The Confidential Report - February 2021

America

The relatively calm installation of Joe Biden as president and the Democratic Party’s control of Congress were appreciated with relief by markets worldwide. The S&P has risen by almost 18% from its low of 3270 on 30th October 2020 to its recent high of 3855 on 25th January 2021. Biden has promised further substantial stimulation of the economy, and the roll out of vaccines in first world countries has given some hope that the battle with COVID-19 may now be won. Some of the various vaccines appear to be effective against new strains of the virus which have emerged and caused a second wave.

Technically, the S&P500 index was overdue for some sort of correction which has been taking place this week. Consider the chart:

Here you can see the V-bottom caused by COVID-19 in March/April of 2020. The recovery was followed by a 7,1% correction in June 2020, a 9,6% correction in September 2020 and a 7,1% correction in October 2020, immediately before the US election.

We are currently in the throes of a 4th correction which, as of Friday last week, had seen the market fall by 3,66%. This correction is probably overdue, given the sharp rise of the market since Biden was elected, and the market may well fall further. In our view, however, it remains a correction within an overall bull trend and therefore presents a buying opportunity.

There can be no doubt that Wall Street is trading at historically high price:earnings multiples. This has led to a rash of bearish sentiment fuelled by various stock market gurus. Click here for the article: Elimination of the Bears

It is well to remember that since its low of 676,53 made on 9th March 2009, the S&P has gained 470% in almost 12 years – a post-World War II record for any bull market. Quite naturally, some experts are staking their reputations on calling the top.

In our view, these bears will be proved wrong over the next six months and their reputations will suffer accordingly. Certainly, we will have corrections (because nothing in the markets moves in a straight line), but the underlying bull trend will remain in tact and shares will move inexorably higher.

The JSE will inevitably be dragged up to higher levels despite the parlous state of the South African economy and our undeniable fiscal problems. Right now, however, as this correction reaches its apex, there will be opportunities for private investors to buy high quality shares at good prices.

Political

The “step-aside” battle between the Ramaphosa camp and erstwhile supporters of ex-president Jacob Zuma is becoming the benchmark of ANC integrity. Ace Magashule is refusing to step aside, despite the fact that he has been arrested and charged, while Ramaphosa is trying to implement a decision of the ANC’s National Executive Committee that those who are charged with a crime should step aside to protect the name of the party. Ramaphosa is said to favour a compromise which involves the affected person explaining themselves to the ANC’s Integrity committee and then that committee will make a recommendation to the NEC on the person’s status – but the ANC’s Integrity Committee has now said that Magashule should resign. He is still there, and the ANC is doing what it has always done – talk and postpone.

It is becoming clear, with the latest revelations from the Zondo Commission, that the rot within the ANC runs much deeper than was previously suspected. The task of cleaning up the mess and regaining the faith of the South African public seems almost insurmountable. President Ramaphosa has boosted the staffing at the National Prosecuting Authority, but the extent and depth of the corruption is so monstrous that it will take years to investigate and secure convictions. Perhaps the answer in the short term is to make a salutary example of a few of the worst and highest profile offenders.

Economy

The “second wave” of the pandemic became official in South Africa on Wednesday 9th December 2020 when there were over 6700 new cases spread across all provinces, including Natal and Gauteng. The wave is associated with a new more infectious strain of the virus. Subsequently, the daily infection rate peaked at over 22 000 with between 500 and 1000 deaths per day. Apparently, the spread began during the Festive Season, mostly among younger people attending indoor gatherings where alcohol is consumed. By the end of January 2021, the second wave was declining and definitely past its peak. The restrictions implemented obviously hurt business, especially liquor outlets (which were closed), restaurants and the tourist industry. It is now anticipated that there will be a third wave, probably in July or August this year. The first case of the British variant (B117), which has a higher death rate than the South African variant, has been found in the country. The first vaccines have arrived here now, and a program of vaccination will commence, but it is unlikely to have much impact on the third wave due to the slowness of the roll-out.

Obviously, cutting the funding of SARS at this critical time does appear foolish. SARS is the government agency charged with collecting taxes and its funding has been cut by R238m in the October 2020 mini-budget. In fact, SARS funding should be increased from its current level of around R10,4bn to R14bn so that it can fill the 800 vacancies which it currently has. Putting money into SARS is effectively an investment for the fiscus which will substantially improve government finances over time. Edward Kieswetter has made a presentation to Parliament to urge that SARS funding be increased and that to cut their funding would endanger the re-building of SARS. The international norm is for a good tax authority to receive about 1% of GDP, while SARS is currently getting only 0,73% - before the cuts.

From inside South Africa it is often difficult to get a true perspective on the state of our economy and its prospects. So, it is interesting that JP Morgan, a highly respected international bank, is recommending that its investors invest in this country and particularly its shares. In its advice for 2021, the bank is suggesting that investors should be “over-weight in South African equities”. JP Morgan says that our industrial and financial shares look cheap by international standards. Notably, the JP Morgan picks include two of our banks – Standard and Capitec. JP Morgan also believes that the rand is under-valued against first world currencies – a position which we have maintained for at least two years. They are expecting the rand to continue to appreciate.

The November purchases by the Reserve Bank of government bonds mean that it now has bought about R41bn worth of those bonds in the open market. The Reserve Bank’s position is that it will sell those bonds back into the market once conditions improve. However, the further downgrades of the South African economy by the major ratings agencies suggest that conditions will not improve anytime soon. Ultimately, if the Reserve Bank writes off the money used to buy those bonds, then the purchases become a form of “quantitative easing” (Q/E). The Reserve Bank says that it does not want to resort to Q/E because it still has positive interest rates which could be further lowered to stimulate the economy. However, the lack of liquidity in the bond market is due to the government’s excessive borrowing requirement and the Reserve Bank’s bond purchases have been primarily necessitated to accommodate that – that virtually amounts to Q/E in all bar the name. As the economist, Peter Attard Montalto, said last year, “If it looks like a duck and quacks like a duck, then it probably is a duck”.

The better-than-expected GDP growth figures for the third quarter mean that after nine months of 2020, GDP was down 7,9%. Given that the 4th quarter may also be positive, it seems that the full year will be down by less than 7% - as opposed to the -8% which economists were predicting. Our view has always been that the economy would recover more rapidly than economists were predicting and that appears to be the case, although the second wave of the pandemic and the return to level 3 lockdowns is a negative. More or less no matter what happens, growth in 2021 will be considerably better than it was in 2020. Obviously, much of this growth has been due to the TERS payments (which have now stopped) and the low interest rates which will have to be unwound, probably starting some time in 2022.

Retailers have reported that Black Friday sales and Christmas sales were disappointing with physical store sales down. The November 2020 Bankserv economic transaction index was down for the first time since April and retail sales for the whole month fell by 4%, year-on-year. Obviously, the return to modified level 3 lockdown with the ban on alcohol sales was a major negative. It seems unlikely that a full lockdown will be invoked, however, as that probably would not halt the rate of infection, but it would cause substantial economic damage.

The record trade account surplus in the 3rd quarter indicates that South Africa is benefiting from rising commodity prices and growth in the world economy – while at the same time, local consumer spending is very low. The surplus was almost 6% of GDP. It was also based on very low imports as local consumer spending remains depressed. In the end, the South African economy will have to export its way out of this post-COVID-19 recession – as it has from previous recessions. It is also clear that commodity exports are what is currently sustaining the economy through this crisis.

The construction sector seems to be benefiting from increased construction spending by the state in the post-lockdown period. This is supported by the jump in the Afrimat construction index to 115,9% in the third quarter of 2020 – compared to 65,4% in the second quarter. PPC, which recently reported its results for the six months to 30th September 2020, also showed strong growth in cement sales. Clearly, this time, the government has been acting on its promises to stimulate the economy through infrastructure spend. 62 projects have been identified for the infrastructure spend.

The government’s unexpected win in the Labour Appeal Court means that it will not have to pay civil servants the final pay increase in its three-year deal with them. This will save the Treasury R38bn, but it may make further multi-year wage negotiations very difficult. The international ratings agencies may now feel that the 3-year wage freeze is possible after all. The unions are, of course, appealing the judgement. The civil service unions are busy consolidating their wage demands for presentation in February as the wage negotiations get under way. The government has already made it clear in the October 2020 budget that there will be no civil service pay increases for the next 3 years – and the entire budget is predicated on that. So, the negotiations are likely to be stormy and ultimately result in strike action. South Africans will probably not be too disturbed by a strike in the civil service. Indeed, many of them will not be affected at all, especially in the early stages. The union movement in South Africa has been substantially weakened in recent years and may not have the leadership to sustain a prolonged strike. One thing is certain – South Africa simply cannot afford to pay for such a large civil service.

The fiscal debt is around R3,8 trillion – which equates to 82% of GDP and brings South Africa much closer to a debt trap where just affording the interest payments on this massive amount are becoming unaffordable. About a quarter of that debt is due to government efforts to compensate for COVID-19 – so the emergence of a second wave is a major concern. Clearly, the widespread and rapid implementation of vaccinations is now essential for our economic survival. Ninety-one (NY1) says that the government’s debt is rapidly becoming unsustainable. It says that soon 24% of government revenue will be needed simply to pay the interest on the debt during the next 8 years. Debt will rise to around 95% of GDP. Previously, only about 13% of government revenue was needed to pay interest. The COVID-19 recession has resulted in a sharp fall in tax revenue at the same time as there have been more demands on the fiscus.

It is apparent that the government has essentially exhausted fiscal remedies to stimulate the economy further. The President has said there will be no further stimulus. That leaves monetary options. The level of interest rates could still be reduced further with the repo rate at 3,5% (having been reduced by 3% last year) but the MPC has decided for the third time to hold rates unchanged with a 3:2 majority. The second wave of the pandemic and new level 3 lockdown restrictions are combining with renewed load-shedding to put more strain on the economy. There is an outside possibility of a further rate cut, but most economists believe that rates will be kept on hold for the meantime. The third ban on alcohol sales had a widespread impact on that industry, leading to bankruptcies and job losses.

The Treasury has been considering how the cost of vaccines can be met. There has been suggestion that a new or higher level of taxes will have to be considered. The possibility of re-allocating funding from other government departments seems remote after the SAA funding debacle. On top of that there is the evidence that the vaccine may not be effective against the second wave of the virus in its mutated form. The South African Revenue Service (SARS) is reporting a revenue shortfall of about R313bn and the cost of vaccinating two-thirds of the population is over R20bn. A once-off tax, which is levied according to people’s income levels is likely.

The impact of the third ban on alcohol sales was substantial. SA Breweries cancelled a R2,5bn investment which it had been planning and Consol glass was in the difficult position of having to keep its furnaces running at a cost of about R8m per day. More recently, Heineken has announced the retrenchment of about 70 staff members. Clearly, the closure also impacted thousands of bottle stores and the wine industry, which is apparently sitting on a lake of wine which it cannot sell locally. Banning alcohol sales does undoubtedly reduce the strain on the country’s medical facilities, but it has had a significant cost to the economy.

The humanitarian crisis developing in Zimbabwe is causing a flood of illegal immigrants to cross the border into South Africa. Zimbabwe is experiencing 400% inflation with 90% unemployment. Obviously, for South Africa, this places an additional strain on the country’s resources at a critical time. Increased crime, further housing shortages and greater unemployment are the probable consequences. Steps have been taken to make the border more impenetrable, but these desperate people are still finding ways. They bring with them the further threat of COVID-19 and other diseases.

The Rand

The second wave, which is taking place throughout the world, has also caused a shift from risk-on back to risk-off which has had an impact on the rand taking it from around R14.50 to the US$ to around R15.50. In our view, this weakness is probably temporary, and we expect the rand to regain much of this ground in the next few months.

The international shift to risk-off following the news of the second wave has pushed the rand down to R15.18 to the US dollar, but it remains relatively strong and could probably absorb further rate cuts, especially with inflation expected to remain below 4% this year. Consider the chart:

You can see here that the rand found support at around R15.30 to the US dollar before the onset of COVID-19 and the risk-off sentiment which accompanied that. We regard the impact of COVID-19 as a technical aberration because it was not caused by any normal economic factor. The COVID-19 risk-off sentiment took the rand as low as R19 to the US$ in late April 2020 when international risk-off sentiment was at its highest. Since then, it has returned to its previous trading range below R15.3 to the US$. This recent strength can be attributed to two primary factors – the renewed strength in commodity prices which is supporting our mining industry and the flood of international cash which is looking for the high real returns (i.e., above 6% per annum) on our government bonds.

There is obviously concern among overseas investors about the indebtedness of the South African government and whether there is sufficient political will for the government to be able to hold the line against the civil service unions. For all that, the zero growth in civil service salaries is built into the budget, it may prove hard to implement in practice. The showdown between the ANC and the unions is long overdue and the outcome will be a critical determinant of the South African economy’s success.

State-Owned Enterprises

The proposed conversion of R100bn worth of the Public Investment Corporation’s (PIC) “power utility bonds” into equity means that public servants will effectively be using their pension contributions to pay off a large chunk of Eskom’s debt – with little prospect of a market-related return. The proposal, first put forward by Cosatu, has now been approved by business and government at the National Economic Development and Labour Council (NEDLAC). Presumably, a portion of the government’s 100% ownership of Eskom will be “sold” to the PIC (which is in any event a government agency) in exchange for its interest-bearing bonds. No more interest will then be paid to the PIC. Like other shareholders they will have to wait for the payment of dividends – which are highly unlikely given that Eskom has made a loss of R20bn in each of the last two financial years. Clearly, the PIC has been strong-armed into making this deal without any consideration of the loss of income which it will inevitably incur. On the positive side, the effective repayment of R100bn of Eskom’s debt will greatly improve the financial viability of that entity. But the Eskom business model is seriously flawed with more and more consumers and businesses seeking to install alternative sources of power.

The Road Accident Fund (RAF) is set to become South Africa’s next major debt problem after Eskom. Claims increased by nearly 22% to R330bn in the current financial year and are expected to rise to about R600bn over the next 3 years. This is state-funded third-party insurance for road accidents – which the South African government clearly cannot afford. The RAF is financed by a levy on petrol and diesel prices which is insufficient to meet all the claims resulting in a growing government debt. Notably, the RAF is spending about R11bn a year just on legal costs…

The revelation in parliament that the Land Bank requires about R7bn to stabilize it and the fact that the Auditor General issued a “disclaimed opinion” on its financial results shows that, once again, this is a government run organisation that has been the subject of corruption and mismanagement. Obviously, this is also a crisis for the country’s farmers who rely on the Land Bank for funding. A bank which normally has conservatively valued land as security should never suffer from defaults – and the Land Bank never has before.

The resignation of the Post Office’s Chief Financial Officer, Khathutshelo Ramukumba after just 3 months in office shows the parlous state of this SOE. The Post Office has been losing money for 13 years and is expected to make another R2bn loss this year. Certainly, this is one SOE that South Africa can probably do without.

Commodities

OIL

The price of North Sea Brent has appreciated by about $8 per barrel since our last Confidential Report on 2nd December 2020. This is a result of further stimulation of the world economy (especially the US) and the resultant rise in the demand for oil. The oil price is a good benchmark for assessing the general recovery of the world economy from COVID-19. Despite the second wave of the virus, most economies are gradually coming back to life. With the advent of Joe Biden as US president, further heavy stimulation of the US economy can be expected. On the negative side, the switch to electric motor vehicles is gaining momentum worldwide with many countries setting a date by which internal combustion engines will be outlawed. Over the next decade, the demand for fossil fuels should decline steadily and their price will fall in tandem. Consider the chart:

You can see here that following the Biden win, oil has been trending upwards in line with expectations of further US economic stimulus and a general recovery in the world economy.

GOLD

To get an idea of what is happening to the US dollar price of gold, it is important to look at what is happening to the US dollar itself. The dollar has been falling against the Japanese yen since 1970. Since December 2016, it has fallen from about 117 yen to the dollar to around 104 yen. At the same time, it has been falling against the euro and in the last few months even against the British pound. Against this background the fact that gold has been in a downward trend against the dollar since August last year indicates that there has been a general shift towards risk-on and away from ultra-secure, zero-return assets like gold. The rand price of gold has also been falling since August last year. Since we believe that the rand will continue to appreciate, the outlook for the rand price of gold is not great.

You can see here that the US dollar price of gold has been in a downward sloping “broadening formation” which reflects the falling interest in assets of last resort and also growing uncertainty.

PLATINUM GROUP METALS

The principal use of platinum group metals is in the manufacture of auto catalysts for the motor industry. As the world economy recovers, we can expect prices to rise – at least until electric vehicles begin to have an impact. The shortage of palladium and rhodium has caused some substitution in platinum which has helped that market overcome its over-supply problems. There are also significant efforts being made to find an alternative use for platinum in the production of fuel cells and other power-related technologies.

Companies etc.

BITCOIN

On 8th December 2017 we wrote an article about Bitcoin, The Bitcoin Bubble, in which we suggested that the run up in its price of $15583 at the time was almost certainly unsustainable and that some sort of major correction would follow. That correction began a 10 days later on 18th December 2017 after the peak of $18786 and the cryptocurrency fell back to $3274 a year later. Now we face a new exponential upward move in bitcoin which dwarfs the first and has seen it rise to over $40 000. Consider the chart:

Our advice is the same. No financial market can sustain such an upward move. If you have the coins, sell them. If you do not have them, resist the temptation to buy them.

BANKS

The banking sector is represented by the JSE Banks index (J835) which shows that the banks have taken a big hit as a result of COVID-19. We believe that this offers the private investor an opportunity – and we have drawn attention to this in the past. Historically, whenever the big banks (Nedbank, FNB, Standard, ABSA and now Capitec) traded on a dividend yield (DY) of more than 5% they represented an opportunity for investment. In March 2020, the banks index peaked at a DY of 10,71% and since then it has risen substantially so that the DY is now 5,83%. At the time we drew attention to the “double bottom” which the banks index made and the support which it enjoyed at those lower levels. Consider the chart:

Institutional investors (pension funds, insurance companies, unit trusts and asset managers) with their massive inflows of cash are constantly looking for high-quality shares to buy, especially when they are cheap. At a DY of 5,83% the banks are still very cheap. Sooner or later the institutions will drive these shares up to more normal valuations around a DY of 3,5%.

PROPERTY

One of the sectors which was down before COVID-19 and has been further badly impacted by the pandemic is property. High quality shares like Growthpoint and Redefine are trading as a massive discount to their net asset values (NAV) and on very high yields (around 15%). This represents a buying opportunity for private investors. We believe that the property index will recover substantially in 2021 and 2022. Consider the chart:

It is apparent from this chart of the JSE Sapy (J253) that property shares are beginning to make a recovery but have not yet broken up through resistance at 288. We believe that the lows of November 2020 will not be revisited and that the index will trend up from current levels.

INVESTMENT CLUB

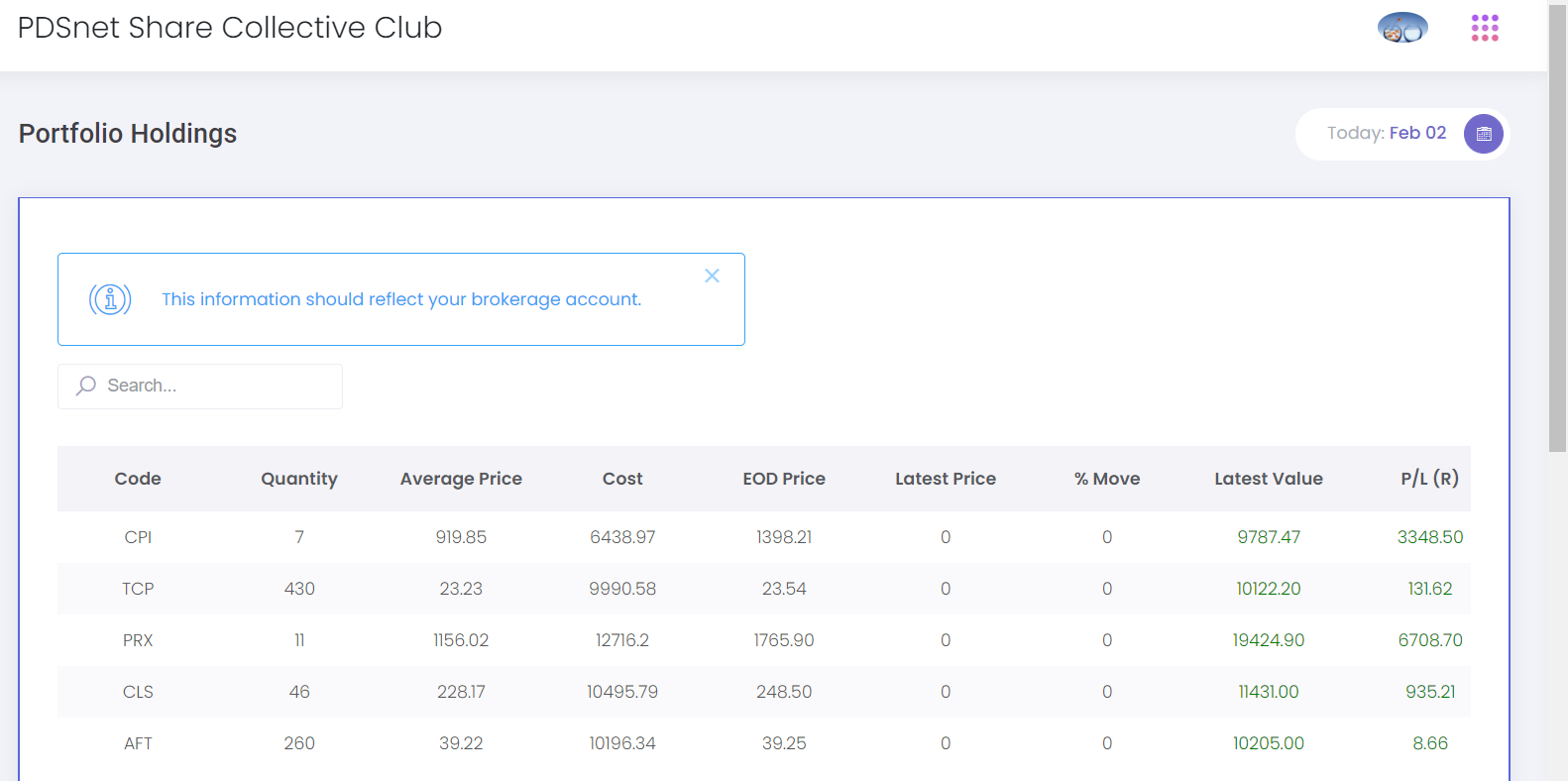

A new free service from PDSnet is that we provide access to our Investment Club software, which enables groups of individuals to set up a JSE investment club and monitor its daily progress. We already have a number of investment clubs running very successfully. Below is an extract from one of the screens showing our in-house investment club’s portfolio as at 10th December 2020. As you can see our members (all employees of PDSnet) had elected to buy Capitec, Transaction Capital, Prosus, Clicks and Afrimat. At the time of writing the club was “in-the-money” on all five investments.

WOOLIES

In a trading update on 25th January 2021 for the 26 weeks to 27th December 2020 the company reported group sales up by 5,3% with Woolworths food in Southern Africa delivering a growth of 12%. The company said, "David Jones (‘DJ’) sales over the 26-week period declined by 8.8% and by 10.5% in comparable stores. Country Road Group (‘CRG’) delivered strong sales growth of 6.7% in the last six weeks of the period, underpinned by new product ranges, particularly in the Country Road business". Headline earnings per share (HEPS) was expected to be between 50% and 60% higher than in the comparable period. Technically, the share collapsed from a high of R106 in November 2015 to around 2558c in March 2020. It has since recovered to 4382c on these latest results and is about to break up through its long-term downward trendline. The current P:E is around 37, but the share appears to have good upside potential. Woollies announced on 14th January 2020 that they had appointed Roy Bagattini, from Levi Strauss, to replace Ian Moir as CEO with effect from 17th February 2020. Consider the chart:

MR PRICE

Mr. Price (MRP) is a retailer of clothing, household goods and sportswear through shop fronts and online in Africa and Australia. Unlike most retailers, Mr. Price receives most of its sales in cash, but there is a growing credit element. Mr. Price has a reputation for being cheaper than other stores. This has been a definite advantage during COVID-19 as consumers tried to stretch the buying power of their income. The company is debt free and has over R1bn in headroom. In a trading update for the 13 weeks to 26th December 2020 the company reported total retail sales up 5,8%. The company said, "Group inflation of 6.8% was driven by price inflation of 3.8% (in line with CPI and lower than the deterioration in the foreign exchange rate) and by lower markdowns". The company said its market share had risen by 2,3% to record levels. The company announced the acquisition of Power Fashion, a group with 170 cash stores in Lesotho, South Africa and Eswatini. In our view, this is a good share in a very difficult industry, especially in the current economic environment in South Africa. Its P:E ratio of 18.4 still seems cheap while the company is well-positioned to ride out these economic hard times and then benefit from any improvement in the economy. Technically, the share appears to be entering a strong new upward trend and is breaking above its long-term downward trendline. At around R174 the share is much cheaper than it was, and private investors should look to accumulate the share on weakness. Consider the chart:

You can see here the new rising trend following the COVID-19 sell-off. You can also see that the share is on the brink of breaking above its long-term downward trendline – which opens the way for a strong recovery.

ITALTILE

Italtile (ITE) is a franchisor of tiles, sanitary ware, flooring and home finishing products - which it manufactures and wholesales itself. The company is controlled by the Ravazotti family. It has 198 stores and 6 online web stores. It also has a property portfolio of retail and industrial properties worth about R4,3bn. The company has acquired 95,47% of Ceramic Industries and 71,54% of Ezee Tile, which it styles as its "manufacturing" business (as opposed to its "retail" business). In a trading statement for the six months to 31st December 2020 the company estimated that headline earnings per share (HEPS) would be between 33% and 43% higher compared to the HEPS of 55,3c in the previous period. The company said that total retail sales between 1st July and 30th November 2020 "...grew by 16.4%...while like-for-like retail store sales increased by 14.9%." The company appears to be benefiting from increased sales as people work from home and seek to improve their home environments. It plans to add between 10 and 15 new stores this year. It has also bought back about R240m worth of its own shares at these lower levels. Technically, the share moved sideways for two years until COVID-19 took it down to levels around R10. Consider the chart:

.png)

The share is now breaking out above resistance at 1450c as economic conditions improve and it represents a significant buying opportunity.

CLICKS

The recent sell-off in Clicks shares must be seen as a buying opportunity. For the past 25 years Clicks shares have been climbing steadily. The chart goes from the bottom left-hand corner of your screen to the top right-hand corner. We call shares like this “diagonals” and they should always be accumulated on weakness. Consider the chart:

You can see the long-term pattern over a period which includes COVID-19, the Zuma years and the 2008 sub-prime crisis. This company just keeps on growing. In a trading update for the 21 weeks to 24th January 2021 the company reported group turnover up 7,8%. The CEO of the company, Vikesh Ramsunder, said, "Clicks reported good growth in front shop health sales as customers focused on preventative healthcare to boost their resistance levels with immunity- building vitamins and supplements. Online sales in Clicks continued their strong growth trajectory, increasing by 173% over the previous year."

← Back to Articles