personal and financial situation, or without consulting a financial professional. Thoughts and opinions will also change from time to time as more information is accumulated. PDSnet reserves the right to delete any comment or opinion for any reason.

Share this article: